Concept explainers

Videos

MacGyver Corporation manufactures a product called Miracle Goo, which comes in handy for just about anything. The thick tarry substance is sold in six-gallon drums. Two raw materials are used; these are referred to by people in the business as A and B. Two types of labor are required also. These are mixers (labor class I) and packers (labor class II). You were recently hired by the company president, Pete Thorn, to be the controller. You soon learned that MacGyver uses a standard-costing system. Variances are computed and closed into Cost of Goods Sold monthly. After your first month on the job, you gathered the necessary data to compute the month’s variances for direct material and direct labor. You finished everything up by 5:00 p.m. on the 31st, including the credit to Cost of Goods Sold for the sum of the variances. You decided to take all your notes home to review them prior to your formal presentation to Thorn first thing in the morning. As an afterthought, you grabbed a drum of Miracle Goo as well, thinking it could prove useful in some unanticipated way.

You spent the evening boning up on the data for your report and were ready to call it a night. As luck would have it though, you knocked over the Miracle Goo as you rose from the kitchen table. The stuff splattered everywhere, and, most unfortunately, obliterated most of your notes. All that remained legible is the following information.

Other assorted data gleaned from your notes:

- The standards for each drum of Miracle Goo include 10 pounds of material A at a standard price of $5 per pound.

- The standard cost of material B is $15 for each drum of Miracle Goo.

- Purchases of material A were 12,000 pounds at $4.50 per pound.

- Given the actual output for the month, the standard allowed quantity of material A was 10,000 pounds. The standard allowed quantity of material B was 5,000 gallons.

- Although 6,000 gallons of B were purchased, only 4,800 gallons were used.

- The standard wage rate for mixers is $15 per hour. The standard labor cost per drum of product for mixers is $30 per drum.

- The standards allow 4 hours of direct labor II (packers) per drum of Miracle Goo. The standard labor cost per drum of product for packers is $48 per drum.

- Packers were paid $11.90 per hour during the month.

You happened to remember two additional facts. There were no beginning or ending inventories of either work in process or finished goods for the month. The increase in accounts payable relates to direct-material purchases only.

Required: Now you’ve got a major problem. Somehow you’ve got to reconstruct all the missing data in order to be ready for your meeting with the president. You start by making the following list of the facts you want to use in your presentation. Before getting down to business, you need a brief walk to clear your head. Out to the trash you go, and toss the remaining Miracle Goo.

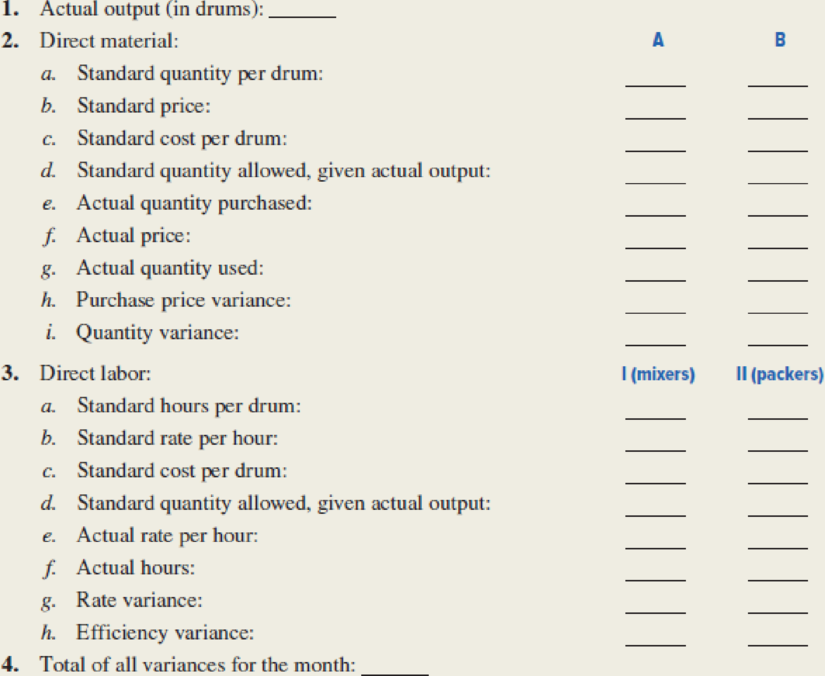

Fill in the missing amounts in the list, using the available facts.

Calculate the missing amount of Company M.

Explanation of Solution

Variance: Variance refers to the difference level in the actual cost incurred and standard cost. The total cost variance is subdivided into separate cost variances; this cost variance indicates that the amount of variance that is attributable to specific casual factors.

Calculate the missing amount of Company M as follows:

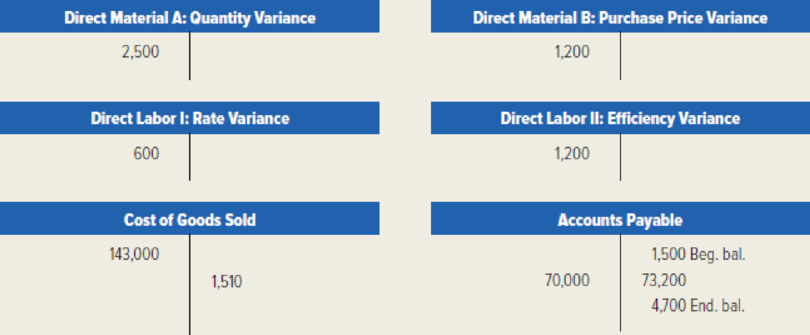

| Particulars | Amount in $ | |

| 1. Actual output (in drums) (1) | 1,000 drums | |

| 2. Direct materials: | A | B |

| a. Standard quantity per drum (2) | 10 lb | 5 gal |

| b. Standard price (3) | $5.00/lb | $3.00/gal. |

| c. Standard cost per drum (4) | $ 50.00 | $ 15.00 |

| d. Standard quantity allowed, given actual output (5) | 10,000 lb | 5,000 gal |

| e. Actual quantity purchased (6) | 12,000 lb | 6,000 gal |

| f. Actual price (7) | $4.50/lb | $3.20/gal. |

| g. Actual quantity used (8) | 10,500 lb | 4,800 gal |

| h. Purchase price variance(9) | $6,000 F | $1,200 U |

| i. Quantity variance (10) | $2,500 U | $600 F |

| 3. Direct labor: |

I (mixers) | II (packers) |

| a. Standard hours per drum (11) | 2 hr. | 4 hr. |

| b. standard rate per hour (12) | $ 15.00 | $ 12.00 |

| c. Standard cost per drum (13) | $ 30.00 | $ 48.00 |

| d. Standard quantity allowed, given actual output (14) | 2,000 hr. | 4,000 hr. |

| e. Actual rate per hour (15) | $ 15.30 | $ 11.90 |

| f. Actual hours(16) | 2,000 hr. | 4,100 hr. |

| g. Rate variance (17) | $600 U | $410 F |

| h. Efficiency variance (18) | 0 | $1,200 U |

| 4. Total of all variance for the month (19) | $1,510 F | |

Table (1)

Working note (1):

Calculate (1) the actual output of Company M.

Working note (2):

Calculate the (2. a.) standard quantity of direct material per drum:

Material A:

The standard quantity of direct material per drum of material A is 10 lb. (given).

Material B:

Note: 10,000 pound = 10lb.

Working note (3):

Calculate the (2. b.) the standard price of direct material:

Material A:

The standard price of direct material A is $5.00/lb. (given).

Material B:

Working note (4):

Calculate the (2. c.) the standard cost per drum:

Material A:

Material B:

Standard cost of direct material B is $15 (given).

Working note (5):

Calculate the (2. d.) the standard quantity allowed for actual output:

The standard quantity allowed for actual output of Material A is 10,000 lb. (given).

The standard quantity allowed for actual output of Material B is 5,000 gal. (given).

Working note (6):

Calculate the (2. e.) the actual quantity purchased:

The actual quantity purchased for Material A is 12,000 lb. (given).

The actual quantity purchased for Material B is 6,000 gal (given).

Working note (7):

Calculate the (2. f.) the actual price of direct material:

Material A:

The actual price of direct material A is $4.50/lb. (given).

