(1)

Journalize the stock investment transactions in the books of Company Z.

(1)

Explanation of Solution

Trading securities: These are short-term investments in debt and equity securities with an intention of trading and earning profits due to changes in market prices.

Debit and credit rules:

- ■ Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in

stockholders’ equity accounts. - ■ Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Prepare journal entry for the purchase of 4,800 shares of Company AP, at $26 per share, and a brokerage commission of $192.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2016 | |||||

| February | 14 | Investments–Company AP Stock | 124,992 | ||

| Cash | 124,992 | ||||

| (To record purchase of shares for cash) | |||||

Table (1)

- ■ Investments–Company AP Stock is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of cash paid to purchase Company AP’s stock.

Prepare journal entry for the purchase of 2,300 shares of Company

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2016 | |||||

| April | 1 | Investments–Company AR Stock | 43,792 | ||

| Cash | 43,792 | ||||

| (To record purchase of shares for cash) | |||||

Table (2)

- ■ Investments–Company AR Stock is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of cash paid to purchase Company AR’s stock.

Prepare journal entry for sale of 600 shares of Company AP, at $32, with a brokerage of $100.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2016 | |||||

| June | 1 | Cash | 19,100 | ||

| Gain on Sale of Investments | 3,476 | ||||

| Investments–Company AP Stock | 15,624 | ||||

| (To record sale of shares) | |||||

Table (3)

- ■ Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- ■ Loss on Sale of Investments is a loss or expense account. Since losses decrease equity, equity value is decreased, and a decrease in equity is debited.

- ■ Investments–Company AP Stock is an asset account. Since stock investments are sold, asset value decreased, and a decrease in asset is credited.

Working Notes:

Calculate the realized gain (loss) on sale of stock.

Step 1: Compute cash received from sale proceeds.

Step 2: Compute cost of stock investment sold.

Step 3: Compute realized gain (loss) on sale of stock.

Note: Refer to Steps 1 and 2 for value and computation of cash received and cost of stock investment sold.

Prepare journal entry for the dividend received from Company AP for 4,200 shares.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2016 | |||||

| June | 27 | Cash | 840 | ||

| Dividend Revenue | 840 | ||||

| (To record receipt of dividend revenue) | |||||

Table (4)

- ■ Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- ■ Dividend Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Compute amount of dividend received on Company AP’s stock.

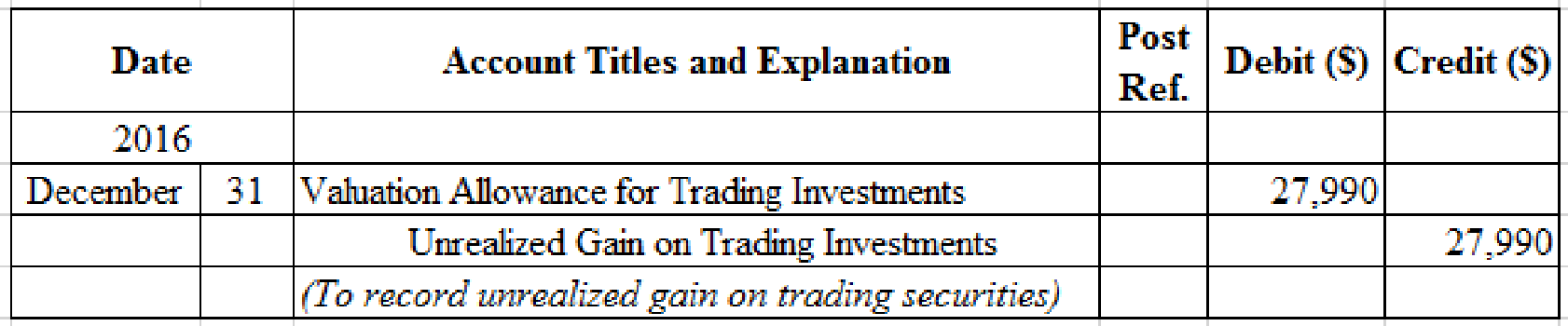

Prepare adjusting entry for valuation of trading securities transaction.

Figure(1)

- ■ Valuation Allowance for Trading Investments is a contra-asset account. The account is credited because the market price was increased (gain) to $181,150 from the cost of $153,160.

- ■ Unrealized Gain on Trading Investments is an adjustment account used to report gain or loss on adjusting cost of investment at fair market value. Since gain has occurred and increase stockholders’ equity value, and an increase in stockholders’ equity value is debited.

Working Notes:

Compute the unrealized gain (loss) as on December 31.

Step 1: Compute the fair value of the portfolio of the trading investment.

| Security | Number of Shares | Fair Market Value | = | Fair Market Value of Investment | |

| Company AP | 4,200 shares | $33.00 | = | $138,600 | |

| Company AR | 2,300 shares | 18.50 | = | 42,550 | |

| Total | $181,150 | ||||

Table (5)

Step 2: Compute the cost per share of Company AP.

Step 3: Compute the cost per share of Company AR.

Step 4: Compute the cost of the portfolio of the trading investment, as on December 31, 2016.

| Security | Number of Shares | Cost per Share | = | Cost of Investment | |

| Company AP | 4,200 shares | $26.04 | = | $109,368 | |

| Company AR | 2,300 shares | 19.04 | = | 43,792 | |

| Total | $153,160 | ||||

Table (6)

Note: Refer to Steps 3 and 4 for cost per share of Company AP and Company AR.

Step 5: Compute the unrealized gain (loss) as on December 31, 2016.

| Details | Amount ($) |

| Trading investments at fair value, December 31 (From Table-5) | $181,150 |

| Less: Trading investments at cost, December 31 (From Table-6) | (153,160) |

| Unrealized loss on trading investments | $27,990 |

Table (7)

Prepare journal entry for the purchase of 1,200 shares of Company AT, at $65 per share, and a brokerage commission of $120.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2017 | |||||

| March | 14 | Investments–Company AT Stock | 78,120 | ||

| Cash | 78,120 | ||||

| (To record purchase of shares for cash) | |||||

Table (8)

- ■ Investments–Company AT Stock is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of cash paid to purchase Company AT’s stock.

Prepare journal entry for the dividend received from Company AP for 4,200 shares.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2017 | |||||

| June | 26 | Cash | 882 | ||

| Dividend Revenue | 882 | ||||

| (To record receipt of dividend revenue) | |||||

Table (9)

- ■ Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- ■ Dividend Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Compute amount of dividend received on Company AP’s stock.

Prepare journal entry for sale of 480 shares of Company AT at $60, with a brokerage of $50.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2017 | |||||

| July | 30 | Cash | 28,750 | ||

| Loss on Sale of Investments | 2,498 | ||||

| Investments–Company AT Stock | 31,248 | ||||

| (To record sale of shares) | |||||

Table (10)

- ■ Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- ■ Loss on Sale of Investments is an expense account. Since expenses and losses decrease equity, equity value is decreased, and a decrease in equity is debited.

- ■ Investments–Company AT Stock is an asset account. Since stock investments are sold, asset value decreased, and a decrease in asset is credited.

Working Notes:

Calculate the realized gain (loss) on sale of stock.

Step 1: Compute cash received from sale proceeds.

Step 2: Compute cost of stock investment sold.

Step 3: Compute realized gain (loss) on sale of stock.

Note: Refer to Steps 1 and 2 for value and computation of cash received and cost of stock investment sold.

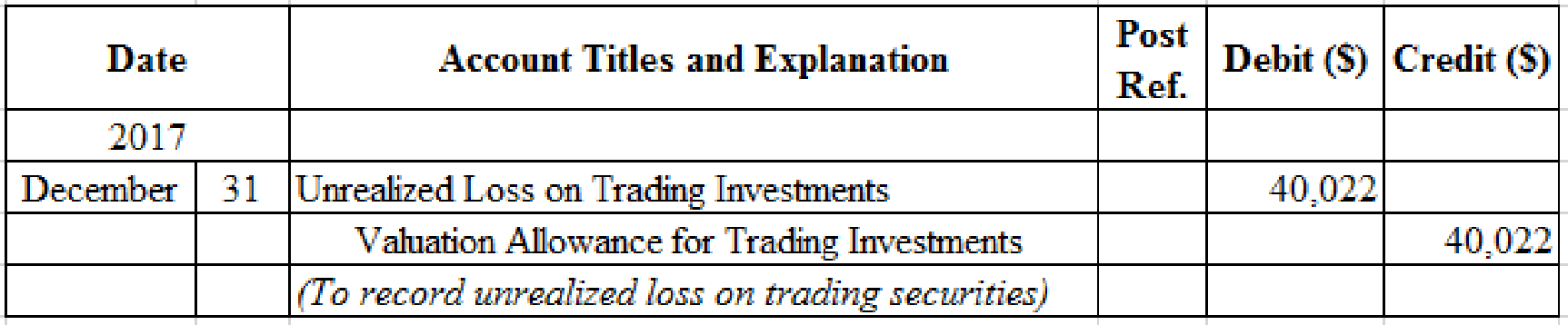

Prepare adjusting entry for valuation of trading securities transaction.

Figure (2)

- ■ Unrealized Loss on Trading Investments is an adjustment account used to report gain or loss on adjusting cost of investment at fair market value. Since loss has occurred and losses decrease stockholders’ equity value, and a decrease in stockholders’ equity value is debited.

- ■ Valuation Allowance for Trading Investments is a contra-asset account. The account is credited because the market price was decreased (loss).

Working Notes:

Compute the unrealized gain (loss) as on December 31, 2017.

| Details | Amount ($) |

| Unrealized loss as on December 31, 2017 | $12,032 |

| Add: Unrealized gain as on December 31, 2016 (From Table-7) | 27,990 |

| Unrealized loss on trading investments | $40,022 |

Table (11)

(2)

Indicate the presentation of trading investments on the current assets section of the balance sheet.

(2)

Explanation of Solution

Balance sheet presentation:

| Company Z | ||

| Balance Sheet (Partial) | ||

| December 31, 2017 | ||

| Assets | ||

| Current assets: | ||

| Trading investments (at cost) | $200,032 | |

| Less valuation allowance for trading investments | (12,032) | |

| Trading investments (at fair value) | $188,000 | |

Table (12)

(3)

Discuss the reporting of trading investments on the financial statements.

(3)

Explanation of Solution

Unrealized gain or loss is the result of change in trading investments cost and fair values, and reported as Other Revenues (Losses) on the income statement. The unrealized gain will be added to the net income and unrealized loss will be deducted from the net income. In 2016, Company Z would report $27,990 of unrealized gain as Other Income on the income statement. In the 2017, Company Z would report $40,022 of unrealized loss as Other Losses on the income statement.

Want to see more full solutions like this?

Chapter 15 Solutions

Financial Accounting

- On April 1, 2024, Sandhill Company purchased 46,400 common shares in Ecotown Ltd. for $13 per share. Management has designated the investment as FVTOCI. On December 5, Ecotown paid dividends of $0.10 per share and its shares were trading at $15 per share on December 31. Prepare the required entries to record the purchase, dividends, and year-end adjusting journal entry (if any) for this investment. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts. Record journal entries in the order presented in the problem. List all debit entries before credit entries.) Date Save for Later Account Titles Debit Credit Attempts: 0 of 1 used Submit Answerarrow_forwardOn July 1, 2016. Elm Company purchased cash eight P 1,000 , 9% bonds of Celebrity Corporation at P 100 plus accrued interest. The bond interest is paid semiannually each May 1 and November 1. The bond maturity date is November 1, 2017. Elm Company's annual reproting period ends December 31. Elm Company classifies this investment as trading security. At December 31, 2016 , Celebrity bonds were quoted at P 97. REQUIRED : a. Give tne entry for Elm Company to record the purchase of the bonds on July 1, 2016 b. Give the entry to record the interest collected during 2016.arrow_forwardPina Colada Corp. has the following portfolio of securities acquired for trading purposes and accounted for using the FV-NI model at September 30, 2023, the end of the company's third quarter: Investment Cost Fair Value 50,500 common shares of Yuen Inc. $313,100 $202,000 3,800 preferred shares of Monty Ltd. 1,650 common shares of Oakwood Inc. 144,400 152,000 148,500 147,675 On October 8, 2023, the Yuen shares were sold for $6.20 per share. On November 16, 2023, 3,000 common shares of Patriot Corp. were purchased at $44.40 per share. Pina Colada pays a 1% commission on purchases and sales of all securities. At the end of the fourth quarter, on December 31, 2023, the fair values of the shares held were as follows: Monty $102,950; Patriot $118,250; and Oakwood $167,475. Pina Colada prepares financial statements every quarter. (a) Prepare the journal entries to record the sale, purchase, and adjusting entries related to the portfolio for the fourth quarter of 2023. (Credit account titles…arrow_forward

- The following selected transactions relate to investment activities of Ornamental Insulation Corporation during 2024. The company buys debt securities, intending to profit from short- term differences in price and maintaining them in an active trading portfolio. Ornamental's fiscal year ends on December 31. No investments were held by Ornamental on December 31, 2023. March 31 Acquired 8% Distribution Transformers Corporation bonds costing S 430,000 at face value. September 1 Acquired $990, 000 of American Instruments' 10% bonds at face value. September 30 Received semiannual interest payment on the Distribution Transformers bonds. October 2 Sold the Distribution Transformers bonds for $470,000. November 1 Purchased $1,550, 000 of M&D Corporation 6% bonds at face value. December 31 Recorded any necessary adjusting entry(s) relating to the investments. The market prices of the investments are American Instruments bonds S 943, 000 M&D Corporation bonds S 1,613,000 (Hint: Interest…arrow_forwardThe following selected transactions relate to investment activities of Ornamental Insulation Corporation during 2024. The company buys debt securities, intending to profit from short-term differences in price and maintaining them in an active trading portfolio. Ornamental's fiscal year ends on December 31. No investments were held by Ornamental on December 31, 2023. March 31 Acquired 8% Distribution Transformers Corporation bonds costing $520,000 at face value. September 1 Acquired $1,260,000 of American Instruments' 10% bonds at face value. September 30 Received semiannual interest payment on the Distribution Transformers bonds. October 2 Sold the Distribution Transformers bonds for $550,000. November 1 Purchased $2,000,000 of M&D Corporation 6% bonds at face value. December 31 Recorded any necessary adjusting entry(s) relating to the investments. The market prices of the investments are American Instruments bonds M&D Corporation bonds (Hint: Interest must be accrued.) Required: 1.…arrow_forwardThe following investment-related transactions were completed by the company during 2021: Purchased P3,000,000.00 of ABC Corporation 7% bonds, paying 102.5 plus accrued interest of P52,500.00. In addition, the company paid brokerage fee of P15,000.00. The company classified these bonds as a trading security. • Purchased 30,000 shares of XYZ Corporation ordinary shares at P125 per share plus brokerage fees of P28,500. The company classified this stock as available for sale. Received semi-annual interest on the ABC Corporation bonds. Sold 4,500 shares of XYZ Corporation at P132 per share. Sold P480,000 of ABC Corporation 7% bonds at 102, plus accrued interest of P2,790.00. Determine the current portion of the investments.arrow_forward

- The following selected transactions relate to investment activities of Ornamental Insulation Corporation during 2024. The company buys debt securities, intending to profit from short-term differences in price and maintaining them in an active trading portfolio. Ornamental's fiscal year ends on December 31. No investments were held by Ornamental on December 31, 2023. March 31 Acquired 8% Distribution Transformers Corporation bonds costing $518,008 at face value. September 1 Acquired $1,238,800 of American Instruments' 18% bonds at face value. September 38 Received semiannual interest payment on the Distribution Transformers bonds. October 2 Sold the Distribution Transformers bonds for $590,000. November 1 Purchased $1,950,088 of M&D Corporation 6% bonds at face value. December 31 Recorded any necessary adjusting entry(s) relating to the investments. The market prices of the investments are American Instruments bonds M&D Corporation bonds (Hint: Interest must be accrued.) Required: 1.…arrow_forwardOn January 1, 2017, KLM Company purchased bonds with faceamount of 5,000,000. The entity paid 4,600,000 plus transaction cost of 142,290. The bonds mature on December 31, 2019 and pay 6% interest annually on December 31 of each year with 8% effective yield. The bonds were quoted at 106.5 on December 31, 2017 and 108 on December 31, 2018. Assume that the business model in managing financial asset is to collect contractual cash flows that are solely for payment of principal and interest and also to sell the bonds in an open market. What is the balance of unrealized gain-OCI on December 31, 2017?arrow_forward(Equity Securities Entries) Aranda Corporation made the following cash purchases of securities during 2017, which is the first year in which Arantxa invested in securities.1. On January 15, purchased 10,000 shares of Sanchez Company’s common stock at $33.50 per share plus commission $1,980.2. On April 1, purchased 5,000 shares of Vicario Co.’s common stock at $52.00 per share plus commission $3,370.3. On September 10, purchased 7,000 shares of WTA Co.’s preferred stock at $26.50 per share plus commission $4,910.On May 20, 2017, Aranda sold 4,000 shares of Sanchez Company’s common stock at a market price of $35 per share less brokerage commissions, taxes, and fees of $3,850. The year-end fair values per share were Sanchez $30, Vicario $55, and WTA $28. In addition, the chief accountant of Aranda told you that the corporation plans to hold these securities for the long-term but may sell them in order to earn profits from appreciation in prices. The equity method of accounting is not…arrow_forward

- Presented below are selected transactions regarding investment for Cardinal Paz Corp. Cardinal Paz Corp. classified these investments as trading. Feb. 1, 2022 Purchased Sharapova Company ordinary shares, $100 par, 200 shares at a purchase price $37,600. April 1 Purchased government bond, 11 percent, due April 1, 2028, interest payable April 1 and October 1, 110 bonds of $1,000 par each (Assume: par bond) July 1 McGrath Company 12 percent bonds, par $50,000, dated March 1, 2022 purchased at $52,000, interest payable annually on March 1, due March 1, 2042. The fair value of the investment on December 31, 2022 were: Sharapova Company $31,800 Government bonds 124,700 McGrath Company bonds 58,600 Instructions a. Prepare journal entries that should be made in 2022 to record the purchase of these investments. b. Prepare journal entries to record the accrued interest on December 31, 2022 (Please ignore the amortization of premium) c. At the end of 2022, what entries (if any) would…arrow_forwardTanner-UNF Corporation acquired as a long-term investment $240 million of 6% bonds, dated July 1, on July 1, 2018. The market interest rate (yield) was 8% for bonds of similar risk and maturity. Tanner-UNF paid $200 million for the bonds. The company will receive interest semiannually on June 30 and December 31. Company management has classified the bonds as available-for-sale investments. As a result of changing market conditions, the fair value of the bonds at December 31, 2018, was $210 million. 1. Prepare any journal entry necessary for Tanner-UNF to report its investment in the December 31, 2018, balance sheet. 2. Suppose Moody's bond rating agency downgraded the risk rating of the bonds motivating Tanner-UNF to sell the investment on January 2, 2019, for $190 million. Prepare the journal entries necessary to record the sale, including updating the fair-value adjustment, recording any reclassification adjustment, and recording the sale PLEASE SHOW WORKarrow_forwardFF&T Corporation is a confectionery wholesaler that frequently buys and sells securities to meet various investment objectives. The following selected transactions relate to FF&T’s investment activities during the last twomonths of 2018. At November 1, FF&T held $48 million of 20-year, 10% bonds of Convenience, Inc., purchasedMay 1, 2018, at face value. Management has the positive intent and ability to hold the bonds until maturity.FF&T’s fiscal year ends on December 31.Nov. 1 Received semiannual interest of $2.4 million from the Convenience, Inc., bonds.Dec. 1 Purchased 12% bonds of Facsimile Enterprises at their $30 million face value, to be held untilthey mature in 2024. Semiannual interest is payable May 31 and November 30.31 Purchased U.S. Treasury bills to be held until they mature in two months for $8.9 million.31 Recorded any necessary adjusting entry(s) relating to the investments.The fair values of the investments at December 31 were:Convenience bonds $44.7…arrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning