Concept explainers

Videos

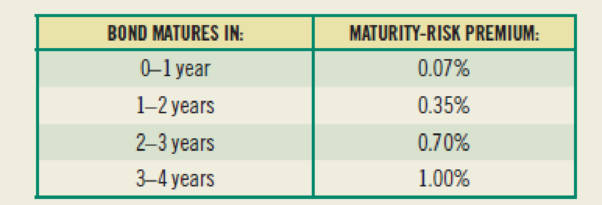

(Interest rate determination) You’re looking at some corporate bonds issued by Ford, and you are trying to determine what the nominal interest rate should be on them. You have determined that the real risk-free interest rate is 3.0%, and this rate is expected to continue on into the future without any change. In addition, inflation is expected to be constant over the future at a rate of 3.0%. The default-risk premium is also expected to remain constant at a rate of 1.5%, and the liquidity-risk premium is very small for Ford bonds, only about 0.02%. The maturity-risk premium is dependent on how many years the bond has to maturity. The maturity-risk premiums are as follows:

Given this information, what should the nominal rate of interest on Ford bonds maturing in 0–1 year, 1–2 years, 2–3 years, and 3–4 years be?

Want to see the full answer?

Check out a sample textbook solution

Chapter 2 Solutions

Foundations Of Finance

Additional Business Textbook Solutions

Principles of Managerial Finance (14th Edition) (Pearson Series in Finance)

Corporate Finance (4th Edition) (Pearson Series in Finance) - Standalone book

Gitman: Principl Manageri Finance_15 (15th Edition) (What's New in Finance)

Corporate Finance

Financial Accounting, Student Value Edition (4th Edition)

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

- The outstanding bonds of Winter Tires Inc. provide a real rate of return of 3.2 percent. If the current rate of inflation is 2.1 percent, what is the actual nominal rate of return on these bonds?arrow_forwardSuppose the real risk-free rate is 2.5%, the average future inflation rate is 2.3%, a maturity premium of 0.07% per year to maturity applies, i.e., MRP = 0.07% (t), where t is the years to maturity. Suppose also that a liquidity premium of 1% and a default risk premium of 0.7% applies to A-rated corporate bonds. How much higher would the rate of return be on a 7-year A-rated corporate bond than on a 5-year Treasury bond. Here we assume that the pure expectations theory is NOT valid. O 1.84% O 1.64% O 1.44% O 1.24% 1.04%arrow_forwardSuppose the real risk-free rate of interest is r=4% and it is expected to remain constant over time. Inflation is expected to be 1.60% per year for the next two years and 3.90% per year for the next three years. The maturity risk premium is 0.1 x (t-1) %, where t is number of years to maturity, a liquidity premium is 0.45%, and the default risk premium for a corporate bond is 1.40%, The average inflation during the first 4 years is What is the yield on a 4-year Treasury bond? O 6.75% O 8.90% O 4.30% O 7.05% What is the yield on a 4-year BBB-rated bond? O 7.50% O 7.05 % O 8.45% 8.90% If the yield on a 5-year Treasury bond is 7.38% and the yield on a 6-year Treasury bond is 7.83%, the expected inflation in 6 years is (Hint: Do not round intermediate calculations.)arrow_forward

- Assume the following: The real risk-free rate, r*, is expected to remain constant at 3%. Inflation is expected to be 3% next year and then to be constant at 2% a year thereafter. The maturity risk premium is zero. Given this information, which of the following statements is CORRECT? a. A 5-year corporate bond must have a lower yield than a 7-year Treasury security. b. The yield curve for U.S. Treasury securities will be upward sloping. c. A 5-year corporate bond must have a lower yield than a 5-year Treasury security. d. The real risk-free rate cannot be constant if inflation is not expected to remain constant. e. This problem assumed a zero maturity risk premium, but that is probably not valid in the real world.arrow_forwardThe rate of return that you would earn if you bought a bond and held it to its maturity date is called the bond’s yield to maturity, or YTM. If interest rates in the economy rise after a bond has been issued, what will happen to the bond’s price and to its YTM? Does the length of time to maturity affect the extent to which a given change in interest rates will affect the bond’s price?arrow_forwardPlease kindly assist d & e. Thank you. Two bonds A and B have the same credit rating, the same par value and the same coupon rate. Bond A has 30 years to maturity and bond B has five (5) years to maturity. Please demonstrate your understanding of interest rates risk by answering the following questions :a. Discuss which bond will trade at a higher price in the marketb. Discuss what happens to the market price of each bond if the interest rates in the economy go up.c. Which bond would have a higher percentage price change if interest rates go up?d. Please substantiate your argument with numerical examples.e. As a bond investor, if you expect a slowdown in the economy over the next 12 months, what would be your investment strategy? Provide your explanations and definitions in detail and be precise.arrow_forward

