Videos

Cost Data for Managerial Purposes

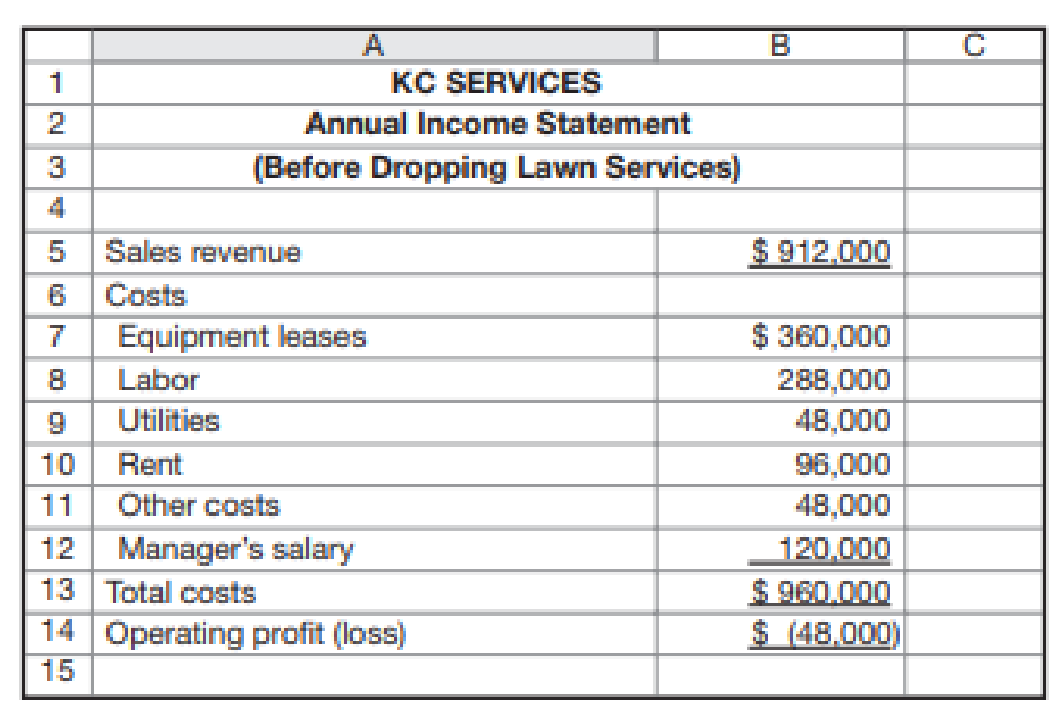

KC Services provides landscaping services in Edison. Kate Chen, the owner, is concerned about the recent losses the company has incurred and is considering dropping its lawn services, which she feels are marginal to the company’s business. She estimates that doing so will result in lost revenues of $150,000 per year (including the lost tree business from customers who use the company for both services). The present manager will continue to supervise the tree services with no reduction in salary. Without the lawn business, Kate estimates that the company will save 15 percent of the equipment leases, labor, and other costs. She also expects to save 20 percent on rent and utilities.

Required

- a. Prepare a report of the differential costs and revenues if the lawn service is discontinued. (Hint: Use the format of Exhibit 1.3.)

- b. Should Kate discontinue the lawn service?

- c. Are there factors other than the differential costs and revenues that Kate should consider?

Want to see the full answer?

Check out a sample textbook solution

Chapter 1 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- Ellie Ice-cream’s owner is disturbed by the poor profit performance of his ice cream counter. He has prepared the following profit analyses for the year just ended: The owner is thinking the elimination of this counter. If it is eliminated then: Depreciation of counter equipment is avoidable The supervisory salaries is avoidable The insurance expense is unavoidable The depreciation of building unavoidable The general overhead is unavoidable Required:a) Should the company eliminate the counter or not? Fill in the table and justify your answer. b) Mention at least three relevant costs.arrow_forwardMembers of the board of directors of Security Team have received the following operating income data for the year ended May 31, 2018: E (Click the icon to view the operating income data.) Members of the board are surprised that the industrial systems product line is not profitable. They commission a study to determine whether the company should drop the line. Company accountants estimate that dropping industrial systems will decrease fixed cost of goods sold by $84,000 and decrease fixed selling and administrative expenses by $10,000. Read the requirements. Requirement 1. Prepare a differential analysis to show whether Security Team should drop the industrial systems product line. (Use parentheses or a minus sign to enter decreases to profits.) in operating income - X Requirements 1. Prepare a differential analysis to show whether Security Team should drop the industrial systems product line. 2. Prepare contribution margin income statements to show Security Team's total operating…arrow_forwardMaking decisions about dropping a product Members of the board of directors of Security Team have received the following operating income data for the year ended March 31, 2018: Members of the board are surprised that the industrial systems product line is losing money. They commission a study to determine whether the company should drop the line. Company accountants estimate that dropping industrial systems will decrease fixed cost of goods sold by $81,000 and decrease fixed selling and administrative expenses by $15,000. Requirements Prepare a differential analysis to show whether Security Team should drop the industrial systems product line. Prepare contribution margin income statements to show Security Team’s total operating income under the two alternatives: (a) with the industrial systems line and without the line. Compare the difference between the two alternatives’ income numbers to your answer to Requirement l. What have you learned from this comparison in Requirement 2?arrow_forward

- Top managers of Vermont Flooring are alarmed by their operating losses. They are considering dropping the laminate flooring product line. Company accountants have prepared the following analysis to help make this decision in the chart below: Total fixed costs will not change if the company stops selling laminate flooring. Requirements 1. Prepare an incremental analysis to show whether Vermont Flooring should discontinue the laminate flooring product line. Will discontinuing laminate flooring add $28,000 to operating income? Explain. 2. Assume that the company can avoid $32,000 of fixed expenses by discontinuing the laminate flooring product line (these costs are direct fixed costs of the laminate flooring product line). Prepare an incremental analysis to show whether the company should stop selling laminate flooring. 3. Now, assume that all of the fixed costs assigned to laminate flooring are direct fixed costs and can be avoided if the company stops selling laminate flooring. However,…arrow_forwardFusion Metals Company is considering the elimination of its Packaging Department. Management has received an offer from an outside firm to supply all Fusion’s packaging needs. To help her in making the decision, Fusion’s president has asked the controller for an analysis of the cost of running Fusion’s Packaging Department. Included in that analysis is $9,100 of rent, which represents the Packaging Department’s allocation of the rent on Fusion’s factory building. If the Packaging Department is eliminated,the space it used will be converted to storage space. Currently Fusion rents storage space in a nearby warehouse for $11,000 per year. The warehouse rental would no longer be necessary if the Packaging Department were eliminated. Required:1. Discuss each of the figures given in the exercise with regard to its relevance in the departmentclosing decision.2. What type of cost is the $11,000 warehouse rental, from the viewpoint of the costs of the Packaging Department?arrow_forwardThe management of Wengel Corporation is considering dropping product B90D. Data from the company's accounting system appear below: Sales Variable expenses Fixed manufacturing expenses Fixed selling and administrative expenses All fixed expenses of the company are fully allocated to products in the company's accounting system. Further investigation has revealed that $179,000 of the fixed manufacturing expenses and $155,200 of the fixed selling and administrative expenses are avoidable if product B90D is discontinued. Required: What would be the financial advantage (disadvantage) of dropping B90D? Should the product be dropped? Net operating income (loss) would $ 745,000 $ 387,000 $ 253,400 $216,200 decline increase by if product B90D were dropped. Therefore, the product droppedarrow_forward

- Equipment replacement decisions and performance evaluation. Susan Smith manages the Wexford plant of Sanchez Manufacturing. A representative of Darnell Engineering approaches Smith about replacing a large piece of manufacturing equipment that Sanchez uses in its process with a more efficient model. While the representative made some compelling arguments in favor of replacing the 3-year-old equipment, Smith is hesitant. Smith is hoping to be promoted next year to manager of the larger Detroit plant, and she knows that the accrual-basis net operating income of the Wexford plant will be evaluated closely as part of the promotion decision. The following information is available concerning the equipment replacement decision: Sanchez uses straight-line depreciation on all equipment. Annual depreciation expense for the old machine is $180,000 and will be $270,000 on the new machine if it is acquired. For simplicity, ignore income taxes and the time value of money.arrow_forwardJerry Prior, Beeler Corporation’s controller, is concerned that net income may be lower this year. He is afraid upper-level management might recommend cost reductions by laying off accounting staff, including him. Prior knows that depreciation is a major expense for Beeler. The company currently uses the double-declining-balance method for both financial reporting and tax purposes, and he’s thinking of selling equipment that, given its age, is primarily used when there are periodic spikes in demand. The equipment has a carrying value of $2,000,000 and a fair value of $2,180,000. The gain on the sale would be reported in the income statement. He doesn’t want to highlight this method of increasing income. He thinks, “Why don’t I increase the estimated useful lives and the salvage values? That will decrease depreciation expense and require less extensive disclosure, since the changes are accounted for prospectively. I may be able to save my job and those of my staff.” Instructions Answer…arrow_forwardSophia & More Company sells clothing, shoes and accessories at a city location near you. Information for the just concluded calendar year follows. Management is considering closing the Shoe segment because of the operating loss and is thinking about expanding the space that is currently devoted to the Accessories segment. A salaried salesperson in the Shoe segment who earns $45,000 will be terminated; however, all other segmental fixed costs will continue to be incurred. Sophia & More will spend $16,000 on remodeling costs and anticipates that sales in the Accessories segment will increase by $70,000. This additional sales revenue is expected to generate a 35% contribution margin for the company. Finally, because clothing customers often purchased shoes and feel strongly about "one-stop shopping," clothing sales are expected to fall by 15% if the Shoe segment is closed. Required: Using incremental analysis, determine whether the Shoe segment should be closed and if so, what…arrow_forward

- Making decisions about dropping a product Members of the board of directors or Security Check have received the following operating income data for the year ended May 31, 2018: Members of my board are surprised that the industrial systems product line is not profitable. They commission a study to determine whether the company should drop the line. Company accountants estimate that dropping industrial systems will decrease the fixed cost of goods sold by $580,000 and decrease fixed selling and administrative expenses by $12,000. Requirements Prepare a differential analysis to show whether Security Check should drop the industrial systems product line. Prepare contribution margin income statements to show Security Check’s total operating income under the two alternatives: (a) with the industrial systems line and (b) without the line. Compare the difference between the two alternatives’ income numbers to your answer to Requirement 1. What have you learned from the comparison in…arrow_forwardBannister Company, an electronics firm, buys circuit boards and manually inserts various electronic devices into the printed circuit board. Bannister sells its products to original equipment manufacturers. Profits for the last two years have been less than expected. Mandy Confer, owner of Bannister, was convinced that her firm needed to adopt a revenue growth and cost reduction strategy to increase overall profits. After a careful review of her firms condition, Mandy realized that the main obstacle for increasing revenues and reducing costs was the high defect rate of her products (a 6 percent reject rate). She was certain that revenues would grow if the defect rate was reduced dramatically. Costs would also decline as there would be fewer rejects and less rework. By decreasing the defect rate, customer satisfaction would increase, causing, in turn, an increase in market share. Mandy also felt that the following actions were needed to help ensure the success of the revenue growth and cost reduction strategy: a. Improve the soldering capabilities by sending employees to an outside course. b. Redesign the insertion process to eliminate some of the common mistakes. c. Improve the procurement process by selecting suppliers that provide higher-quality circuit boards. Required: 1. State the revenue growth and cost reduction strategy using a series of cause-and-effect relationships expressed as if-then statements. 2. Illustrate the strategy using a strategy map. 3. Explain how the revenue growth strategy can be tested. In your explanation, discuss the role of lead and lag measures, targets, and double-loop feedback.arrow_forwardWright Plastic Products is a small company that specialized in the production of plastic dinner plates until several years ago. Although profits for the company had been good, they have been declining in recent years because of increased competition. Many competitors offer a full range of plastic products, and management felt that this created a competitive disadvantage. The output of the companys plants was exclusively devoted to plastic dinner plates. Three years ago, management made a decision to add additional product lines. They determined that existing idle capacity in each plant could easily be adapted to produce other plastic products. Each plant would produce one additional product line. For example, the Atlanta plant would add a line of plastic cups. Moreover, the variable cost of producing a package of cups (one dozen) was virtually identical to that of a package of plastic plates. (Variable costs referred to here are those that change in total as the units produced change. The costs include direct materials, direct labor, and unit-based variable overhead such as power and other machine costs.) Since the fixed expenses would not change, the new product was forecast to increase profits significantly (for the Atlanta plant). Two years after the addition of the new product line, the profits of the Atlanta plant (as well as other plants) had not improvedin fact, they had dropped. Upon investigation, the president of the company discovered that profits had not increased as expected because the so-called fixed cost pool had increased dramatically. The president interviewed the manager of each support department at the Atlanta plant. Typical responses from four of those managers are given next. Materials handling: The additional batches caused by the cups increased the demand for materials handling. We had to add one forklift and hire additional materials handling labor. Inspection: Inspecting cups is more complicated than plastic plates. We only inspect a sample drawn from every batch, but you need to understand that the number of batches has increased with this new product line. We had to hire more inspection labor. Purchasing: The new line increased the number of purchase orders. We had to use more resources to handle this increased volume. Accounting: There were more transactions to process than before. We had to increase our staff. Required: 1. Explain why the results of adding the new product line were not accurately projected. 2. Could this problem have been avoided with an activity-based cost management system? If so, would you recommend that the company adopt this type of system? Explain and discuss the differences between an activity-based cost management system and a traditional cost management system.arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning