Videos

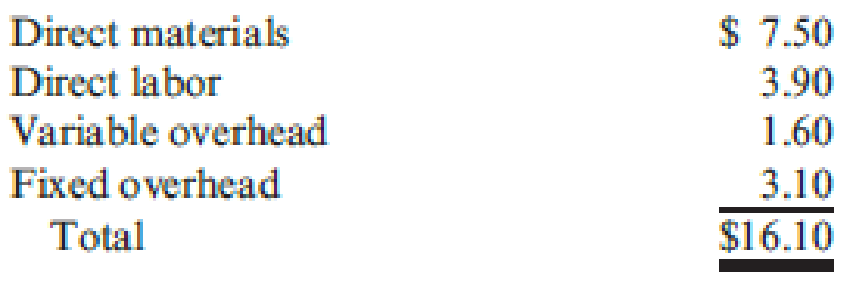

Feinan Sports, Inc., manufactures sporting equipment, including weight-lifting gloves. A national sporting goods chain recently submitted a special order for 4,600 pairs of weight-lifting gloves. Feinan Sports was not operating at capacity and could use the extra business. Unfortunately, the order’s offering price of $12.80 per pair was below the cost to produce them. The controller was opposed to taking a loss on the deal. However, the personnel manager argued in favor of accepting the order even though a loss would be incurred; it would avoid the problem of layoffs and would help maintain the community image of the company. The full cost to produce a pair of weight-lifting gloves is presented below.

No variable selling or administrative expenses would be associated with the order. Non-unit-level activity costs are a small percentage of total costs and are therefore not considered.

Required:

- 1. Assume that the company would accept the order only if it increased total profits. Should the company accept or reject the order? Provide supporting computations.

- 2. Suppose that Feinan Sports has negotiated with the potential customer, and has determined that it can substitute cheaper materials, reducing direct materials cost by $0.95 per unit. In addition, the company’s engineers have found a way to reduce direct labor cost by $0.50 per unit. Should the company accept or reject the order? Provide supporting computations.

- 3. Consider the personnel manager’s concerns. Discuss the merits of accepting the order even if it decreases total profits.

Trending nowThis is a popular solution!

Chapter 17 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Feinan Sports, Inc., manufactures sporting equipment, including weight- lifting gloves. A national sporting goods chain recently submitted a special order for 4,600 pairs of weight-lifting gloves. Unfortunately, the order's offering price of $14.80 per pair was far below the regular price of $25, and even below the cost of production. One marketing manager was opposed to taking a loss on the deal. However, the personnel manager argued in favor of accepting the order even though a loss would be incurred; it would avoid the problem of layoffs and would help maintain the community image of the company. The full cost to produce and sell a regular pair of weight-lifting gloves is presented below. Direct material Direct labor Variable overhead Fixed overhead Variable selling and adm. Total 7.5 3.9 1.6 3.1 2.8 18.9 No variable selling or administrative expenses would be associated with the special order. Required: (You must Provide supporting computations.) 1. Assume that the company has…arrow_forwardSTARTOM Inc, manufactures sporting equipment, including weight-lifting gloves. Anationalsporting goods chain recently submitted a special order for 4,600 pairs of weight-lifting gloves. STARTOM JnC.was not operating at capacity and couldusethe extra business. Unfortunately, the order's offering price of $12.80 per pair was below the costto produce them. The controller was opposedto takingaloss onthe deal. However, the personnel manager arguedin favor of accepting the order even though a loss would be incurred; it would avoid the problem of layoffs andwouldhelp maintainthe community image of the company. The full costto produce a pair of weight-lifting gloves is presented as follows: Direct materials - S7.50; Direct labor- $3.90; Variable overhead -$1.60; Fixed overhead - $3.10; Total - $16.10. No variable and selling or administrative expenses would be associated with the order. Non-unit level activity costs are a small percentage oftotal costs and are therefore not censidered Assume…arrow_forwardTania Company manufactures watches. A national sporting goods chain recently submitted a special order for 4,000 sport watches. Tania was not operating at capacity and could use the extra business. Unfortunately, the order’s offering price of RM17 per watch was below the cost to produce the watches. The controller did not agree to take a loss on the deal. However, the personnel manager argued in favor of accepting the order even though a loss would be incurred: it would avoid the problems of layoff and would help maintain the community image of the company. The following information is the full cost to produce a sport watch: Rewuired: i) List the relevant costs of the two alternatives of the special order. ii) Propose whether operating income increase or decrease if the order is accepted with calculation details.arrow_forward

