Concept explainers

Videos

Cost Allocation and Regulated Prices

The City of Imperial Falls contracts with Evergreen Waste Collection to provide solid waste collection to households and businesses. Until recently, Evergreen had an exclusive franchise to provide this service in Imperial Falls, which meant that other waste collection firms could not operate legally in the city. The price per pound of waste collected was regulated at 20 percent above the

Cost data for the most recent year of operations for Evergreen are as follows:

Data on customers for the most recent year are:

The City Council of Imperial Falls is considering allowing other private waste haulers to collect waste from businesses, but not from households. Service to businesses from other waste collection firms would not be subject to price regulation. Based on information from neighboring cities, the price that other private waste collection firms will charge is estimated to be $0.04 per pound (= $80 per ton).

Evergreen’s CEO has approached the city council with a proposal to change the way costs are allocated to households and businesses, which will result in different rates for households and businesses. She proposes that administrative costs and truck operating costs be allocated based on the number of customers and the other collection costs be allocated based on pounds collected. The total costs allocated to households would then be divided by the estimated number of pounds collected from households to determine the cost of collection. The rate would then be 20 percent above the cost. The rate for businesses would be determined using the same calculation.

Required

- a. Based on cost data from the most recent year, what is the price per pound charged by Evergreen for waste collection under the current system (the same rate for both types of customers)?

- b. Based on cost and waste data from the most recent year, what would be the price per pound charged to households and to businesses by Evergreen for waste collection if the CEO’s proposal were accepted?

- c. As a staff member to one of the council members, would you support the proposal to change the way costs are allocated? Explain.

a.

Calculate the price per pound charged by Company E for waste collection under the current system.

Answer to Problem 71P

The price per pound is $0.075 for waste collection under the current system.

Explanation of Solution

Price of the unit:

Price of a unit is the amount per unit that is charged by the customer to generate the sales of the business. It is calculated above the cost of the product in order to generate sales.

Calculate the price per pound:

Thus, the price per pound is $0.075 for waste collection under the current system. The premium on rate is 20%. So the net premium rate is 1.2.

Working note 1:

Calculate the average cost per pound:

Working note 2:

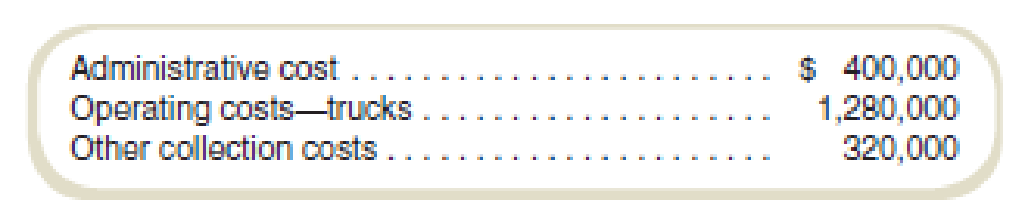

Calculate the total cost of collection:

| Particulars | Amount |

| Administrative cost | $400,000 |

| Operating costs—trucks | $1,280,000 |

| Other collection costs | $320,000 |

| Total cost of collection | $2,000,000 |

Table: (1)

Working note 3:

Calculate the total waste collection:

| Particulars | Amount |

| Waste collection of household | 4,000 |

| Waste collection of businesses | 12,000 |

| Total waste collection (tons) | 16,000 |

Table: (2)

Thus, the total waste collection is 16,000 tons. It will be $32,000,000 in the pound. One ton is equal to 2000 pound.

b.

Calculate the price per pound charged to households and businesses by Evergreen for waste collection if the CEO’s proposal were accepted.

Answer to Problem 71P

The price per pound is $0.21 and $0.03 for household and business respectively that should be charged to households and businesses by Evergreen for waste collection if the CEO’s proposal were accepted.

Explanation of Solution

Price of the unit:

Price of a unit is the amount per unit that is charged by the customer to generate the sales of the business. It is calculated above the cost of the product in order to generate sales.

Calculate the price per pound:

| Particulars | Household | Businesses |

| Customer cost | $1,344,000 (1) | $336,000 (2) |

| Other cost | $80,000(3) | $240,000 (4) |

| Total cost | $1,424,000 | $576,000 |

|

Total number of pound | 8,000,000 | 24,000,000 |

| Average cost per pound | $0.178 | $0.024 |

| Price premium (1.2) | 1.20 | 1.20 |

| Net price | $0.21 | $0.03 |

Table: (1)

Thus, the net price is $0.21 and $0.03 for household and business respectively.

Working note 1:

Calculate the customer cost for a household:

Working note 2:

Calculate the customer cost for businesses:

Working note 3:

Calculate the other cost for household:

Working note 4:

Calculate the other cost for businesses:

c.

Give opinion on the change in the cost allocation.

