Concept explainers

Videos

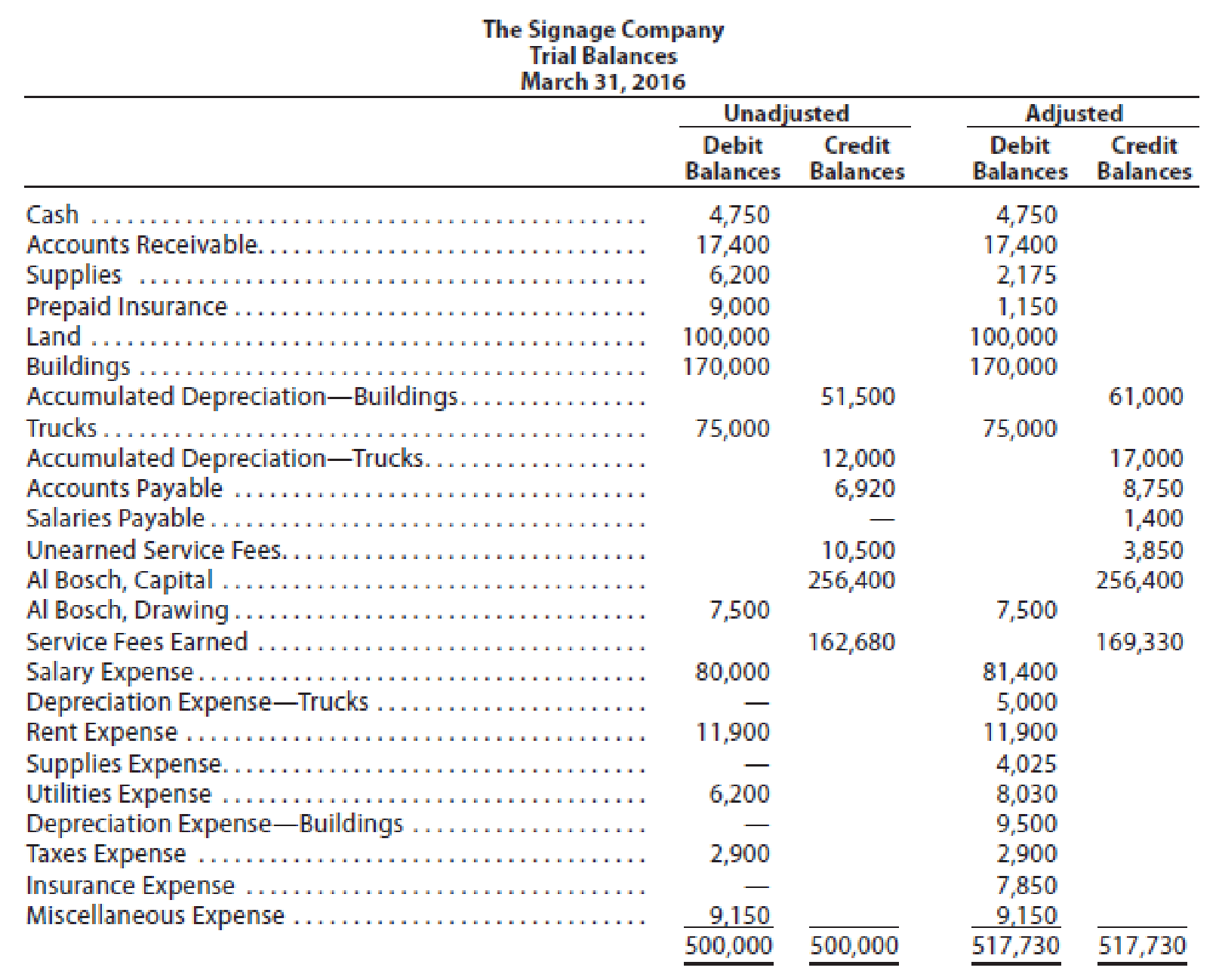

The Signage Company specializes in the maintenance and repair of signs, such as billboards. On March 31, 2016, the accountant for The Signage Company prepared the following

Instructions

Journalize the seven entries that adjusted the accounts at March 31. None of the accounts were affected by more than one

Prepare the adjusting entries in the books of Company S at the end of the year.

Explanation of Solution

Adjusting entries: Adjusting entries refers to the entries that are made at the end of an accounting period in accordance with revenue recognition principle, and expenses recognition principle. All adjusting entries affect at least one income statement account (revenue or expense), and one balance sheet account (asset or liability).

Rules of Debit and Credit:

Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and owner’s equities.

- Credit, all increase in liabilities, revenues, and owners’ equities, all decrease in assets, expenses.

An adjusting entry for Supplies expenses:

In this case, Company S recognized the supplies expenses at the end of the year. So, the necessary adjusting entry that the Company S should record to recognize the supplies expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Supplies expenses (1) | 4,025 | |||

| March | 31 | Supplies | 4,025 | ||

| (To record the supplies expenses incurred at the end of the year) | |||||

Table (1)

- Supplies expense decreased the value of owner’s equity by $4,025; hence debit the supplies expenses for $4,025.

- Supplies are an asset, and it decreased the value of asset by $4,025, hence credit the supplies for $4,025.

Working note (1):

Calculate the value of supplies expense.

An adjusting entry for insurance expenses:

In this case, Company S recognized the insurance expenses at the end of the year. So, the necessary adjusting entry that the Company S should record to recognize the prepaid expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Insurance expenses (2) | 7,850 | |||

| March | 31 | Prepaid insurance | 7,850 | ||

| (To record the insurance expenses incurred at the end of the year) | |||||

Table (2)

- Insurance expense decreased the value of owner’s equity by $7,850; hence debit the insurance expenses for $7,850.

- Prepaid insurance is an asset, and it decreased the value of asset by $7,850, hence credit the prepaid insurance for $7,850.

Working note (2):

Calculate the value of insurance expense.

An adjusting entry for depreciation expenses-Buildings:

In this case, Company S recognized the depreciation expenses on buildings at the end of the year. So, the necessary adjusting entry that the Company S should record to recognize the accrued expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Depreciation expenses –Buildings (3) | 9,500 | |||

| March | 31 | Accumulated depreciation-Buildings | 9,500 | ||

| (To record the depreciation expenses incurred at the end of the year) | |||||

Table (3)

- Depreciation expense decreased the value of owner’s equity by $9,500; hence debit the depreciation expenses for $9,500.

- Accumulated depreciation is a contra-asset account, and it decreased the value of asset by $9,500, hence credit the accumulated depreciation for $9,500.

Working note (3):

Calculate the value of depreciation expense-Equipment.

An adjusting entry for depreciation expenses-Trucks:

In this case, Company S recognized the depreciation expenses on trucks at the end of the year. So, the necessary adjusting entry that the Company S should record to recognize the accrued expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Depreciation expenses –Trucks(4) | 5,000 | |||

| March | 31 | Accumulated depreciation-Trucks | 5,000 | ||

| (To record the depreciation expenses incurred at the end of the year) | |||||

Table (4)

- Depreciation expense decreased the value of owner’s equity by $5,000; hence debit the depreciation expenses for $5,000.

- Accumulated depreciation is a contra-asset account, and it decreased the value of asset by $5,000, hence credit the accumulated depreciation for $5,000.

Working note (4):

Calculate the value of depreciation expense-Trucks.

An adjusting entry for utilities expenses:

In this case, Company S recognized the utilities expenses at the end of the year. So, the necessary adjusting entry that the Company S should record to recognize the accrued expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Utilities expenses (5) | 1,830 | |||

| March | 31 | Accounts payable | 1,830 | ||

| (To record the utilities expenses incurred at the end of the year) | |||||

Table (5)

- Utilities expense decreased the value of owner’s equity by $1,830; hence debit the utilities expenses for $1,830.

- Accounts payable is a liability, and it increased the value of liability by $1,830, hence credit the accounts payable for $1,830.

Working note (5):

Calculate the value of utilities expense.

An adjusting entry for salaries expenses:

In this case, Company S recognized the salaries expenses at the end of the year. So, the necessary adjusting entry that the Company S should record to recognize the accrued expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Salaries expenses (6) | 1,400 | |||

| March | 31 | Salaries payable | 1,400 | ||

| (To record the salaries expenses incurred at the end of the year) | |||||

Table (6)

- Salaries expense decreased the value of owner’s equity by $1,400; hence debit the salaries expenses for $1,400.

- Salaries payable is a liability, and it increased the value of liability by $1,400, hence credit the salaries payable for $1,400.

Working note (6):

Calculate the value of salaries expense.

An adjusting entry for unearned service fees:

In this case, Company S received cash in advance before the service provided to customer. So, the necessary adjusting entry that the Company S should record for the unearned fees revenue at the end of the year is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Unearned service fees | 6,650 | |||

| March | 31 | Service fees earned (7) | 6,650 | ||

| (To record the unearned service fees at the end of the year) | |||||

Table (7)

- Unearned service fees are a liability, and it decreased the value of liability by $6,650, hence debit the unearned service fees for $6,650.

- Service fees earned increased owner’s equity by $6,650; hence credit the service fees earned for $6,650

Working note (7):

Calculate the value of service fees earned.

Want to see more full solutions like this?

Chapter 3 Solutions

Financial Accounting

- After Bunker Hill Assay Services Inc. had completed all postings for March in the current year (2016), the sum of the balances in the following accounts payable ledger did not agree with the 37,600 balance of the controlling account in the general ledger: Assuming that the controlling account balance of 36,600 has been verified as correct, (a) determine the error(s) in the preceding accounts and (b) prepare a listing of accounts payable creditor balances (from the corrected accounts payable subsidiary ledger).arrow_forwardThe accounts receivable clerk for Waddell Industries prepared the following partially completed aging of receivables schedule as of the end of business on August 31: The following accounts were unintentionally omitted from the aging schedule and not included in the preceding subtotals: a. Determine the number of days past due for each of the preceding accounts as of August 31. b. Complete the aging of receivables schedule by adding the omitted accounts to the bottom of the schedule and updating the totals.arrow_forwardWig Creations Company supplies wigs and hair care products to beauty salons throughout Texas and the Southwest. The accounts receivable clerk for Wig Creations prepared the following partially completed aging of receivables schedule as of the end of business on December 31, 20Y1: The following accounts were unintentionally omitted from the aging schedule: Wig Creations has a past history of uncollectible accounts by age category, as follows: Instructions 1. Determine the number of days past due for each of the preceding accounts. 2. Complete the aging of receivables schedule by adding the omitted accounts to the bottom of the schedule and updating the totals. 3. Estimate the allowance for doubtful accounts, based on the aging of receivables schedule. 4. Assume that the allowance for doubtful accounts for Wig Creations has a credit balance of 7,375 before adjustment on December 31, 20Y1. Journalize the adjustment for uncollectible accounts. 5. Assuming that the adjusting entry in (4) was inadvertently omitted, how would the omission affect the balance sheet and income statement?arrow_forward

- The accounts receivable clerk for Kirchhoff Industries prepared the following partially completed aging of receivables schedule as of the end of business on August 31: The following accounts were unintentionally omitted from the aging schedule and not included in the preceding subtotals: a. Determine the number of days past due for each of the preceding accounts as of August 31. b. Complete the aging of receivables schedule by adding the omitted accounts to the bottom of the schedule and updating the totals.arrow_forwardPrior to recording the following, Elite Electronics, Incorporated, had a credit balance of $2,200 in its Allowance for Doubtful Accounts. Required: Prepare journal entries for each transaction. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field.) On August 31, a customer balance for $320 from a prior year was determined to be uncollectible and was written off. On December 15, the customer balance for $320 written off on August 31 was collected in full.arrow_forwardQuantum Solutions Company, a computer consulting firm, has decided to write off the $33,550 balance of an account owed by a customer, Alliance Inc. Journalize the entry to record the write-off, assuming that (a) the direct write-off method is used and (b) the allowance method is used.arrow_forward

- Quantum Solutions Company, a computer consulting firm, has decided to write off the $33,550 balance of an account owed by a customer, Alliance Inc. Required: On March 1, journalize the entry to record the write-off, assuming that (a) the direct write-off method is used and (b) the allowance method is used. Refer to the Chart of Accounts for exact wording of account titles.arrow_forwardPrior to recording the following, Elite Electronics, Inc., had a credit balance of $2,000 in its Allowance for Doubtful Accounts.Required:Prepare journal entries for each transaction.a. On August 31, a customer balance for $300 from a prior year was determined to be uncollectible and was written off.b. On December 15, the customer balance for $300 written off on August 31 was collected in full.arrow_forwardThe following transactions were completed by Irvine Company during the current fiscal year ended December 31: Required: 1. Record the January 1 credit balance of $25,685 in a T-account for Allowance for Doubtful Accounts. 2.A. Journalize the transactions. Refer to the Chart of Accounts for exact wording of account titles. B. Post each entry that affects the following selected T-accounts and determine the new balances: Allowance for Doubtful Accounts and Bad Debt Expense. 3. Determine the expected net realizable value of the accounts receivable as of December 31 (after all of the adjustments and the adjusting entry). 4. Assuming that instead of basing the provision for uncollectible accounts on an analysis of receivables, the adjusting entry on December 31 had been based on an estimated expense of ¼ of 1% of the net sales of $17,710,000 for the year, determine the following: A. Bad debt expense for the year. B. Balance in the allowance account after the adjustment of…arrow_forward

- The Signage Company specializes in the maintenance and repair of signs, such as billboards. On March 31, 2019, the accountant for The Signage Company prepared the trial balances shown at the top of the following page.arrow_forwardGood Note Company specializes in the repair of music equipment and is owned and operated by Robin Stahl. On November 30, 2018, the end of the current year, the accountant for GoodNote prepared the following trial balances: InstructionsJournalize the seven entries that adjusted the accounts at November 30. None of the accountswere affected by more than one adjusting entryarrow_forwardAt the end of the first year of operations, Gaur Manufacturing had gross accounts receivable of $300,000. Gaur's management estimates that 6% of the accounts will prove uncollectible.What journal entry should Gaur record to establish an allowance for uncollectible accounts? (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.)arrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning