Videos

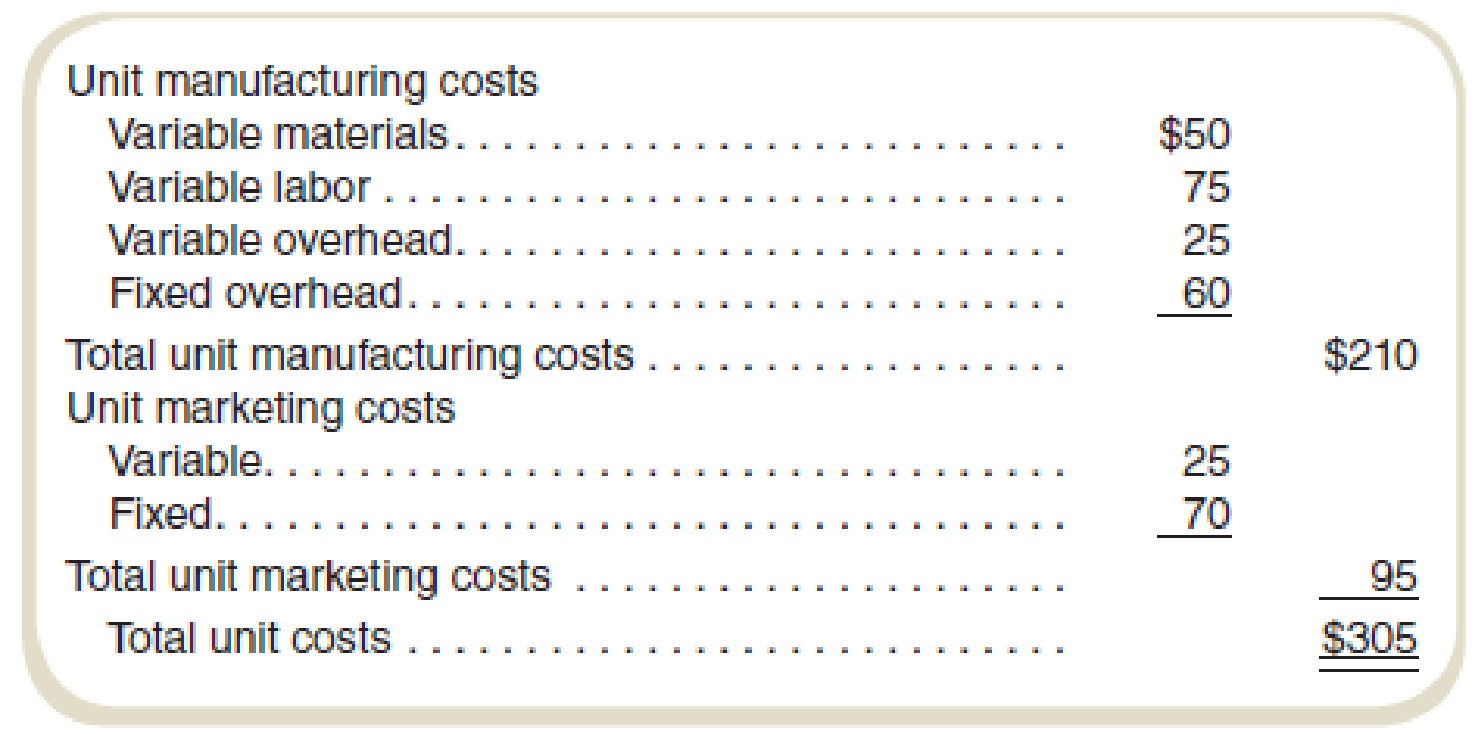

Davis Kitchen Supply produces stoves for commercial kitchens. The costs to manufacture and market the stoves at the company’s normal volume of 6,000 units per month are shown in the following table:

Unless otherwise stated, assume that no connection exists between the situation described in each question; each is independent. Unless otherwise stated, assume a regular selling price of $370 per unit. Ignore income taxes and other costs that are not mentioned in the table or in the question itself.

Required

- a.

Market research estimates that volume could be increased to 7,000 units, which is well within production capacity limitations if the price were cut from $370 to $325 per unit. Assuming that the cost behavior patterns implied by the data in the table are correct, would you recommend taking this action? What would be the impact on monthly sales, costs, and income? - b. On March 1, the federal government offers Davis a contract to supply 1,000 units to military bases for a March 31 delivery. Because of an unusually large number of rush orders from its regular customers, Davis plans to produce 8,000 units during March, which will use all available capacity. If it accepts the government order, it would lose 1,000 units normally sold to regular customers to a competitor. The government contract would reimburse its “share of March

manufacturing costs ” plus pay a $50,000 fixed fee (profit). (No variable marketing costs would be incurred on the government’s units.) What impact would accepting the government contract have on March income? (Part of your problem is to figure out the meaning of “share of March manufacturing costs.”) - c. Davis has an opportunity to enter a highly competitive foreign market. An attraction of the foreign market is that its demand is greatest when the domestic market’s demand is quite low; thus, idle production facilities could be used without affecting domestic business. An order for 2,000 units is being sought at a below-normal price to enter this market. For this order, shipping costs will total $40 per unit; total (marketing) costs to obtain the contract will be $4,000. No other variable marketing costs would be required on this order, and it would not affect domestic business. What is the minimum unit price that Davis should consider for this order of 2,000 units?

- d. An inventory of 460 units of an obsolete model of the stove remains in the stockroom. These must be sold through regular channels (thus incurring variable marketing costs) at reduced prices or the inventory will soon be valueless. What is the minimum acceptable selling price for these units?

- e. A proposal is received from an outside contractor who will make and ship 2,000 stoves per month directly to Davis’s customers as orders are received from Davis’s sales force. Davis’s fixed marketing costs would be unaffected, but its variable marketing costs would be cut by 20 percent for these 2,000 units produced by the contractor. Davis’s plant would operate at two-thirds of its normal level, and total fixed manufacturing costs would be cut by 30 percent. What in-house unit cost should be used to compare with the quotation received from the supplier? Should the proposal be accepted for a price (that is, payment to the outside contractor) of $215 per unit?

- f. Assume the same facts as in requirement (e) except that the idle facilities would be used to produce 1,600 modified stoves per month for use in extreme climates. These modified stoves could be sold for $450 each, while the costs of production would be $275 per unit variable manufacturing expense. Variable marketing costs would be $50 per unit. Fixed marketing and manufacturing costs would be unchanged whether the original 6,000 regular stoves were manufactured or the mix of 4,000 regular stoves plus 1,600 modified stoves were produced. Should the proposal be accepted for a price of $215 per unit to the outside contractor?

a.

Explain whether the action should be taken or not on the basis of the given situation. Also, identify the impact on monthly sales, costs, and income.

Explanation of Solution

Differential cost:

The cost difference of two alternatives is differential cost. Before taking any decision, the management of the business has to check for various options to make sure the reliability of the alternative.

| Particulars | Before Price Reduction | After price reduction | Impact | Increase/decrease |

| Sales price | $370 | $325 | ||

| Quantity | 6000 | 7000 | ||

| Revenue | $2,220,000 | $2,275,000 | $55,000 | Increase |

| Variable manufacturing cost | $900,000 | $1,050,000 | $150,000 | Increase |

| Variable marketing costs | $150,000 | $175,000 | $25,000 | Increase |

| Contribution margin | $1,170,000 | $1,050,000 | ($120,000) | Decrease |

| Fixed manufacturing costs | $360,000 | $360,000 | ||

| Fixed marketing costs | $420,000 | $420,000 | ||

| Income | $390,000 | $270,000 | ($120,000) | Decrease |

Table: (1)

Thus, the price should not be lowered because it results in a decrease in operating profit. However, the market share and other points can be taken into consideration.

b.

Identify the impact of the increase in price on profit.

Explanation of Solution

The impact of the increase in price on profit:

| Particulars | Without Government Contract | With Government Contract | Impact | Increase/decrease | ||

| Regular | Government | Total | ||||

| Revenue | $2,960,000 | $2,590,000 | $245,000 (1) | $2,835,000 | ($125,000) | Decrease |

| Variable manufacturing costs | $1,200,000 | $1,050,000 | $150,000 | $1,200,000 | $0 | |

| Variable marketing costs | $200,000 | $175,000 | $0 | $175,000 | ($25,000) | Decrease |

| Contribution margin | $1,560,000 | $1,365,000 | $95,000 | $1,460,000 | ($100,000) | Decrease |

| Fixed manufacturing costs | $360,000 | $360,000 | $0 | |||

| Fixed marketing costs | $420,000 | $420,000 | $0 | |||

| Income | $780,000 | $680,000 | ($100,000) | Decrease | ||

Table: (2)

Thus, the contact should not be accepted because it results in decrease in income to the company.

Working note 1:

Compute the government revenue:

c.

Find the minimum unit price that Mr. D should consider for this order of 2,000 units.

Explanation of Solution

Compute the minimum unit price that Mr. D should consider for this order of 2,000 units:

Thus, the minimum unit price that Mr. D should consider for this order of 2,000 units is $192.

d.

Determine the minimum acceptable selling price for the given units.

Explanation of Solution

Determine the minimum acceptable selling price for the given units:

The minimum acceptable selling price will be the differential costs which involve the marketing costs of $25 per unit. The minimum price is the differential marketing costs because the variable costs must be recovered for selling the product. The additional price if charged will add to the income.

e.

Calculate the in-house unit cost which should be used to compare with the quotation received from the supplier. Also, decide whether the proposal should be accepted for a price of $215 per unit.

Explanation of Solution

Calculate the in-house unit cost which should be used to compare with the quotation received from the supplier:

| Particulars | All Production In-house | 2,000 Units Contracted |

| Total revenue | $ 2,220,000 | $ 2,220,000 |

| Total variable manufacturing costs | $ 900,000 | $ 1,030,000 (2) |

| Total variable marketing costs | $ 150,000 | $ 140,000 (3) |

| Total contribution margin | $ 1,170,000 | $ 1,050,000 |

| Total fixed manufacturing costs | $ 360,000 | $ 252,000 (4) |

| Total fixed marketing costs | $ 420,000 | $ 420,000 |

| Income | $ 390,000 | $ 378,000 |

Table: (3)

The proposed price of $215 should not be accepted by the management because it would result in a decrease in net income by $12,000. Thus, price of $215 is not an acceptable price.

Working note 2:

Compute the total variable manufacturing costs when 2,000 units are being contracted:

Working note 3:

Compute the total variable marketing costs when 2,000 units are being contracted:

Working note 4:

Compute the total fixed marketing costs when 2,000 units are being contracted:

f.

Determine whether the proposal should be accepted for a price of $215 per unit to the outside contractor.

Explanation of Solution

Determine the income for a price of $215 per unit to the outside contractor:

| Particulars | 6,000 Regular Stoves Produced | Contract 2,000 Regular stoves; Produce 1,600 Modified stoves and 4,000 Regular Stoves | |||

| In-house | Regular (In) | Regular (Out) | Modified | Total | |

| Revenue | $2,220,000 | $1,480,000 | $740,000 | $720,000 | $2,940,000 (5) |

| Variable manufacturing costs | $900,000 | $600,000 | $430,000 | $440,000 | $1,470,000 (6) |

| Variable marketing costs | $150,000 | $100,000 | $40,000 | $80,000 | $220,000 (7) |

| Contribution margin | $1,170,000 | $780,000 | $270,000 | $200,000 | $1,250,000 |

| Fixed manufacturing costs | $360,000 | $360,000 | |||

| Fixed marketing costs | $420,000 | $420,000 | |||

| Income | $390,000 | $470,000 | |||

Table: (4)

Compute the in-house cost savings from the contract:

| Particulars | Amount (per unit) |

| Variable manufacturing cost saved | $ 150 |

| Variable marketing saved | $ 5 |

| Contribution from freed-up capacity | $ 100 |

| In-house cost savings | $ 255 |

Table: (5)

The proposed price of $215 should be accepted now. The deal made with the subcontractor is more profitable as there is a cost saving of $255 per unit.

Working note 5:

Compute the total revenue when 2,000 units are being contracted:

Working note 6:

Compute the total variable manufacturing costs when 2,000 units are being contracted:

Working note 7:

Compute the total variable marketing costs when 2,000 units are being contracted:

Want to see more full solutions like this?

Chapter 4 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- A company manufactures various-sized plastic bottles for its medicinal product. The manufacturing cost for small bottles is $148 per unit (100 bottles), including fixed costs of $33 per unit. A proposal is offered to purchase small bottles from an outside source for $95 per unit, plus $11 per unit for freight. a. Prepare a differential analysis dated July 31 to determine whether the company should make (Alternative 1) or buy (Alternative 2) the bottles, assuming fixed costs are unaffected by the decision. If an amount is zero, enter "0". Use a minus sign to indicate a loss. Differential Analysis Make Bottles (Alt. 1) or Buy Bottles (Alt. 2) July 31 Make Bottles (Alternative 1) Buy Bottles (Alternative 2) Differential Effect on Income (Alternative 2) Sales price $fill in the blank 2d4f3efa1ffef7f_1 $fill in the blank 2d4f3efa1ffef7f_2 $fill in the blank 2d4f3efa1ffef7f_3 Unit costs: Purchase price $fill in the blank 2d4f3efa1ffef7f_4 $fill in the blank…arrow_forwardUse this information for Stryker Industries to answer the question that follow.Stryker Industries received an offer from an exporter for 15,000 units of product at $17.50 per unit. The acceptance of the offer will not affect normal production or domestic sales prices. The following data are available: Domestic unit sales price $20 Unit manufacturing costs: Variable 11 Fixed 1 What is the amount of income or loss from the acceptance of the offer?arrow_forwardA company manufactures a subcomponent of an assembly for $80 per unit, including fixed costs of $25 per unit. A proposal is offered to purchase the subcomponent from an outside source for $60 per unit, plus $5 per unit freight. Prepare a differential analysis to determine whether the company should make (Alternative 1) or buy (Alternative 2) the subcomponent, assuming fixed costs are unaffected by the decision.arrow_forward

- How can I resolve this problem Mauro Products distributes a single product, a woven basket whose selling price is $12 per unit and whose variable expense is $9 per unit. The company’s monthly fixed expense is $7,800. Required: 1. Calculate the company’s break-even point in unit sales. 2. Calculate the company’s break-even point in dollar sales. (Do not round intermediate calculations.) 3. If the company's fixed expenses increase by $600, what would become the new break-even point in unit sales? In dollar sales?arrow_forwardGreen Co. incurs a cost of $15 per pound to produce Product X, which it sells for $26 per pound. The company can further process Product X to produce Product Y. Product Y would sell for $30 per pound and would require an additional cost of $10 per pound to be produced. The differential revenue of producing Product Y is _____. a.$4 per pound b.$5 per pound c.$26 per pound d.$30 per poundarrow_forwardYour answer is partially correct. Novak Co. sells product P-14 at a price of $48 a unit. The per-unit cost data are direct materials $15, direct labour $12, and overhead $16 (75% variable). Novak has no excess capacity to accept a special order for 38,200 units, at a discount of 25% from the regular price. Selling costs associated with this order would be $3 per unit. Indicate the net income (loss) that Novak would realize by accepting the special order. (Enter loss with a negative sign preceding the number, e.g.-15,000 or parenthesis, e.g. (15,000).) Incremental income (loss) Novak Co. should not accept eTextbook and Media Save for Later $ -382000 the special order. Attempts: 2 of 3 used Submit Answerarrow_forward

- [The following information applies to the questions displayed below.] Henna Company produces and sells two products, Carvings and Mementos. It manufactures these products in separate factories and markets them through different channels. They have no shared costs. This year, the company sold 42,000 units of each product. Income statements for each product follow. Sales Variable costs Contribution margin Fixed costs Income Problem 18-4A (Algo) Part 1 Required: 1. Compute the break-even point in dollar sales for each product. (Enter CM ratlo as percentage rounded to 2 decimal places.) Contribution Margin Ratio Numerator: Break-Even Point in Dollars Numerator: Contribution Margin Ratio Break-Even Point in Dollars 1 1 1 1 Carvings $ 747,600 523,320 224,280 Mementos $ 747,600 149,520 598,080 108,280 482,080 $ 116,000 $ 116,000 1 PRODUCT CARVINGS Denominator: Denominator: PRODUCT MEMENTOS = IL 11 Contribution margin ratio Break-even point in dollars Contribution margin ratio Break-even point…arrow_forwardRequired information [The following information applies to the questions displayed below.] Trevino Company makes and sells products with variable costs of $24 each. Trevino incurs annual fixed costs of The current sales price is $87. Note: The requirements of this question are interdependent. For example, the $252,000 desired profit introduce Requirement c also applies to subsequent requirements. Likewise, the $80 sales price introduced in Requiremen applies to the subsequent requirements. f. If variable cost rises to $30 per unit and fixed costs are $280,000, what level of sales is required to earn the desired your answer in units and dollars. Prepare an income statement using the contribution margin format. Complete this question by entering your answers in the tabs below. Req F1 If variable cost rises to $30 per unit and fixed costs are $280,000, prepare an income statement using the contribution margin format. Req F2 TREVINO COMPANY Income Statement Sales Variable cost Contribution…arrow_forwardUse the information below to answer the following question(s). Franscioso Company sells several products. Information of average revenue and costs is as follows: Selling price per unit $28.50 Variable costs per unit: Direct material $5.25 Direct manufacturing labour $1.15 Manufacturing overhead $0.25 Selling costs $1.85 Annual fixed costs $110,000 The Franscioso Company contribution margin ratio is O A. 0.702:1. O B. 1.425:1. O C. 0.298:1. O D. 1.102:1. O E. 0.637:1.arrow_forward

- Z Motor Inc. manufactures and sell a range of automobile parts. The regular price and costs data for Part C are as follows: Price and Cost Data for Part C Price and Costs Amount Market selling price $79 Variable costs per unit $35 Fixed costs per unit (allocated) $25 Z Motor received an offer from an exporter to sell 5,000 units of Part C for $49 per unit. The company has enough capacity to fulfill this offer. Acceptance of this offer will not affect the company’s regular sale. The amount of profit or loss from the acceptance of the offer would be: Group of answer choices $70,000 profit $245,000 profit $150,000 loss $55,000 lossarrow_forwardSheridan Company incurs a cost of $36 per unit, of which $20 is variable, to make a product that normally sells for $57. A foreign wholesaler offers to buy 7,000 units at $30 each. Sheridan will incur additional costs of $2 per unit to imprint a logo and to pay for shipping. Compute the increase or decrease in net income Sheridan will realize by accepting the special order, assuming Sheridan has sufficient excess operating capacity. (Enter negative amounts using either a negative sign preceding the number e.g.-45 or parentheses e.g. (45)) Revenues Costs Net income $ $ Reject Sheridan company should LA $ LA Should Sheridan Company accept the special order? ✓the special order. Accept $ LA LA $ Net Income Increase (Decrease) A SUPParrow_forwardPharoah Company has decided to introduce a new product. The new product can be manufactured by either a capital-intensive method or a labor-intensive method. The manufacturing method will not affect the quality of the product. The estimated manufacturing costs by the two methods are as follows. Direct materials Direct labor Variable overhead Fixed manufacturing costs (a) Pharoah' market research department has recommended an introductory unit sales price of $28.00. The selling expenses are estimated to be $432,000 annually plus $2.00 for each unit sold, regardless of manufacturing method. Capital-Intensive $4.00 per unit $5.00 per unit $3.00 per unit $2,284,000 Calculate the estimated break-even point in annual unit sales of the new product if Pharoah Company uses the: 1. Capital-intensive manufacturing method. Labor-intensive manufacturing method. 2. Labor-Intensive $4.50 per unit $7.00 per unit $4.00 per unit $1,437,000 Break-even point in units Capital-Intensive Labor-Intensivearrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education