Concept explainers

Videos

Preparing

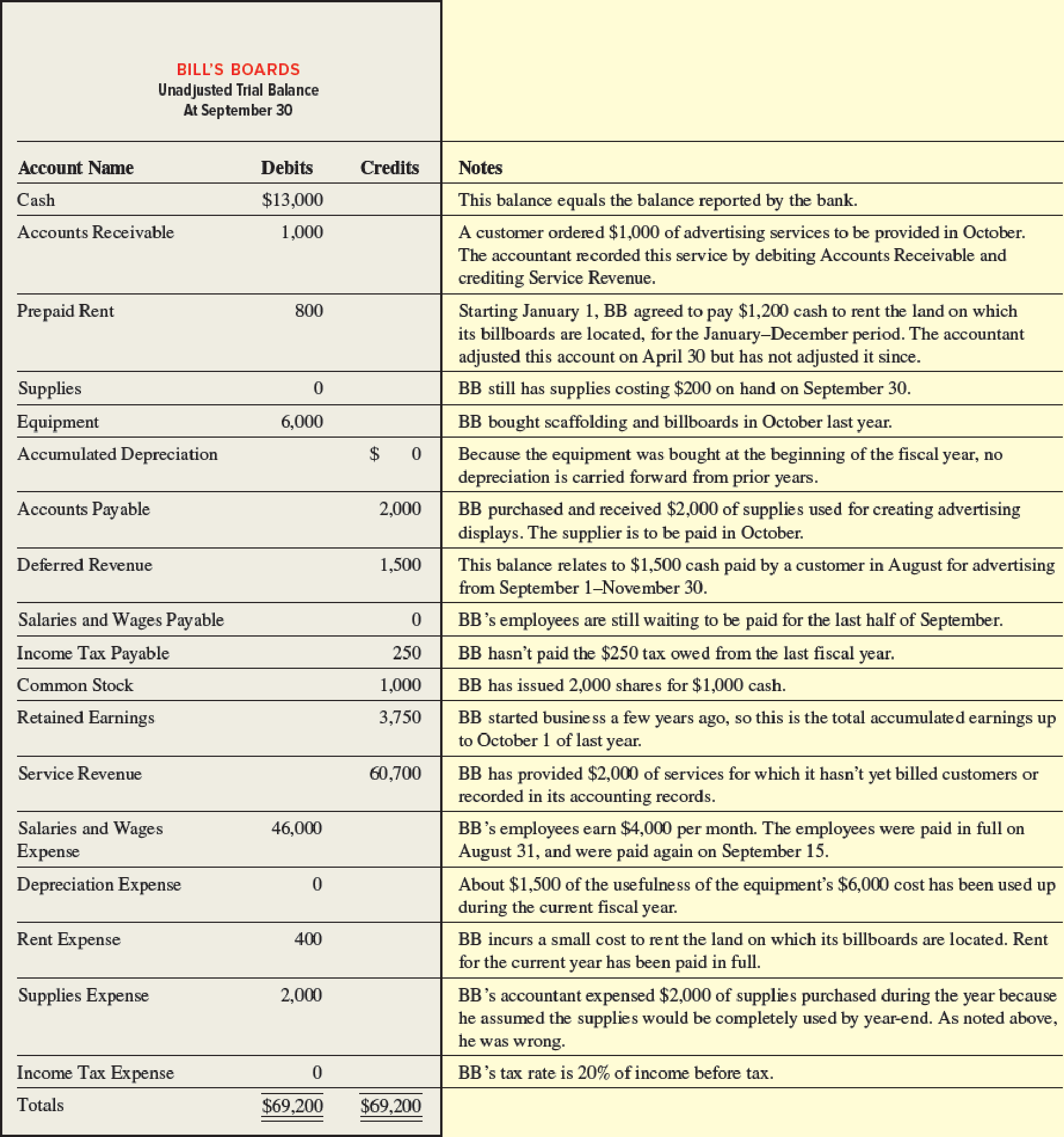

Bill’s Boards (BB) is an outdoor advertising company founded by William Longfall. William knows very little accounting so he hired a friend to “keep the books.” Unfortunately, William did not review his friend’s work and now it seems his friend has made a mess of the accounting records. William has provided you the following list of unadjusted account balances at BB’s September 30 fiscal year-end. You have reviewed the balances with William and made notes shown in the right column.

Required:

- 1. Use the notes to determine and record the adjusting

journal entries needed on September 30 to (a) fix the premature recording of advertising revenue, (b) update the rent accounts, (c) account for the use of equipment, (d) update deferred revenue, (e) accrue revenue not yet billed, (f ) accrue unpaid wages, (g) correct the supplies accounts, and (h) accrue income taxes for the year. - 2. Post the adjusting journal entries from requirement 1 to T-accounts to determine new adjusted balances, and prepare an adjusted trial balance. (If you are completing this exercise using the general ledger tool in Connect, this requirement will be completed automatically for you.)

- 3. Using the adjusted account balances from requirement 2, prepare an income statement, statement of

retained earnings , and classifiedbalance sheet .

a.

Record the adjusting journal entries needed on September 30.

Explanation of Solution

Adjusting entries: Adjusting entries are those entries which are recorded at the end of the year, to update the income statement accounts (revenue and expenses) and balance sheet accounts (assets, liabilities, and stockholders’ equity) to maintain the records according to accrual basis principle.

Record the adjusting journal entries needed on September 30 as follows:

| Date | Particulars | Debit ($) | Credit ($) | |

| (a) | Service Revenue (+R, +SE) | 1,000 | ||

| Accounts Receivable (+A) | 1,000 | |||

| (To record the service revenue recognized on account) | ||||

| (b) | Rent Expense (+E, –SE) (1) | 500 | ||

| Prepaid Rent (–A) | 500 | |||

| (To record the interest expense incurred at the end of the accounting year) | ||||

| (c) | Depreciation Expense (+E, –SE) | 1,500 | ||

| Accumulated Depreciation (+xA, –A) | 1,500 | |||

| (To record the depreciation expense incurred at the end of the accounting year) | ||||

| (d) | Deferred Revenue (–L) (2) | 500 | ||

| Service Revenue (+R, +SE) | 500 | |||

| (To record the service revenue recognized at the end of the accounting year) | ||||

| (e) | Accounts Receivable (+A) | 2,000 | ||

| Service Revenue (+R, +SE) | 2,000 | |||

| (To record the service revenue earned on account) | ||||

| (f) | Salaries and Wages Expense (+E, –SE) (3) | 2,000 | ||

| Salaries and Wages Payable (+L) | 2,000 | |||

| (To record the salaries and wages expense incurred at the end of the accounting year) | ||||

| (g) | Supplies (+A) | 200 | ||

| Supplies Expense (–E, +SE) | 200 | |||

| (To record supplies expense incurred at the end of the accounting year) | ||||

| (h) | Income Tax Expense (+E, –SE) ( 5) | 2,000 | ||

| Income Tax Payable (+L) | 2,000 | |||

| (To record the income tax expense incurred at the end of the accounting year) |

Table (1)

Working note 1:

Calculate the value of rent expense.

Working note 2:

Calculate the value of deferred revenue.

Working note 3:

Calculate the value of salaries and wages expense (adjusted).

Working note 4:

Calculate the unadjusted net income.

Working note 5:

Calculate the value of income tax expense:

Note: Supplies costing of $200 on hand on September 30 is considered as the supplies expense incurred at the end of the accounting year.

b.

Post the adjusting journal entries to T-accounts to determine the new adjusted balance and prepare the adjusted trial balance.

Explanation of Solution

Post the adjusting journal entries to T-accounts to determine the new adjusted balance as follows:

| Cash (A) | |||

| Beg. | 13,000 | ||

| 13,000 | |||

| Supplies (A) | |||

| Beg. | 0 | ||

| g. | 200 | ||

| 200 | |||

| Accounts Payable (L) | |||

| 2,000 | Beg. | ||

| 2,000 | |||

| Income Tax Payable (L) | |||

| 250 | Beg. | ||

| 2,000 | h. | ||

| 2,250 | |||

| Service Revenue (R) | |||

| a. | 1,000 | 60,700 | Beg. |

| 500 | d. | ||

| 2,000 | e. | ||

| 62,200 | |||

| Rent Expense (E) | |||

| Beg. | Beg. 400 | ||

| b. | 500 | ||

| 900 | |||

| Accounts Receivable (A) | |||

| Beg. | 1,000 | ||

| e. | 2,000 | 1,000 | a. |

| 2,000 | |||

| Equipment (A) | |||

| Beg | 6,000 | ||

| 6,000 | |||

| Deferred Revenue (L) | |||

| 1,500 | Beg. | ||

| d. | 500 | ||

| 1,000 | |||

| Common Stock (SE) | |||

| 1,000 | Beg. | ||

| 1,000 | |||

| Salaries and Wages Expense (E) | |||

| Beg. | 46,000 | ||

| f. | 2,000 | ||

| 48,000 | |||

| Supplies Expense (E) | |||

| Beg. | 2,000 | ||

| 200 | g. | ||

| 1,800 | |||

| Prepaid Rent (A) | |||

| Beg. | 800 | ||

| 500 | (b) | ||

| 300 | |||

| Accumulated Depreciation (xA) | |||

| 0 | Beg. | ||

| 1,500 | c. | ||

| 1,500 | |||

| Salaries and Wages Payable (L) | |||

| 0 | Beg. | ||

| 2,000 | f. | ||

| 2,000 | |||

| Retained Earnings (SE) | |||

| 3,750 | Beg. | ||

| 3,750 | |||

| Depreciation Expense (E) | |||

| Beg. | 0 | ||

| c. | 1,500 | ||

| 1,500 | |||

| Income Tax Expense | |||

| Beg. | 0 | ||

| h. | 2,000 | ||

| 2,000 | |||

Prepare the adjusted trial balance as follows:

| Company B | ||

| Adjusted Trial Balance | ||

| September, 30 | ||

| Account Titles | Debit ($) | Credit ($) |

| Cash | 13,000 | |

| Accounts Receivable | 2,000 | |

| Prepaid Rent | 300 | |

| Supplies | 200 | |

| Equipment | 6,000 | |

| Accumulated Depreciation | 1,500 | |

| Accounts Payable | 2,000 | |

| Deferred Revenue | 1,000 | |

| Salaries and Wages Payable | 2,000 | |

| Income Tax Payable | 2,250 | |

| Common Stock | 1,000 | |

| Retained Earnings | 3,750 | |

| Service Revenue | 62,200 | |

| Salaries and Wages Expense | 48,000 | |

| Supplies Expense | 1,800 | |

| Depreciation Expense | 1,500 | |

| Rent Expense | 900 | |

| Income Tax Expense | 2,000 | |

| Totals | 75,700 | 75,700 |

Table (2)

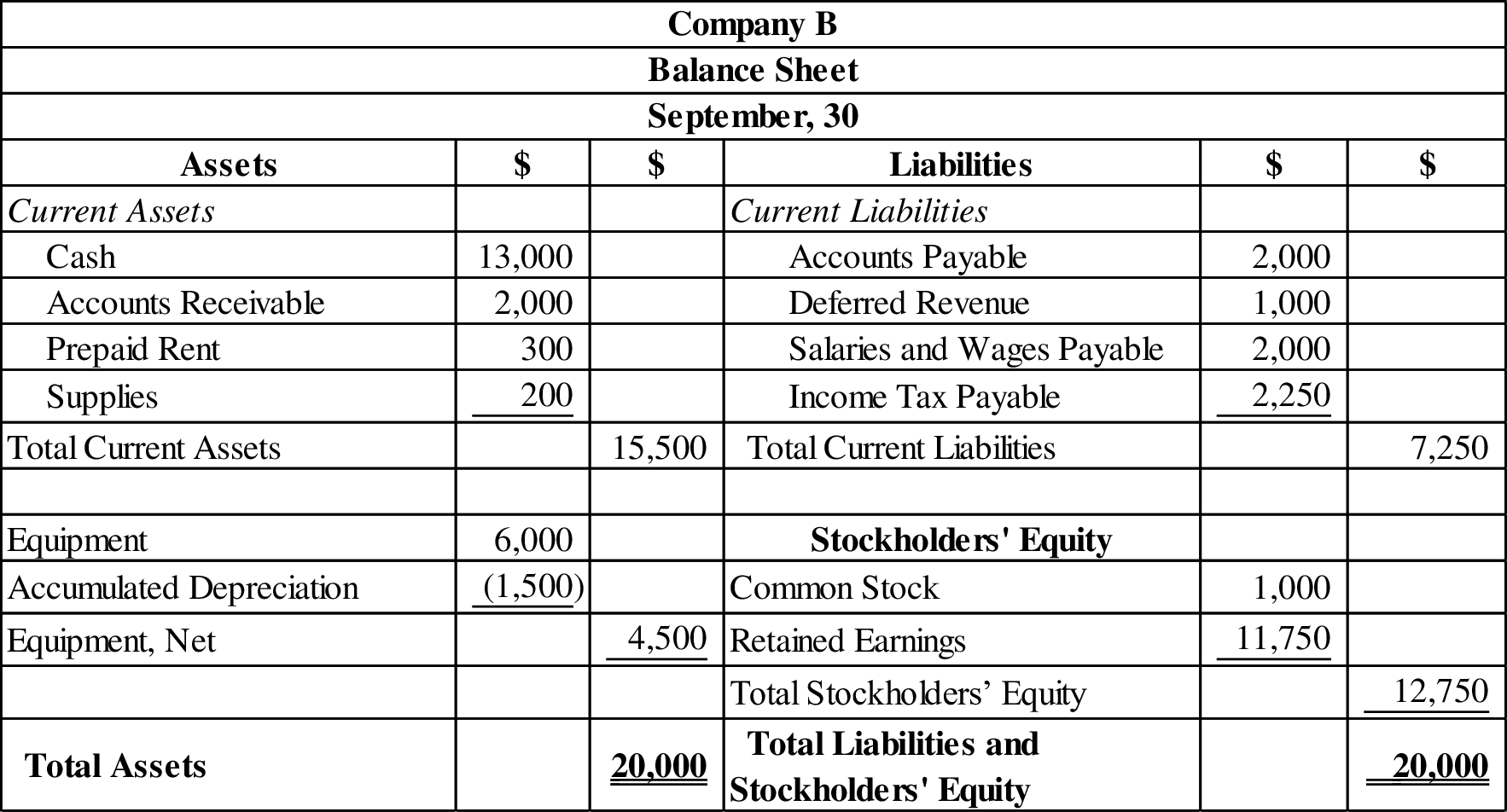

c.

Prepare an income statement, statement of retained earnings, and classified balance sheet of company B.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Classified balance sheet: The main elements of balance sheet assets, liabilities, and stockholders’ equity are categorized or classified further into sections, and sub-sections in a classified balance sheet. Assets are further classified as current assets, long-term investments, property, plant, and equipment (PPE), and intangible assets. Liabilities are classified into two sections current and long-term. Stockholders’ equity comprises of common stock and retained earnings. Thus, the classified balance sheet includes all the elements under different sections.

Prepare an income statement, statement of retained earnings, and classified balance sheet as follows:

| Company B | ||

| Income Statement | ||

| For the Year Ended September 30 | ||

| Particulars | $ | $ |

| Service Revenue | 62,200 | |

| Less: Expenses | ||

| Salaries and Wages Expense | 48,000 | |

| Supplies Expense | 1,800 | |

| Depreciation Expense | 1,500 | |

| Rent Expense | 900 | |

| Income Tax Expense | 2,000 | |

| Total Expenses | 54,200 | |

| Net Income | 8,000 | |

Table (3)

| Company B | |

| Statement of Retained Earnings | |

| For the Year Ended September 30 | |

| Particulars | $ |

| Beginning Balance | 3,750 |

| Add: Net Income | 8,000 |

| Less: Dividends | - |

| Ending Balance | 11,750 |

Table (4)

Figure (1)

Want to see more full solutions like this?

Chapter 4 Solutions

Fundamentals Of Financial Accounting

- Current Attempt in Progress Before preparing financial statements for the current year, the chief accountant for Sunland Company discovered the following errors in the accounts. 1. 2. 3. 1. Prepare the correcting entries at December 31. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts.) Account Titles and Explanation N The declaration and payment of $48,500 cash dividend was recorded as a debit to Interest Expense $48,500 and a credit to Cash $48,500. No. Date Dec. 31 2. A 10% stock dividend (1,400 shares) was declared on the $12 par value stock when the market price per share was $18. The only entry made was Stock Dividends (Dr.) $16,800 and Dividend Payable (Cr.) $16,800. The shares have not been issued. 3. A 4-for-1 stock split involving the issue of 357,000 shares of $5 par value common stock for 89,250 shares of $20 par value common stock…arrow_forwardThe chief accountant for Bramble Corporation provides you with the following list of accounts receivable written off in the current year. Date March 31 June 30 September 30 December 31 Customer E. L. Masters Company Stephen Crane Associates Amy Lowell's Dress Shop R. Frost, Inc. Amount $7,500 6,600 6.900 Net income would be $ 9,100 Bramble follows the policy of debiting Bad Debt Expense as accounts are written off. The chief accountant maintains that this procedure is appropriate for financial statement purposes because the Internal Revenue Service will not accept other methods for recognizing bad debts. All of Bramble's sales are on a 30-day credit basis. Sales for the current year total $2,200,000. The balance in Accounts Receivable at year-end is $81,100 and an analysis of customer risk and charge-off experience indicates that 12% of receivables will be uncollectible (assume a zero balance in the allowance). (b) By what amount would income before taxes differ if bad debt expense was…arrow_forwardGate City Cycles had trouble collecting its account receivable from Sue Ann Noel. On June 19, 2018, Gate City Cycles finally wrote off Noel's $750 account receivable. On December 31, Noel sent a $750 check to Gate City Cycles. Journalize the entries required for Gate City Cycles, assuming Gate City Cycles uses the direct write-off method. On June 19, 2018, Gate City Cycles wrote off Noel's $750 account receivable. Journalize the entry.(Record debits first, then credits. Select the explanation on the last line of the journal entry table.) Date Accounts and Explanation Debit Credit Jun. 19 On December 31, Noel sent a $750 check to Gate City Cycles. Start by journalizing the entry to reverse the earlier write-off. Date Accounts and Explanation Debit Credit Dec. 31arrow_forward

- Prior to recording the following, Elite Electronics, Incorporated, had a credit balance of $2,200 in its Allowance for Doubtful Accounts. Required: Prepare journal entries for each transaction. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field.) On August 31, a customer balance for $320 from a prior year was determined to be uncollectible and was written off. On December 15, the customer balance for $320 written off on August 31 was collected in full.arrow_forwardPyramid Corporation is assessed a $40 fee as the result of a $126 NSF check received from a customer for services purchased on account. Neither the fee nor the NSF check has been accounted for on Pyramid’s books.Required:Record the appropriate journal entry to update Pyramid’s books.arrow_forwardCreative Solutions Company, a computer consulting firm, has decided to write off the $15,220 balance of an account owed by a customer, Wil Treadwell. Question Content Area a. Journalize the entry to record the write-off, assuming that the direct write-off method is used. If an amount box does not require an entry, leave it blank. blank Account Debit Credit blank Bad Debt Expense Bad Debt Expense Accounts Receivable-Wil Treadwell Accounts Receivable-Wil Treadwell Feedback Area Feedback Remember that under the direct write-off method, Bad Debt Expense is not recorded until the customer's account is determined to be worthless. Question Content Area b. Journalize the entry to record the write-off, assuming that the allowance method is used. If an amount box does not require an entry, leave it blank. blank Account Debit Credit blank Allowance for Doubtful Accounts Allowance for Doubtful Accountsarrow_forward

- James Din has been advised that one of his customers has ceased trading and that he will not recover the balance of $720 owed by his customer.Required:Record the journal entry that should be made in the general ledger.arrow_forwardQuantum Solutions Company, a computer consulting firm, has decided to write off the $33,550 balance of an account owed by a customer, Alliance Inc. Required: On March 1, journalize the entry to record the write-off, assuming that (a) the direct write-off method is used and (b) the allowance method is used. Refer to the Chart of Accounts for exact wording of account titles. CHART OF ACCOUNTS Quantum Solutions Company General Ledger ASSETS 110 Cash 111 Petty Cash 121 Accounts Receivable-Alliance Inc. 129 Allowance for Doubtful Accounts 131 Interest Receivable 132 Notes Receivable 141 Merchandise Inventory 145 Office Supplies 146 Store Supplies 151 Prepaid Insurance 181 Land 191 Store Equipment 192 Accumulated Depreciation-Store Equipment 193 Office Equipment 194 Accumulated Depreciation-Office Equipment LIABILITIES 210 Accounts Payable 211 Salaries Payable 213 Sales Tax Payable 214 Interest Payable 215…arrow_forwardWaffle Shack is a registered vendor, with a number of transactions in July that it has not yet encountered. It needs assistance in recording these transactions in its financial records. In order to assist the business, prepare the general journal entries (with narrations) for the following three transactions (voucher and folio numbers are not required): Transaction 1 As a result of one of the finance staff members being on leave and no one fulfilling the role, the business did not settle one of their outstanding supplier accounts within the settlement period. As a result, the supplier charged them interest for one month on their outstanding balance of R146 000 on 31 July, with the supplier's annual interest charge being 20%. Date Details Debit Credit Transaction 2 The owner of the business took a waffle iron from the business for use in her home on 15 July. The business initially purchased the waffle iron for R7 500. Its market value is now R5 250. Date Details Debit Credit Transaction…arrow_forward

- The chief accountant for Dickinson Corporation provides you with the following list of accounts receivable written off in the current year. Date Customer Amount March 31 E. L. Masters Company $7,800 June 30 Stephen Crane Associates 6,700 September 30 Amy Lowell"s Dress Shop 7,000 December 31 R. Frost, Inc. 9,830 Dickinson follows the policy of debiting Bad Debt Expense as accounts are written off. The chief accountant maintains that this procedure is appropriate for financial statement purposes because the Internal Revenue Service will not accept other methods for recognizing bad debts. All of Dickinson’s sales are on a 30-day credit basis. Sales for the current year total $2,200,000. The balance in Accounts Receivable at year-end is $77,000 and an analysis of customer risk and charge-off experience indicates that 12% of receivables will be uncollectible (assume a zero balance in the allowance). Instructions a. Do you agree or disagree with…arrow_forwardDexter Company applies the direct write-off method in accounting for uncollectible accounts. March 11 Dexter determines that it cannot collect $45,000 of its accounts receivable from its customer Leer Company 29 Leer Company unexpectedly pays its account in full to Dexter Company. Dexter records its recovery of this bad d Prepare journal entries to record the above selected transactions of Dexter. View transaction list Journal entry worksheet 1 2 Record write off of Leer Company account Note: Enter debits before credits. Date General Journal Debit Credit March 11 Record entry Clear entry View general journal 2arrow_forwardb. Discuss whether there has or has not been any violation of ethical conduct.arrow_forward