Videos

a

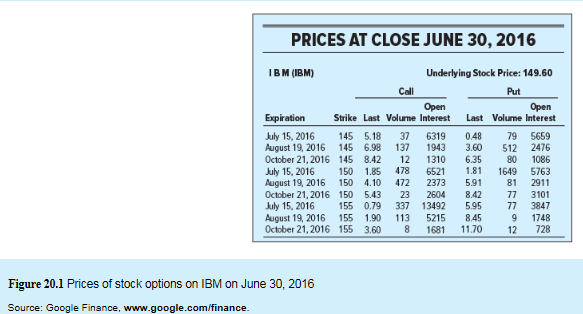

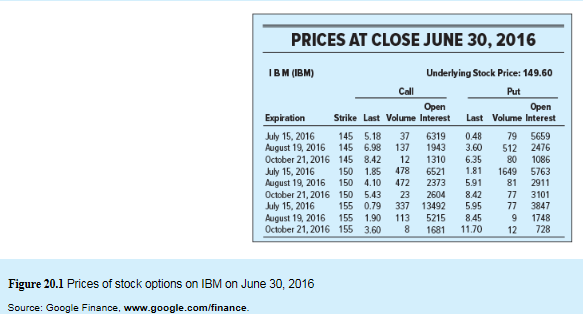

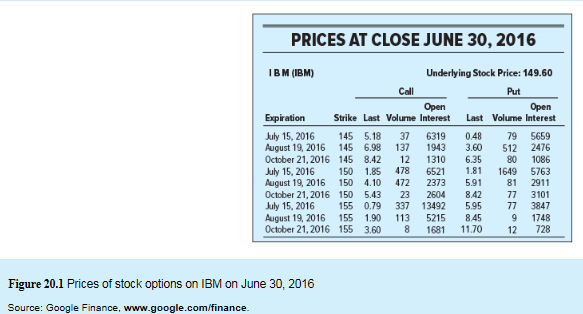

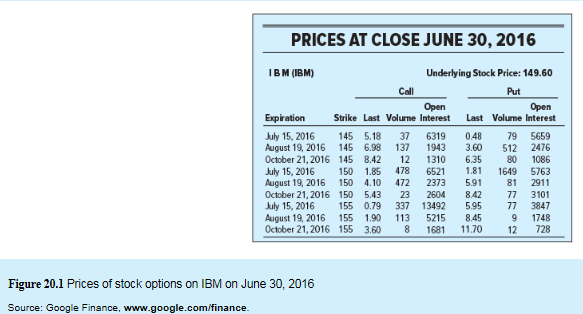

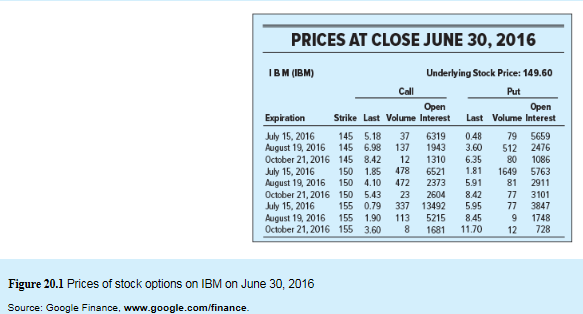

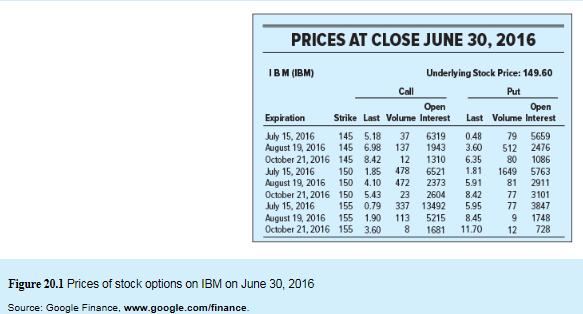

To compute: The payoff and the profit for investments when the call option’s exercise price X=$145 assuming that the stock price on the expiration date is $150.

Introduction:

Options: Options are the instruments used in financial transactions. These are derived based on the value of the underlying assets. Normally, the purpose of an option is to provide the buyer an opportunity to buy or sell the underlying asset depending upon the type of contract they possess. There are two types of options- Call option and put option.

a

Answer to Problem 5PS

The call buyer will incur loss of -$0.18 when the exercise price is $145.

Explanation of Solution

The information given to us is as follows:

Let us calculate the payoff when Call option X is $145 and stock price on expiry date is $150.

| Calculation of payoff in case of call option | ||

| Position | Stock price > X | Stock price is less than or equal to X |

| Payoff to call holder | Stock price -X | 0 |

| Payoff to call writer | -(Stock price -X) | 0 |

Stock price at expiration is $150.

Exercise or Strike price X=$145.

So, let us now substitute the values in the above table. We get

| Calculation of payoff in case of call option | ||

| Position | Stock price > X | Stock price is less than or equal to X |

| Payoff to call holder |  | 0 |

| Payoff to call writer |  | 0 |

By the above calculation, it is observed that the call writer is prepared to bear the risk in return of option premium as there is loss if stock price increases.

Calculation of profit for investment:

But as per the information given to us, the price of the call option is $5.18 at a strike price $145 on June 2016.

Therefore, the call buyer will incur loss of -$0.18.

b.

To compute: The payoff and the profit for investments when the put option’s exercise price X=$145 assuming that the stock price on the expiration date is $150.

Introduction:

Payoff: In financial terminology, payoff refers to the return on an investment.

b.

Answer to Problem 5PS

The loss incurred by the put buyer will be -$0.48 when the exercise price is $145.

Explanation of Solution

The information given to us is as follows:

Let us calculate the payoff when Put option X is $145 and stock price on expiry date is $150.

| Calculation of payoff in case of a put option | ||

| Position | If Stock price is less than X | If Stock price is greater or equal to X |

| Payoff to Put holder | X-Stock price | 0 |

| Payoff to Put writer | -(X-Stock price) | 0 |

Stock price at expiration is $150.

Exercise or Strike price X=$145.

So, let us now substitute the values in the above table. We get

| Calculation of payoff in case of a put option | ||

| Position | If Stock price is less than X | If Stock price is greater or equal to X |

| Payoff to Put holder | $0 | 0 |

| Payoff to Put writer | $0 | 0 |

But, we are informed that the put option is $0.48 at a strike price of $145 on June2016.

Therefore, the loss incurred by the buyer on put option will be -$0.48.

c

To compute: The payoff and the profit for investments when the call option’s exercise price X=$150 assuming that the stock price on the expiration date is $150.

Introduction:

Profit on investment: Investments are supposed to be considered as a monetary asset. Investments are done with an expectation to earn good income in future or to sell this asset at a higher price. If the purchase price of the asset is less than the sale price of the asset, it can be termed as profit on investment else it is loss on investment.

c

Answer to Problem 5PS

The call buyer will incur loss of -$1.85 when the exercise price is $150.

Explanation of Solution

The information given to us is as follows:

Let us calculate the payoff when Call option X is $150 and stock price on expiry date is $150.

| Calculation of payoff in case of call option: | ||

| Position | Stock price > X | Stock price is less than or equal to X |

| Payoff to call holder | Stock price -X | 0 |

| Payoff to call writer | -(Stock price -X) | 0 |

Stock price at expiration is $150.

Exercise or Strike price X=$150.

So, let us now substitute the values in the above table. We get

| Calculation of payoff in case of call option | ||

| Position | Stock price > X | Stock price is less than or equal to X |

| Payoff to call holder |  | 0 |

| Payoff to call writer |  | 0 |

By the above calculation, it is observed that the call writer is prepared to bear the risk in return of option premium as there is loss if stock price increases.

Calculation of profit for investment:

But as per the information given to us, the price of the call option is $1.85 at a strike price $150 on June 2016.

Therefore, the call buyer will incur loss of -$1.85.

d.

To compute: The payoff and the profit for investments when the put option’s exercise price X=$150 assuming that the stock price on the expiration date is $150.

Introduction:

Options: Options are the instruments used in financial transactions. These are derived based on the value of the underlying assets. Normally, the purpose of an option is to provide the buyer an opportunity to buy or sell the underlying asset depending upon the type of contract they possess. There are two types of options- Call option and put option.

d.

Answer to Problem 5PS

The incurred by the put buyer will be -$1.81 when the exercise price is $150.

Explanation of Solution

The information given to us is as follows:

Let us calculate the payoff when Put option X is $150 and stock price on expiry date is $150.

| Calculation of payoff in case of a put option | ||

| Position | If Stock price is less than X | If Stock price is greater or equal to X |

| Payoff to Put holder | X-Stock price | 0 |

| Payoff to Put writer | -(X-Stock price) | 0 |

Stock price at expiration is $150.

Exercise or Strike price X=$150.

So, let us now substitute the values in the above table. We get

| Calculation of payoff in case of a put option | ||

| Position | If Stock price is less than X | If Stock price is greater or equal to X |

| Payoff to Put holder | $0 | 0 |

| Payoff to Put writer | $0 | 0 |

But, we are informed that the put option is $1.81 at a strike price of $150 on June 2016.

Therefore, the loss incurred by the buyer on put option will be -$1.81.

e.

To compute: The payoff and the profit for investments when the call option’s exercise price X=$155 assuming that the stock price on the expiration date is $150.

Introduction:

Payoff: In financial terminology, payoff refers to the return on an investment.

e.

Answer to Problem 5PS

The loss incurred by the call buyer will be -$0.79 when the exercise price is $155.

Explanation of Solution

The information given to us is as follows:

Let us calculate the payoff when Call option X is $155 and stock price on expiry date is $150.

| Calculation of payoff in case of call option | ||

| Position | Stock price > X | Stock price is less than or equal to X |

| Payoff to call holder | Stock price -X | 0 |

| Payoff to call writer | -(Stock price -X) | 0 |

Stock price at expiration is $150.

Exercise or Strike price X=$155.

So, let us now substitute the values in the above table. We get

| Calculation of payoff in case of call option | ||

| Position | Stock price > X | Stock price is less than or equal to X |

| Payoff to call holder | 0 | 0 |

| Payoff to call writer | 0 | 0 |

By the above calculation, it is observed that the call writer is prepared to bear the risk in return of option premium as there is loss if stock price increases.

Calculation of profit for investment

But as per the information given to us, the price of the call option is $0.79 at a strike price $155 on June 2016.

Therefore, the call buyer will incur loss of -$0.79.

f.

To compute: The payoff and the profit for investments when the put option’s exercise price X=$155 assuming that the stock price on the expiration date is $150.

Introduction:

Loss on investment: Investments are supposed to be considered as a monetary asset. Investments are done with an expectation to earn good income in future or to sell this asset at a higher price. If the purchase price of the asset is less than the sale price of the asset, it can be termed as profit on investment else it is loss on investment.

f.

Answer to Problem 5PS

The loss incurred by the put buyer will be $-0.95 when the exercise price is $155.

Explanation of Solution

The information given to us is as follows:

Let us calculate the payoff when Put option X is $155 and stock price on expiry date is $150.

| Calculation of payoff in case of a put option | ||

| Position | If Stock price is less than X | If Stock price is greater or equal to X |

| Payoff to Put holder | X-Stock price | 0 |

| Payoff to Put writer | -(X-Stock price) | 0 |

Stock price at expiration is $150.

Exercise or Strike price X=$155.

So, let us now substitute the values in the above table. We get

| Calculation of payoff in case of a put option | ||

| Position | If Stock price is less than X | If Stock price is greater or equal to X |

| Payoff to Put holder |  | 0 |

| Payoff to Put writer |  | 0 |

But, we are informed that the put option is $5.95 at a strike price of $155 on June 2016.

Therefore, the loss incurred by the buyer on put option will be -0.95.

Want to see more full solutions like this?

Chapter 20 Solutions

EBK INVESTMENTS

- Required: Refer to Figure 15.1, which lists the prices of various Microsoft options. Use the data in the figure to calculate the payoff and the profit/loss for investments in each of the following November 2019 expiration options on a single share, assuming that the stock price on the expiration date is $138. (Loss amounts should be indicated by a minus sign. Round "Profit/Loss" to 2 decimal places.) ✓ Answer is complete but not entirely correct. Payoff Profit/Loss a. Call option, X = 135 $ 3.00 $ (3.78) b. Put option, X = 135 $ 0.00 $ (1.89) c. Call option, X = 140 $ 0.00 $ (1.50) X d. Put option, X = 140 $ 7.00 $ 0.35 xarrow_forwardAssume a stock with an option with the information as follows. • Stock purchased price was $113.• Call option on the stock was purchased at $4. • Call option has strike price at $115.• the stock price is $117on expiration date Please explain the Call Options Payoff Diagrams below, why it plot like this (please explain step by step) . Thank you for your answeringarrow_forwardRefer to the stock options on Microsoft in the Figure 2.10. Suppose you buy a November expiration call option on 100 shares with the excise price of $140. Required: a-1. If the stock price at option expiration is $144, will you exercise your call?a-2. What is the net profit/loss on your position? (Input the amount as a positive value.)a-3. What is the rate of return on your position? (Negative value should be indicated by a minus sign. Round your answer to 2 decimal places.) b-1. Would you exercise the call if you had bought the November call with the exercise price $135?b-2. What is the net profit/loss on your position? (Input the amount as a positive value.)b-3. What is the rate of return on your position? (Negative value should be indicated by a minus sign. Round your answer to 2 decimal places.)c-1. What if you had bought the November put with exercise price $140 instead? Would you exercise the put at a stock price of $140?c-2. What is the rate of return on your position? (Negative…arrow_forward

- 1) Draw the binomial tree listing only the option prices at each node. Assume the following data on a 6-month call option, using 3-month intervals as the time period. K = $40, S = $37.90, r = 5.0%, σ = 0.35 2) Draw the binomial tree listing only the stock prices at each node. Assume the following data on a 6-month call option, using 3-month intervals as the time period. K = $70, S = $68.50, r = 6.0%, σ = 0.32 3) Draw the binomial tree listing only the option prices at each node. Assume the following data on a 6-month put option, using 3-month intervals as the time period. K = $40.00, S = $37.90, r = 5.0%, σ = 0.35 4) Using a binomial tree explanation, explain the situation in which an American option would alter the pricing of an option.arrow_forwardAssume the following inputs for a call option: (1) current stock price is $31, (2) strike price is $35, (3) time to expiration is 2 months, (4) annualized risk-free rate is 3%, and (5) variance of stock return is 0.25. The data has been collected in the Microsoft Excel Online file below. Open the spreadsheet and perform the required analysis to answer the question below. Use the Black-Scholes model to find the price for the call option. Do not round intermediate calculations. Round your answer to the nearest cent.arrow_forwardRefer to Figure 15.1, which lists the prices of various Microsoft options. Use the data in the figure to calculate the payoff and the profit/loss for investments in each of the following November 2019 expiration options on a single share, assuming that the stock price on the expiration date is $143. (Loss amounts should be indicated by a minus sign. Round "Profit/Loss" to 2 decimal places.)arrow_forward

- Consider the following options portfolio. You write an August expiration call option on IBM with exercise price $150. You write an August IBM put option with exercise price $145.a. Graph the payoff of this portfolio at option expiration as a function of IBM’s stock price at that time.b. What will be the profit/loss on this position if IBM is selling at $153 on the option expiration date? What if IBM is selling at $160? c. At what two stock prices will you just break even on your investment?d. What kind of “bet” is this investor making; that is, what must this investor believe about IBM’s stock price to justify this position?arrow_forwardCall options on a stock are available with strike prices of $15, $17.5 and $20 before expiration date. The call premiums for each are $4, $2 and $0.5 respectively. Explain how the options can be used to create a butterfly spread. A. Construct a table showing how profit varies with stock price for the butterfly spread. B. Plot the profit with stock price for the butterfly spread. List the profit formula for each trend.arrow_forwardSuppose that both a call option and a put option have been written on a stock with an exerciseprice of $40. The current stock price is $42, and the call and put premiums are $3 and $0.75,respectively. Calculate the profit to positions of both the short call and the long put with an expiration day stock price of $43.arrow_forward

- Use the Black-Scholes formula to find the value of a call option based on the following inputs. (Round your final answer to 2 decimal places. Do not round intermediate calculations.) Stock price Exercise price Interest rate Dividend yield Time to expiration Standard deviation of stock's returns Call value GA $ $ $ 48 60 0.07 0.04 0.50 0.26arrow_forwardExcel Online Structured Activity: Black-Scholes Model Assume the following inputs for a call option: (1) current stock price is $29, (2) strike price is $36, (3) time to expiration is 5 months, (4) annualized risk-free rate is 4%, and (5) variance of stock return is 0.31. Use the Black-Scholes model to find the price for the call option. Do not round intermediate calculations. Round your answer to the nearest cent.arrow_forwardA PUT and a CALL option are written on a stock with a strikeprice of $60. The options are held until expiration. Suppose the stock price at expiration is $75. Call premium is $16 and Put premium is $3. The CALL option will ___ because the call is ___. But the PUT option will ___ because the put is ___, with a TIME VALUE of ___.a) Be exercised; in-the-money; not be exercised; out-of-the-money; zerob) not be exercised; out-of-the-money; be exercised; in-the-money; zeroc) Be exercised; in-the-money; not be exercised; out-of-the-money; 1d) Be exercised; in-the-money; be exercised; in-the-money; zeroe) None of the above is correctarrow_forward

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education