Material B:

Working note (8):

Calculate the (2. g.) the actual quantity used during the month:

Material A:

Material B:

The actual quantity of material B used during the month is 4,800 gal (given).

Working note (9):

Calculate the (2. h.) the price variance for direct material:

Material A:

Material B:

The price variance of material B is $1,200 Unfavorable (given).

Working note (10):

Calculate the (2. i.) the quantity variance for direct material:

Material A:

The quantity variance of direct material A is $2,500 Unfavorable (given).

Material B:

Note: Debit side of variance account indicates the unfavorable variance, and credit side of variance account indicates the favorable variance.

Working note (11):

Calculate the (3. a.) the standard direct labor hours per drum:

Mixers:

Packers:

The standard direct labor hour per drum is 4 hours (given).

Working note (12):

Calculate the (3. b.) the standard rate per hour:

Mixers:

The standard rate per hour for mixers is $15.00 (given).

Packers:

Working note (13):

Calculate the (3. c.) the standard cost per drum:

The standard cost per drum for Mixers (type-I labor) is $30.00 (given).

The standard cost per drum for Packers (type-II labor) is $48.00 (given).

Working note (14):

Calculate the (3. d.) the standard quantity allowed for actual output:

Mixers:

Packers:

Working note (15):

Calculate the (3. e.) the actual rate per hour:

Mixers:

Packers:

The actual rate per hour for packers (type-II labor) is $11.90 (given).

Working note (16):

Calculate the (3. f.) the actual direct labor hours:

Mixers:

In this case, there is no efficiency variance for type I labors. Hence standard hours are equal to actual hours. Therefore, the actual direct labor hours for type I labors is 2,000 hours (given).

Packers:

Working note (17):

Calculate the (3. g.) the direct labor rate variance:

Mixers:

The direct labor rate variance for type-I labor is $600 Unfavorable (given).

Packers:

Working note (18):

Calculate the (3. h.) the direct labor efficiency variance:

The direct labor efficiency variance of mixtures (type-I labor) is $0 (given).

The direct labor efficiency variance of packers (type-II labor) is $1,200 Unfavorable (given).

Working note (19):

Calculate the (4) the total of all variances for the month:

| Particulars | Amount in $ |

| Direct-material variances: | |

| Price variance of material A (9) | 6,000 F |

| Quantity variance of material A (10) | -2,500 U |

| Price variance of material B (9) | -1,200 U |

| Quantity variance of material B (10) | 600 F |

| Direct-labor variances: | |

| Rate variance of type I labor (17) | -600 U |

| Efficiency variance of type I labor (18) | 0 |

| Rate variance of type II labor (17) | 410 F |

| Efficiency variance of type II labor (18) | -1,200 U |

| Total of all variances | 1,510 F |

Table (2)

Want to see more full solutions like this?

Chapter 10 Solutions

Managerial Accounting: Creating Value in a Dynamic Business Environment

- WoolCorp buys sheep’s wool from farmers. The company began operations in January of this year, and is making decisions on product offerings, pricing, and vendors. The company is also examining its method of assigning overhead to products. You’ve just been hired as a production manager at WoolCorp. Currently WoolCorp makes three products: (1) raw, clean wool to be used as stuffing or insulation; (2) wool yarn for use in the textile industry, and (3) extra-thick yarn for use in rugs. Upper management would like your recommendations regarding a production decision regarding their current and proposed product lines. For the past year, WoolCorp has experimented with its third product, extra-thick rug yarn. The company wishes to consider whether to continue or discontinue manufacturing and selling this product. You decide to prepare a differential analysis of the income related to all three products. To begin your analysis, you review the following condensed income statement. Then scroll…arrow_forwardBig Boomers makes custom clubs for golfers. Most of the work is done by hand and with small tools used by craftsmen. Customers are quoted a price in advance of their clubs being manufactured. To produce clubs at a profit, management must have a thorough understanding of product costs. Jeff Ranck, manager of the business, is using direct labor hours as the activity base for allocating overhead costs. He estimated the following amounts at the beginning of 2022: Estimated total overhead. .$190,000Estimated direct labor hou .16,000 hours The following information is available for job number 17, which was started and completed in February 2022: - Direct materials used$1200- Direct labor used$600(corresponding to 50 direct labor hours) Prepare journal entries to: a. Record all the manufacturing costs charged to job 17 . b. Record the completion of job 17. c. Record the cash sale of job 17 in its entirety at a selling price of13%of its manufacturing cost. Record in a separate entry the…arrow_forwardJohnny Lee Incorporated produces a line of small gasoline-powered engines that can be used in a variety of residential machines, ranging from different types of lawnmowers, to snowblowers, to garden tools (such as tillers and weed-whackers). The basic product line consists of three different models, each meant to fill the needs of a different market. Assume you are the cost accountant for this company and that you have been asked by the owner of the company to construct a flexible budget for factory overhead costs, which seem to be growing faster than revenues. Currently, the company uses machine hours (MHs) as the basis for assigning both variable and fixed factory overhead costs to products. Within the relevant range of output, you determine that the following factory fixed overhead costs per month should occur: engineering support, $15,200; insurance on the manufacturing facility, $5,200; property taxes on the manufacturing facility, $12,200; depreciation on manufacturing…arrow_forward

- While attending night school to earn a degree in computer engineering, Stan Wilson worked for Morlot Container Company (MCC) as an assembly line supervisor. MCC was located near Wilson’s hometown and had been a prominent employer in the area for many years.MCC’s main product was milk cartons that were distributed throughout the Midwest for milk processing plants.The technology at MCC was stable, and the assembly lines were monitored closely. MCC employed a standard cost system because cost control was considered important. The employees who manned the assembly lines were generally unskilled workers who had been with the company for many years; the majority of these workers belonged to the local union.Wilson was glad he was nearly finished with school because he found the work at MCC to be repetitive and boring, even as a supervisor. The supervisors were monitored almost as closely as the line workers, and standard policies and procedures existed that applied to most situations. Most of…arrow_forwardJohnny Lee Incorporated produces a line of small gasoline-powered engines that can be used in a variety of residential machines, ranging from different types of lawnmowers, to snowblowers, to garden tools (such as tillers and weed-whackers). The basic product line consists of three different models, each meant to fill the needs of a different market. Assume you are the cost accountant for this company and that you have been asked by the owner of the company to construct a flexible budget for factory overhead costs, which seem to be growing faster than revenues. Currently, the company uses machine hours (MHs) as the basis for assigning both variable and fixed factory overhead costs to products. Within the relevant range of output, you determine that the following factory fixed overhead costs per month should occur: engineering support, $15,200; insurance on the manufacturing facility, $5,200; property taxes on the manufacturing facility, $12,200; depreciation on manufacturing…arrow_forwardWoolCorp WoolCorp buys sheep’s wool from farmers. The company began operations in January of this year, and is making decisions on product offerings, pricing, and vendors. The company is also examining its method of assigning overhead to products. You’ve just been hired as a production manager at WoolCorp. Currently WoolCorp makes two products: (1) raw, clean wool to be used as stuffing or insulation and (2) wool yarn for use in the textile industry. The company would like you to evaluate its costing methods for its raw wool and wool yarn. Single Plantwide Rate WoolCorp is currently using the single plantwide factory overhead rate method, which uses a predetermined overhead rate based on an estimated allocation base such as direct labor hours or machine hours. The rate is computed as follows: Single Plantwide Factory Overhead Rate = (Total Budgeted Factory Overhead) ÷ (Total Budgeted Plantwide Allocation Base) WoolCorp has been using combing machine hours as its allocation base.…arrow_forward

- Whitley Construction Company is in the home remodeling business. Whitley has three teams of highly skilled employees, each of whom has multiple skills involving carpentry, painting, and other home remodeling activities. Each team is led by an experienced employee who coordinates the work done on each job. As the needs of different jobs change, some team members may be shifted to other teams for short periods of time. Whitley uses a job costing system to determine job costs and to serve as a basis for bidding and pricing the jobs. Direct materials and direct labor are easily traced to each job using Whitley’s cost tracking software. Overhead consists of the purchase and maintenance of construction equipment, some supervisory labor, the cost of bidding for new customers, and administrative costs. Whitley uses an annual overhead rate based on direct labor hours. Whitley has recently completed work for three clients: Harrison, Barnes, and Tyler. The cost data for each of the three jobs are…arrow_forwardWhitley Construction Company is in the home remodeling business. Whitley has three teams of highly skilled employees, each of whom has multiple skills involving carpentry, painting, and other home remodeling activities. Each team is led by an experienced employee who coordinates the work done on each job. As the needs of different jobs change, some team members may be shifted to other teams for short periods of time. Whitley uses a job costing system to determine job costs and to serve as a basis for bidding and pricing the jobs. Direct materials and direct labor are easily traced to each job using Whitley's cost tracking software. Overhead consists of the purchase and maintenance of construction equipment, some supervisory labor, the cost of bidding for new customers, and administrative costs. Whitley uses an annual overhead rate based on direct labor hours. Whitley has recently completed work for three clients: Harrison, Barnes, and Tyler. The cost data for each of the three jobs are…arrow_forwardWhitley Construction Company is in the home remodeling business. Whitley has three teams of highly skilled employees, each of whom has multiple skills involving carpentry, painting, and other home remodeling activities. Each team is led by an experienced employee who coordinates the work done on each job. As the needs of different jobs change, some team members may be shifted to other teams for short periods of time. Whitley uses a job costing system to determine job costs and to serve as a basis for bidding and pricing the jobs. Direct materials and direct labor are easily traced to each job using Whitley's cost tracking software. Overhead consists of the purchase and maintenance of construction equipment, some supervisory labor, the cost of bidding for new customers, and administrative costs. Whitley uses an annual overhead rate based on direct labor hours. Whitley has recently completed work for three clients: Harrison, Barnes, and Tyler. The cost data for each of the three jobs are…arrow_forward

- Johnny Lee Inc. produces a line of small gasoline-powered engines that can be used in a variety of residential machines, ranging from different types of lawnmowers, to snowblowers, to garden tools (such as tillers and weed-whackers). The basic product line consists of three different models, each meant to fill the needs of a different market. Assume you are the cost accountant for this company and that you have been asked by the owner of the company to construct a flexible budget for factory overhead costs, which seem to be growing faster than revenues. Currently, the company uses machine hours (MHs) as the basis for assigning both variable and fixed factory overhead costs to products. Within the relevant range of output, you determine that the following factory fixed overhead costs per month should occur: engineering support, $15,800; insurance on the manufacturing facility, $5,800; property taxes on the manufacturing facility, $12,800; depreciation on manufacturing equipment,…arrow_forwardJohnny Lee Inc. produces a line of small gasoline-powered engines that can be used in a variety of residential machines, ranging from different types of lawnmowers, to snowblowers, to garden tools (such as tillers and weed-whackers). The basic product line consists of three different models, each meant to fill the needs of a different market. Assume you are the cost accountant for this company and that you have been asked by the owner of the company to construct a flexible budget for factory overhead costs, which seem to be growing faster than revenues. Currently, the company uses machine hours (MHs) as the basis for assigning both variable and fixed factory overhead costs to products. Within the relevant range of output, you determine that the following factory fixed overhead costs per month should occur: engineering support, $15,000; insurance on the manufacturing facility, $5,000; property taxes on the manufacturing facility, $12,000; depreciation on manufacturing equipment,…arrow_forwardRene is working with the operations manager to determine what the standard labor cost is for a spice chest. He has watched the process from start to finish and taken detailed notes on what each employee does. The fırst employee selects and mills the wood, so it is smooth on all four sides. This takes the employee 1 hour(s) for each chest. The next employee takes the wood and cuts it to the proper size. This takes 32 minutes. The next employee assembles and sands the chest. Assembly takes 3 hour(s). The chest then goes to the finishing department. It takes 3 hour(s) to finish the chest. All employees are cross-trained so they are all paid the same amount per hour, $18.62. What is the standard cost per chest for labor? Round to the nearest penny, two decimal places.arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education