Explanation of Solution

Allocation of cost:

Allocation of cost refers to the cost of distribution of the common cost among the various departments on the basis of the resource utilized by the department.

Opinion on cost allocation:

Cost allocation can play a very important in price determination. Price in the first allocation was $0.075, and it was $0.24 in the second allocation. Second cost allocation allows the business to evaluate the cost of each unit (businesses and household). In future reference, this allocation can be used as it will calculate all the variables of each unit.

Thus, if there is any bottleneck in any of the unit, then it can be identified by the second allocation of cost.

Want to see more full solutions like this?

Chapter 2 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- A company uses charging rates to allocate service department costs to the using departments. The accountant compiled the following information on one of the service departments: If Department K plans to use 1,350 hours of the service departments service in the coming year, how much of the service departments cost is allocated to Department K? a. 3,375 b. 27,300 c. 26,325 d. 23,950arrow_forwardRequired information [The following information applies to the questions displayed below.) Jorgansen Lighting, Incorporated, manufactures heavy-duty street lighting systems for municipalities. The company uses variable costing for internal management reports and absorption costing for external reports to shareholders, creditors, and the government. The company has provided the following data: Inventories Year 1 Year 2 Variable costing net operating income Add (deduct) fixed manufacturing overhead deferred in (released from) inventory under absorption costing Absorption costing net operating income Beginning (units) 210 150 Ending (units) Variable costing net operating income $ 290,000 The company's fixed manufacturing overhead per unit was constant at $560 for all three years. 150 200 $ 269,000 Year 31 200 240 $ 260,000 Required: 1. Calculate each year's absorption costing net operating income. (Enter any losses or deductions as a negative value.) Reconciliation of Variable Costing and…arrow_forwardRequired information [The following information applies to the questions displayed below.] Jorgansen Lighting, Incorporated, manufactures heavy-duty street lighting systems for municipalities. The company uses variable costing for internal management reports and absorption costing for external reports to shareholders, creditors, and the government. The company has provided the following data: Inventories Beginning (units) Year 1 210 160 $ 300,000 Year 2 Variable costing net operating income Add (deduct) fixed manufacturing overhead deferred in (released from) inventory under absorption costing Absorption costing net operating income 160 180 $ 279,000 Year 3 Ending (units) Variable costing net operating income The company's fixed manufacturing overhead per unit was constant at $550 for all three years. Reconciliation of Variable Costing and Absorption Costing Net Operating Incomes Year 1 Year 2 Year 3 180 220 $ 260,000 Required: 1. Calculate each year's absorption costing net operating…arrow_forward

- Required information [The following information applies to the questions displayed below.] Jorgansen Lighting, Incorporated, manufactures heavy-duty street lighting systems for municipalities. The company uses variable costing for internal management reports and absorption costing for external reports. The company provided the following data: Inventories Beginning (units) Ending (units) Variable costing net operating income Year 1 Year 2 Year 3 220 150 150 180 180 220 $ 290,000 $ 279,000 $ 250,000 The company's fixed manufacturing overhead per unit was constant at $550 for all three years. Required: 1. Calculate each year's absorption costing net operating income. Note: Enter any losses or deductions as a negative value. Reconciliation of Variable Costing and Absorption Costing Net Operating Incomes Variable costing net operating income Add (deduct) fixed manufacturing overhead deferred in (released from) inventory under absorption costing Absorption costing net operating income Year 1…arrow_forwardThe Westfield branch of Security Home Bank submitted the following cost data for last year: Teller wages Assistant branch manager salary Branch manager salary Total Virtually all other costs of the branch-rent, depreciation, utilities, and so on-are organization-sustaining costs that cannot be meaningfully assigned to individual customer transactions such as depositing checks. In addition to the cost data above, the employees of the Westfield branch were interviewed concerning how their time was distributed last year across the activities included in the activity-based costing study. The results of those interviews appear below: Teller wages Assistant branch manager salary Branch manager salary $ 144,000 74,000 90,000 $ 308,000 Activity Opening accounts Processing deposits and withdrawals Processing other customer transactions Distribution of Resource Consumption Across Activities Processing Deposits and Withdrawals 75% 15% 0% Opening Accounts 4% 15% 4% Activity Cost Pool Opening…arrow_forwardRequired information [The following information applies to the questions displayed below.] Jorgansen Lighting, Incorporated, manufactures heavy-duty street lighting systems for municipalities. The company uses variable costing for internal management reports and absorption costing for external reports to shareholders, creditors, and the government. The company has provided the following data: Inventories Beginning (units) Year 1 Year 2 210 150 Ending (units) Variable costing net operating income $ 300,000 The company's fixed manufacturing overhead per unit was constant at $560 for all three years. Variable costing net operating income Add (deduct) fixed manufacturing overhead deferred in (released from) inventory under absorption costing Absorption costing net operating income 150 190 $ 279,000 Year 3 Reconciliation of Variable Costing and Absorption Costing Net Operating Incomes Year 1 Year 2 Year 3 Required: 1. Calculate each year's absorption costing net operating income. (Enter any…arrow_forward

- Required information [The following information applies to the questions displayed below.] Jorgansen Lighting, Inc., manufactures heavy-duty street lighting systems for municipalities. The company uses variable costing for internal management reports and absorption costing for external reports to shareholders, creditors, and the government. The company has provided the following data: Year 1 Year 2 Year 3 Inventories Beginning (units) 210 160 190 Ending (units) 160 190 230 Variable costing net operating income $290,000 $269,000 $260,000 The company’s fixed manufacturing overhead per unit was constant at $560 for all three years. rev: 03_09_2019_QC_CS-162392 Required: 1. Calculate each year’s absorption costing net operating income. (Enter any losses or deductions as a negative value.)arrow_forwardRequired information [The following information applies to the questions displayed below.] Jorgansen Lighting, Incorporated, manufactures heavy-duty street lighting systems for municipalities. The company uses variable costing for internal management reports and absorption costing for external reports to shareholders, creditors, and the government. The company has provided the following data: Year 1 Year 2 160 190 $ 279,000 O Increase O Decrease Year 3 Inventories. Beginning (units) Ending (units) 220 160 190 220 Variable costing net operating income i $ 290,000 $ 260,000 The company's fixed manufacturing overhead per unit was constant at $560 for all three years.. 2. Assume in Year 4 that the company's variable costing net operating income was $260,000 and its absorption costing net operating Income was $300,000. a. Did inventories increase or decrease during Year 4? b. How much fixed manufacturing overhead cost was deferred or released from inventory during Year 4? Fixed…arrow_forward[The following information applies to the questions displayed below.] Jorgansen Lighting, Inc., manufactures heavy-duty street lighting systems for municipalities. The company uses variable costing for internal management reports and absorption costing for external reports to shareholders, creditors, and the government. The company has provided the following data: Year 1 Year 2 Year 3 Inventories Beginning (units) 220 170 190 Ending (units) 170 190 220 Variable costing net operating income $290,000 $279,000 $250,000 The company’s fixed manufacturing overhead per unit was constant at $400 for all three years. Required: 1. Calculate each year’s absorption costing net operating income. (Enter any losses or deductions as a negative value.) Reconciliation of Variable Costing and Absorption Costing Net Operating Incomes Year 1 Year 2 Year 3 Variable costing net operating income Add (deduct) fixed manufacturing overhead…arrow_forward

- The following information applies to the questions displayed below.] Jorgansen Lighting, Inc., manufactures heavy-duty street lighting systems for municipalities. The company uses variable costing for internal management reports and absorption costing for external reports to shareholders, creditors, and the government. The company has provided the following data: Year 1 Year 2 Year 3 Inventories Beginning (units) 220 170 190 Ending (units) 170 190 220 Variable costing net operating income $290,000 $279,000 $250,000 The company’s fixed manufacturing overhead per unit was constant at $400 for all three years. 2. Assume in Year 4 that the company’s variable costing net operating income was $250,000 and its absorption costing net operating income was $270,000. a. Did inventories increase or decrease during Year 4? multiple choice Increase Decrease b. How much fixed manufacturing overhead cost was deferred or released from…arrow_forwardRequired information (The following information applies to the questions displayed below.] Jonas Materials Science (JMS) purchases its materials from several countries. As part of its cost-control program, JMS uses a standard cost system for all aspects of its operations, including purchases of direct materials. The company establishes standard costs for direct materials at the beginning of each fiscal year. Pat Butch, the purchasing manager, is happy with the result of the year just ended. He believes that the purchase price variance for direct materials for the year will be favorable and is very confident that his department has at least met the standard prices. The preliminary report from the controller's office confirms his jubilation. Following is a portion of the preliminary report: Total quantity purchased Average price per kilogran Standard price per kilogran 40,000 kilograms $50.00 $ 60.00 Budgeted quantity per quarter 5,000 kilograns In the fourth quarter, the purchasing…arrow_forward[The following information applies to the questions displayed below.] Jorgansen Lighting, Incorporated, manufactures heavy-duty street lighting systems for municipalities. The company uses variable costing for internal management reports and absorption costing for external reports to shareholders, creditors, and the government. The company has provided the following data: Year 1 Year 2 Year 3 Inventories Beginning (units) 210 160 180 Ending (units ) 160 180 230 Variable costing net operating income $300,000 $ 279,000 $ 260,000 The company's fixed manufacturing overhead per unit was constant at $560 for all three years. Required: 1. Calculate each year's absorption costing net operating income. Note: Enter any losses or deductions as a negative value.arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College