Videos

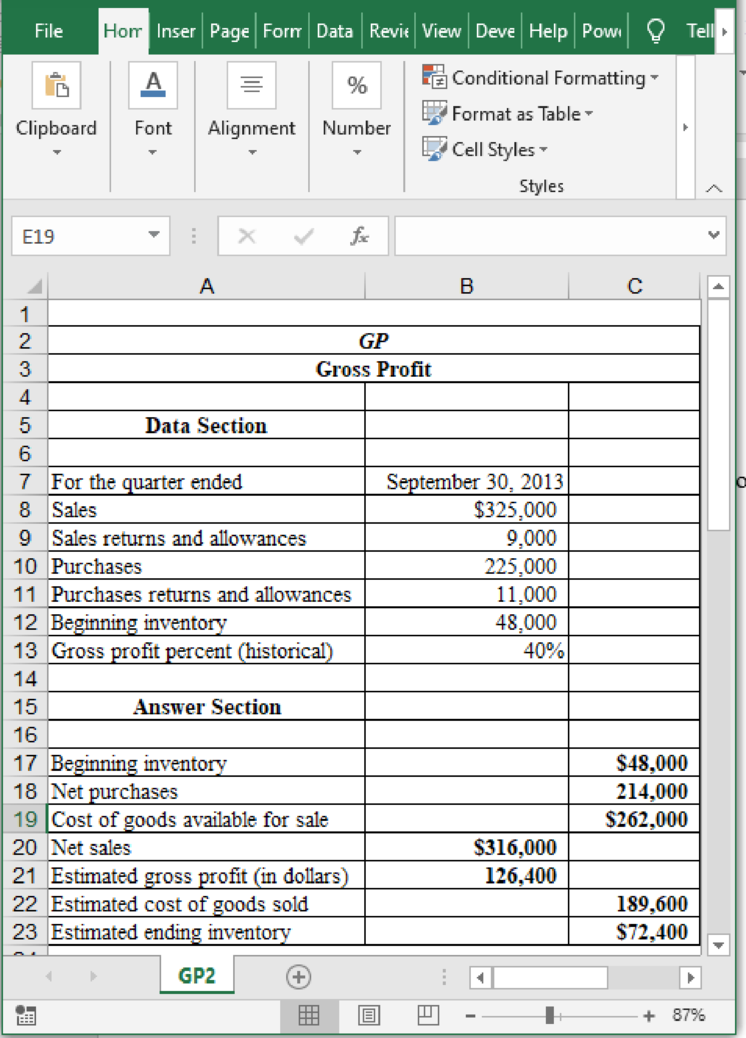

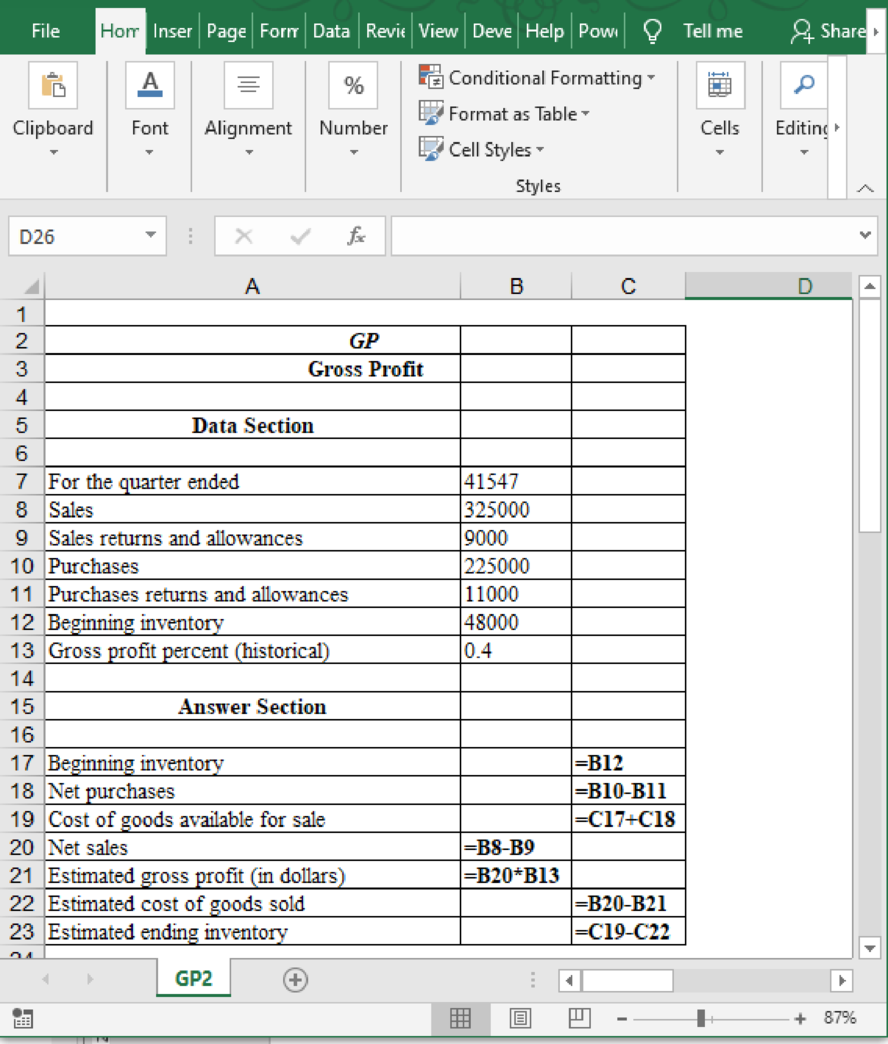

On September 30, 2013, the general ledger of Leonʼs Golf Shop, which uses the calendar year as its accounting period, showed the following year-to-date account balances:

The merchandise inventory account had a $48,000 balance on January 1, 2013. The historical gross profit percentage is 40%.

Leon prepares quarterly financial statements and takes physical inventory once a year–at the end of the accounting period. In order to prepare the financial statements for the third quarter, the store needs to have an estimate of ending inventory. You have been asked to use the gross profit method to estimate the ending inventory. Review the worksheet called GP. Study it carefully because it may have a solution format somewhat different from the one shown in your textbook.

Compute the ending inventory using the gross profit method.

Explanation of Solution

Compute the ending inventory using the gross profit method:

Table (1)

The formulae used in the table are given below:

Want to see more full solutions like this?

Chapter 8 Solutions

Excel Applications for Accounting Principles

- Martinez Shoe Sales has a January 31 fiscal year-end. At the start of the year, Martinez had 250 pairs of shoes in its Inventory at a cost of $30 per pair. Assume that the oldest inventory is sold first. Martinez uses a perpetual inventory system and estimates returns of 5% on all sales. During the month of February 2022, the following transactions took place: Feb. 4 Purchased 1,000 pairs for $20 each from Marigold Corp. on account, terms n/30. 11 Returned 100 pairs to Marigold for $2,000 credit because the shoes were the wrong size. 13 Sold 210 pairs for $90 each to Shoes for Kids, terms n/30. 18 Granted credit of $1,080 to Shoes for Kids for the return of 12 pairs that were the wrong colour. The shoes were restored to inventory. 26 Paid Marigold the amount owing. 28 Received payment in full from the Shoes for Kids. Record the February transactions. (Credit account titles are automatically indented when the amount is entered. Do not indent…arrow_forwardJack Hammer Company completed the following transactions. The annual accounting period ends December 31. Apr. 30 Received $465,000 from Commerce Bank after signing a 12-month, 7 percent, promissory note. June 6 Purchased merchandise on account at a cost of $66,000. (Assume a perpetual inventory system.) July 15 Paid for the June 6 purchase. Aug. 31 Signed a contract to provide security service to a small apartment complex starting in September, and collected six months' fees in advance amounting to $18,600. Dec. 31 Determined salary and wages of $31,000 were earned but not yet paid as of December 31 (ignore payroll taxes). Dec. 31 Adjusted the accounts at year-end, relating to interest. Dec. 31 Adjusted the accounts at year-end, relating to security service. Required: 1. & 2. Make journal entries for each of the transactions through August 31 and adjusting entries required on December 31. 3. Show how all of the liabilities arising from these items are reported on the balance sheet…arrow_forwardJack Hammer Company completed the following transactions. The annual accounting period ends December 31. Apr. 30 Received $672,000 from Commerce Bank after signing a 12-month, 9.00 percent, promissory note. June 6 Purchased merchandise on account at a cost of $81,000. (Assume a perpetual inventory system.) July 15 Paid for the June 6 purchase. Aug. 31 Signed a contract to provide security service to a small apartment complex starting in September, and collected six months' fees in advance, amounting to $27,000. Dec. 31 Determined salary and wages of $46,000 were earned but not yet paid as of December 31 (ignore payroll taxes). Dec. 31 Adjusted the accounts at year-end, relating to interest. Dec. 31 Adjusted the accounts at year-end, relating to security service. Required: For each listed transaction and related adjusting entry, indicate the accounts, amounts, and effects on the accounting equation. For each item, indicate whether the debt-to-assets ratio is increased or decreased…arrow_forward

- On January 1, 2022, Nash's Trading Post, LLC had Accounts Receivable of $57,300 and Allowance for Doubtful Accounts of $3,500. Nash's Trading Post, LLC prepares financial statements annually. During the year, the following selected transactions occurred: Sold $4,500 of merchandise to Rian Company, terms n/30. Accepted a $4,500, 4-month, 10% promissory note from Rian Company for balance due. Sold $14,400 of merchandise to Cato Company and accepted Cato's $14,400, 2-month, 10% note for the balance due. Sold $5,700 of merchandise to Malcolm Co., terms n/10. Accepted a $5,700, 3-month, 8% note from Malcolm Co. for balance due. Jan. 5 Feb. 2 12 26 Apr. 5 12 Collected Cato Company note in full. June 2 Collected Rian Company note in full. 15 Sold $2,100 of merchandise to Gerri Inc. and accepted a $2,100, 6-month, 11% note for the amount due.arrow_forwardJack Hammer Company completed the following transactions. The annual accounting period ends December 31. Apr. 30 Received $600,000 from Commerce Bank after signing a 12-month, 6 percent, promissory note. June 6 Purchased merchandise on account at a cost of $75,000. (Assume a perpetual inventory system.) July 15 Paid for the June 6 purchase. Aug. 31 Signed a contract to provide security service to a small apartment complex starting in September, and collected six months’ fees in advance, amounting to $24,000. Dec. 31 Determined salary and wages of $40,000 were earned but not yet paid as of December 31 (ignore payroll taxes). Dec. 31 Adjusted the accounts at year-end, relating to interest. Dec. 31 Adjusted the accounts at year-end, relating to security service. Required: For each listed transaction and related adjusting entry, indicate the accounts, amounts, and effects on the accounting equation. For each item, indicate whether the debt-to-assets ratio is increased or decreased or there…arrow_forwardOn January 1, 2022, Sunland Company had Accounts Receivable of $54,800 and Allowance for Doubtful Accounts of $3,800. Sunland Company prepares financial statements annually. During the year, the following selected transactions occurred: Jan. 5 Sold $4,700 of merchandise to Rian Company, terms n/30. Feb. 2 Accepted a $4,700, 4-month, 9% promissory note from Rian Company for balance due. 12 Sold $10,140 of merchandise to Cato Company and accepted Cato’s $10,140, 2-month, 10% note for the balance due. 26 Sold $5,300 of merchandise to Malcolm Co., terms n/10. Apr. 5 Accepted a $5,300, 3-month, 8% note from Malcolm Co. for balance due. 12 Collected Cato Company note in full. June 2 Collected Rian Company note in full. 15 Sold $1,800 of merchandise to Gerri Inc. and accepted a $1,800, 6-month, 11% note for the amount due. Journalize the transactions. (Omit cost of goods sold entries.) (Credit account titles are automatically indented when amount is…arrow_forward

- Jack Hammer Company completed the following transactions. The annual accounting period ends December 31. April 30 Received $672,000 from Commerce Bank after signing a 12-month, 9.00 percent, promissory note. June 6 Purchased merchandise on account at a cost of $81,000. (Assume a perpetual inventory system.) July 15 Paid for the June 6 purchase. August 31 Signed a contract to provide security service to a small apartment complex starting in September, and collected six months' fees in advance, amounting to $27,000. December 31 Determined salary and wages of $46,000 were earned but not yet paid as of December 31 (ignore payroll taxes). December 31 Adjusted the accounts at year-end, relating to interest. December 31 Adjusted the accounts at year-end, relating to security service. Required: 1. For each listed transaction and related adjusting entry, indicate the accounts, amounts, and effects on the accounting equation. 2. For each item, indicate whether the debt-to-assets ratio is…arrow_forwardOn January 1, 2022, Kingbird, Inc. had Accounts Receivable of $49,900 and Allowance for Doubtful Accounts of $3,500. Kingbird, Inc. prepares financial statements annually. During the year, the following selected transactions occurred: Jan. 5 Sold $3,450 of merchandise to Rian Company, terms n/30. Feb. 2 Accepted a $3,450, 4-month, 8% promissory note from Rian Company for balance due. 12 Sold $11,800 of merchandise to Cato Company and accepted Cato’s $11,800, 2-month, 9% note for the balance due. 26 Sold $5,300 of merchandise to Malcolm Co., terms n/10. Apr. 5 Accepted a $5,300, 3-month, 8% note from Malcolm Co. for balance due. 12 Collected Cato Company note in full. June 2 Collected Rian Company note in full. 15 Sold $2,200 of merchandise to Gerri Inc. and accepted a $2,200, 6-month, 11% note for the amount due. Journalize the transactions. (Omit cost of goods sold entries.) (Credit account titles are automatically indented when amount is…arrow_forwardOn January 1, 2022, Skysong, Inc. had Accounts Receivable of $52,500 and Allowance for Doubtful Accounts of $3,800. Skysong, Inc. prepares financial statements annually. During the year, the following selected transactions occurred. Jan. 5 Sold $4,200 of merchandise to Rian Company, terms n/30. Feb. 2 Accepted a $4,200, 4-month, 9% promissory note from Rian Company for balance due. 12 Sold $10,800 of merchandise to Cato Company and accepted Cato’s $10,800, 2-month, 10% note. 26 Sold $5,500 of merchandise to Malcolm Co., terms n/10. Apr. 5 Accepted a $5,500, 3-month, 8% note from Malcolm Co. 12 Collected Cato Company note in full. June 2 Collected Rian Company note in full. 15 Sold $2,200 of merchandise to Gerri Inc. and accepted a $2,200, 6-month, 12% note. Journalize the transactions. (Omit cost of goods sold entries.) (Do not round intermediate calculations. Round final answers to 0 decimal places, e.g. 5,275. Credit account titles are…arrow_forward

- Ehler Corporation sells rock-climbing products and also operates an indoor climbing facility for climbing enthusiasts. During the last part of 2017, Ehler had the following transactions related to notes payable. Sept. 1 Issued a $12,000 note to Pippen to purchase inventory. The 3-month note payable bears interest of 6% and is due December 1. (Ehler uses a perpetual inventory system.) Sept. 30 Recorded accrued interest for the Pippen note. Oct. 1 Issued a $16,500, 8%, 4-month note to Prime Bank to finance the purchase of a new climbing wall for advanced climbers. The note is due February 1. Oct. 31 Recorded accrued interest for the Pippen note and the Prime Bank note. Nov. 1 Issued a $26,000 note and paid $8,000 cash to purchase a vehicle to transport clients to nearby climbing sites as part of a new series of climbing classes. This note bears interest of 6% and matures in 12 months. Nov. 30 Recorded accrued interest for the Pippen note,…arrow_forwardOn January 1, 2022, Harvee Company had Accounts Receivable of $54,200 and Allowance for Doubtful Accounts of $3,700. Harvee Company prepares financial statements annually. During the year, the following selected transactions occurred: Jan. 5 Sold $4,000 of merchandise to Rian Company, terms n/30. Feb. 2 Accepted a $4,000, 4-month, 9% promissory note from Rian Company for balance due. 12 Sold $12,000 of merchandise to Cato Company and accepted Cato’s $12,000, 2-month, 10% note for the balance due. 26 Sold $5,200 of merchandise to Malcolm Co., terms n/10. Apr. 5 Accepted a $5,200, 3-month, 8% note from Malcolm Co. for balance due. 12 Collected Cato Company note in full. June 2 Collected Rian Company note in full. 15 Sold $2,000 of merchandise to Gerri Inc. and accepted a $2,000, 6-month, 12% note for the amount due. - Journalize the transactions (Omit cost of good sold entries)arrow_forwardOn January 1, 2018, Carly Company had accounts receivable $109,000 and allowance for doubtful accounts $10,000. Carly Company prepares financial statements annually. During the year the following selected transactions occurred. Jan. 5 Sold $12,000 of merchandise to Sam Company, terms n/30. Feb. 2 Accepted a $12,000, 4-month, 10% promissory note from Sam Company for the balance due. 12 Sold $15,000 of merchandise to Neville Company and accepted Neville's $15,000, 2-month, 10% note for the balance due. Apr. 12 Collected Neville Company note in full. June 2 Collected Sam Company note in full. July 15 Sold $11,000 of merchandise to Hutchinson Co. and accepted Hutchinson's $11,000, 3-month, 12% note for the amount due. Oct. 15 Hutchinson Co.'s note was dishonored. Hutchinson Co. is bankrupt, and there is no hope of future settlement. Instructions Journalize the transactions.arrow_forward

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College