- Two bonds, A and B, have the same credit rating, the same par value, and the same coupon rate. Bond A has 30 years to maturity and bond B has 5 years to maturity. Please demonstrate your understanding of interest rate risk by answering the following questions : Discuss which bond will trade at a higher price in the market. Discuss what happens to the market price of each bond if the interest rates in the economy go up. Which bond would have a higher percentage price change if interest rates go up? Please substantiate your argument with numerical examples. As a bond investor, if you expect a slowdown in the economy over the next 12 months, what would be your investment strategy?arrow_forwardGive typing answer with explanation and conclusion Consider the prevailing condition of inflation (including changes in global oil price), the economy, budget deficit, decreases in expected remittance inflow, and the central bank monetary policy that could affect interest rate. Based on the prevailing conditions do you think bond price will increase or decreases in next six-month period. In the real economic environment which other factors may affect the bond price? Which factor in your opinion will have biggest impact on bond price? Assess the above given situations.arrow_forwardThe yield on two-year government bonds is 4.5%, and one-year government bonds provide a yield of 3%. In addition, the real risk-free interest rate (r*) is 1%, and the maturity risk premium is 0. 1) According to the theory of expectation, what is the rate of return on annual government bonds from now to later? Calculate the rate of return using the geometric mean. 2) What are the expected inflation rates for the first and second years respectively?arrow_forward

- Suppose you are considering two possible investment opportunities: a 12-year Treasury bond and a 7-year, A-rated corporate bond. The current real risk-free rate is 3%, and inflation is expected to be 2% for the next 2 years, 3% for the following 4 years, and 4% thereafter. The maturity risk premium is estimated by this formula: MRP = 0.02(t - 1)%. The liquidity premium (LP) for the corporate bond is estimated to be 0.3%. You may determine the default risk premium (DRP), given the company's bond rating, from the following table. Remember to subtract the bond's LP from the corporate spread given in the table to arrive at the bond's DRP. Corporate Bond Yield Rate Spread = DRP + LP U.S. Treasury 0.83 % — AAA corporate 1.03 0.20 % AA corporate 1.39 0.56 A corporate 1.79 0.96 What yield would you predict for each of these two investments? Round your answers to three decimal places. 12-year Treasury yield: fill in the blank _ % 7-year Corporate yield: fill…arrow_forwardIn this problem we are going to calculate bond prices and returns Suppose that the yield on a 3 year note is 2.5%. a) Calculate the price of the 3 year note (face value = $1000) with three annual coupon payments (after year 1, after year 2, after year 3) of $30, i.e., the coupon rate is 3.0%. b) Is this note selling at a discount or premium? Explain. Suppose that after one year and after you receive one coupon payment, you decide to sell your note. Your note is now a two year note with one coupon payment after 1 year and another after year 2. Consider the following two scenarios: Scenario #1 - interest rates on what is now a two year note (i.e., your note) have fallen to 1.00% Scenario #2 - interest rates on what is now a two year note (i.e., your note) have risen to 4% c) given scenan d) Calculate the price that you can sell your note for under scenario #1 and the associated rate of return when you sell your note Calculate the price that you can sell your note for under scenario #2…arrow_forwardTwo bonds A and B have the same credit rating, the same par value and the same coupon rate. Bond A has 30 years to maturity and bond B has five (5) years to maturity. Please demonstrate your understanding of interest rates risk by answering the following questions : Discuss which bond will trade at a higher price in the market Discuss what happens to the market price of each bond if the interest rates in the economy go up. Which bond would have a higher percentage price change if interest rates go up? Please substantiate your argument with numerical examples. As a bond investor, if you expect a slowdown in the economy over the next 12 months, what would be your investment strategy? note: all answers neededarrow_forward

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education