- Tania Company manufactures watches. A national sporting goods chain recentlysubmitted a special order for 4,000 sport watches. Tania was not operating at capacityand could use the extra business. Unfortunately, the order’s offering price of RM17 perwatch was below the cost to produce the watches. The controller did not agree to take aloss on the deal. However, the personnel manager argued in favor of accepting theorder even though a loss would be incurred: it would avoid the problems of layoff andwould help maintain the community image of the company. The following informationis the full cost to produce a sport watch:Table 6: Production CostsDetails Unit CostRMDirect materials 6.50Direct labor 5.00Variable overhead 3.25Fixed overhead 2.50Total 17.25 List the relevant costs of the two alternatives of the special order. (ii) Propose whether operating income increase or decrease if the order is acceptedarrow_forwardFusion Metals Company is considering the elimination of its Packaging Department. Management has received an offer from an outside firm to supply all Fusion’s packaging needs. To help her in making the decision, Fusion’s president has asked the controller for an analysis of the cost of running Fusion’s Packaging Department. Included in that analysis is $9,100 of rent, which represents the Packaging Department’s allocation of the rent on Fusion’s factory building. If the Packaging Department is eliminated,the space it used will be converted to storage space. Currently Fusion rents storage space in a nearby warehouse for $11,000 per year. The warehouse rental would no longer be necessary if the Packaging Department were eliminated. Required:1. Discuss each of the figures given in the exercise with regard to its relevance in the departmentclosing decision.2. What type of cost is the $11,000 warehouse rental, from the viewpoint of the costs of the Packaging Department?arrow_forwardI keep working this problem over and over and been working on it but cant seem to get it right [The following information applies to the questions displayed below.] Hult Games buys electronic components for manufacturing from two suppliers, Milan Components and Dundee Parts. If the components are delivered late, the shipment to the customer is delayed. Delayed shipments lead to contractual penalties that call for Hult to reimburse a portion of the purchase price to the customer. During the past quarter, the purchasing and delivery data for the two suppliers showed the following. Milan Dundee Total Total purchases (cartons) 98,000 42,000 140,000 Average purchase price (per carton) $ 20.00 $ 22 $ 20.60 Number of deliveries 80 20 100 Percentage of late deliveries 25 % 10 % 22 % The Accounting Department recorded $602,700 as the cost of late deliveries to customers. Required: Assume that the average quality,…arrow_forward

- Dylan Engineering Corporation has a contract with Marley Stores to provide customized software for Marley's inventory control system. Cliff Outlets, Inc., Marley's competitor, pays $2,500 to Costello, a Dylan subcontractor, who is writing code for the Marley software, to delay delivery of the code for one week. As a result, Dylan's delivery of the software to Marley is delayed, and Marley sustains $100,000 in lost profits. On what ground could Marley recover damages from Cliff? What would Marley have to prove to win their case? Fully discuss, including explaining what must be proven to establish any legal theories and how such issues are most likely to be resolved in court.arrow_forward[The following information applies to the questions displayed below.] Watko Entertainment Systems (WES) buys audio and video components for assembling home entertainment systems from two suppliers, Bacon Electronics and Hessel Audio and Video. The components are delivered in cartons. If the cartons are delivered late, the installation for the customer is delayed. Delayed installations lead to contractual penalties that call for WES to reimburse a portion of the purchase price to the customer. During the past quarter, the purchasing and delivery data for the two suppliers showed the following: Bacon Hessel Total Total purchases (cartons) 5,000 3,000 8,000 Average purchase price (per carton) $ 190 $ 206 $ 196 Number of deliveries 40 20 60 Percentage of cartons delivered late. 30% 15% 25% The Accounting Department recorded $263,250 as the cost of late deliveries to customers. Required: Assume that the average quality, measured by the percentage of late deliveries,…arrow_forwardMicron Manufacturing produces electronic equipment. This year, it produced 7,500 oscilloscopes at a manufacturing cost of $300 each. These oscilloscopes were damaged in the warehouse during storage and, while usable, cannot be sold at their regular selling price of $500 each. Management has investigated the matter and has identified three alternatives for these oscilloscopes. 1. They can be sold as is to a wholesaler for $75 each. 2. They can be disassembled at a cost of $400,000 and the parts sold to a recycler for $130 each. 3. They can be reworked and turned into good units. The cost of reworking the units will be $3,200,000, after which the units can be sold at their regular price of $500 each. Required Which alternative should management pursue? Show analysis for each alternative.arrow_forward

- Finerly Corporation sells cosmetics through a network of independent distributors. Finerly shipped cosmetics to its distributors and is considering whether it should record $300,000 of revenue upon shipment of a new line of cosmetics. Finerly expects the distributors to be able to sell the cosmetics, but is uncertain because it has little experience with selling cosmetics of this type. Finerly is committed to accepting the cosmetics back from the distributors if the cosmetics are not sold. How much revenue should Finerly recognize upon delivery to its distributors?arrow_forwardGamma Company produces cars. Two of the profit centers, Tires center and Assembly center, were in conflict over the price of tires. External suppliers of tires offered Rania, the manager of the Assembly center, the same type and quality of tire for $200. Rania used to buy these tires internally for $300 each. Jamil the CEO of the company called for a meeting with the managers of both centers in order to solve the issue. Kamil the manager of the Tires Centre explained that: "The tires we produce have been a trusted brand for over 60 years and are distributed by Gamma Company to members all over the globe. Our tires have long been recognized as a leading private brand since 1954." Tires Center: Cost per tire 2$ Direct materials 95 Direct labor 54 Variable overheads 25arrow_forwardWatko Entertainment Systems (WES) buys audio and video components for assembling home entertainment systems from two suppliers, Bacon Electronics and Hessel Audio and Video. The components are delivered in cartons. If the cartons are delivered late, the installation for the customer is delayed. Delayed installations lead to contractual penalties that call for WES to reimburse a portion of the purchase price to the customer. During the past quarter, the purchasing and delivery data for the two suppliers showed the following: Bacon Hessel Total Total purchases (cartons) 5,000 3,000 8,000 Average purchase price (per carton) $ 170 $ 186 $ 176 Number of deliveries 40 20 60 Percentage of cartons delivered late. 30% 15% 25% The Accounting Department recorded $243,750 as the cost of late deliveries to customers. Required: Assume that the average quality, measured by the percentage of late deliveries, and prices from the two companies will continue as in the past. Also…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning