Concept explainers

Videos

1.

General Ledger

General ledger refers to the ledger that records all the transactions of the business related to the company’s assets, liabilities, owners’ equities, revenues, and expenses. Each subsidiary ledger is represented in the general ledger by summarizing the account.

Accounts payable control account and subsidiary ledger

Accounts payable account and subsidiary ledger is the ledger which is used to post the creditors transaction in one particular ledger account. It helps the business to locate the error in the creditor ledger balance. After all transactions of creditor accounts are posted, the balances in the accounts payable subsidiary ledger should be totaled, and compare with the balance in the general ledger of accounts payable. If both the balance does not agree, the error has been located and corrected.

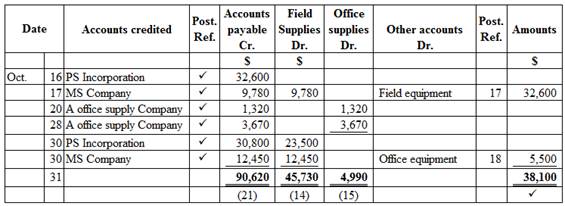

Purchase journal

Purchase journal refers to the journal that is used to record all purchases on account. In the purchase journal, all purchase transactions are recorded only when the business purchased the goods on account. For example, the business purchased cleaning supplies on account.

Cash payments journal

Cash payments journal refers to the journal that is used to record all transaction which involves the cash payments. For example, the business paid cash to employees (salary paid to employees).

To Prepare: A single column revenue journal and cash receipt journal, and post the accounts in the accounts payable subsidiary ledger.

1.

Explanation of Solution

Purchase journal

Purchase journal of Company WTE in the month of October 2016 is as follows:

Figure (1)

Cash payment journal

Cash payment journal of Company WTE in the month of October 2016 is as follows:

Cash payment journal

| Date | Check No. | Account debited | Post Ref. | Other accounts Dr. | Accounts payable Dr. | Cash Dr. | |

| Oct. | 16 | 1 | Rent expense | 71 | 7,000 | 7,000 | |

| 18 | 2 | Field supplies | 14 | 4,570 | 4,570 | ||

| Office supplies | 15 | 650 | 650 | ||||

| 24 |

|

✓ | 32,600 | 32,600 | |||

| 26 |

|

✓ | 9,780 | 9,780 | |||

| 28 | Land | 240,000 | 240,000 | ||||

| 30 |

|

✓ | 1,320 | 1,320 | |||

| 31 | Salary expense | 61 | 32,000 | 32,000 | |||

| 31 | 284,220 | 43,700 | 327,920 | ||||

| ✓ | (21) | (11) | |||||

Table (1)

Accounts payable subsidiary ledger

| Name: A Office supply Company | ||||||

| Date | Item | Post. Ref | Debit ($) |

Credit ($) | Balance ($) | |

| Oct. | 20 | P1 | 1,320 | 1,320 | ||

| 28 | P1 | 3,670 | 4,990 | |||

| 30 | CP1 | 1,320 | 3,670 | |||

Table (2)

| Name: MS Company | ||||||

| Date | Item | Post. Ref | Debit ($) |

Credit ($) | Balance ($) | |

| Oct. | 17 | P1 | 9,780 | 9,780 | ||

| 26 | CP1 | 9,780 | - | |||

| 30 | P1 | 12,450 | 12,450 | |||

Table (3)

| Name: PS Incorporation | ||||||

| Date | Item | Post. Ref | Debit ($) |

Credit ($) | Balance ($) | |

| Oct. | 16 | P1 | 32,600 | 32,600 | ||

| 24 | CP1 | 32,600 | - | |||

| 30 | P1 | 30,800 | 30,800 | |||

Table (4)

2. and 3.

To

2. and 3.

Explanation of Solution

Prepare the general ledger for given accounts as follows:

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 31 | CP1 | 327,920 | 327,920 | |||

Table (5)

| Account: Field supplies Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 18 | CP1 | 4,570 | 4,570 | |||

| 31 | P1 | 47,530 | 52,100 | ||||

Table (6)

| Account: Office supplies Account no. 15 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 18 | CP1 | 650 | 650 | |||

| 31 | P1 | 4,990 | 5,460 | ||||

Table (7)

| Account: Prepaid rent Account no. 16 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 31 | J1 | 15,000 | 15,000 | |||

Table (8)

| Account: Field equipment Account no. 17 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 16 | P1 | 32,600 | 32,600 | |||

| 31 | J1 | 15,000 | 17,600 | ||||

Table (9)

| Account: Office equipment Account no. 18 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 31 | P1 | 5,500 | 5,500 | ||||

Table (10)

| Account: Land Account no. 19 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 23 | CP1 | 240,000 | 240,000 | |||

Table (11)

| Account: Accounts payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 31 | P1 | 90,620 | 90,620 | |||

| 31 | CP1 | 43,700 | 46,920 | ||||

Table (12)

| Account: Salary expense Account no. 61 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 31 | CP1 | 32,000 | 32,000 | |||

Table (13)

| Account: Rent expense Account no. 71 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 16 | CP1 | 7,000 | 7,000 | |||

Table (14)

| Journal Page 01 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| Oct. | 31 | Prepaid rent | 16 | 15,000 | |

| Field equipment | 17 | 15,000 | |||

| (To record leasing of field equipment) | |||||

Table (15)

4.

To prepare: The accounts payable creditor balances.

4.

Explanation of Solution

Accounts payable creditor balance

Accounts payable creditor balance is as follows:

| Company WTE | |

| Accounts payable creditor balances | |

| October 31, 2016 | |

| Amount ($) | |

| A Office supply Company | 3,670 |

| MS Company | 12,450 |

| PS Incorporation | 30,800 |

| Total accounts receivable | 46,920 |

Table (16)

Accounts payable controlling account

Ending balance of accounts payable controlling account is as follows:

| Company WTE | |

| Accounts payable (Controlling account) | |

| October 31, 2016 | |

| Amount ($) | |

| Opening balance | 0 |

| Add: | |

| Total credits (from purchase journal) | 90,620 |

| 90,620 | |

| Less: | |

| Total debits (from cash payment journal) | (43,700) |

| Total accounts payable | 46,920 |

Table (17)

In this case, accounts payable subsidiary ledger is used to identify, and locate the error by way of cross-checking the creditor balance and accounts payable controlling account. From the above calculation, we can understand that both balances of accounts payable is agree, hence there is no error in the recording and posing of transactions.

5.

To discuss: The reason for using subsidiary ledger for the field equipment.

5.

Explanation of Solution

A subsidiary ledger for the field equipment helps the company to track the cost of each piece of equipment, location, useful life, and other necessary data. This information is used for safeguarding the equipment and determining depreciation of equipment.

Want to see more full solutions like this?

Chapter 5 Solutions

Accounting (Text Only)

- Notes Receivable Transactions The following notes receivable transactions occurred for Harris Company during the last three months of the current year. (Assume all notes are dated the day the transaction occurred.) Required: 1. Prepare the journal entries to record the preceding note transactions and the necessary adjusting entries on December 31. (Assume that Harris does not normally sell its notes and uses a 360-day year for the purpose of computing interest. Round all calculations to the nearest penny.) 2. Show how Harris notes receivable would be disclosed on the December 31 balance sheet. (Assume these are the only note transactions encountered by Harris during the year.)arrow_forwardThe transactions completed by Revere Courier Company during December 2016, the first month of the fiscal year, were as follows: Instructions 1. Enter the following account balances in the general ledger as of December 1: 2. Journalize the transactions for December 2016, using the following journals similar to those illustrated in this chapter: cash receipts journal (p. 31), purchases journal (p. 37, with columns for Accounts Payable, Maintenance Supplies, Office Supplies, and Other Accounts), single-column revenue journal (p. 35), cash payments journal (p. 34), and two-column general journal (p. 1). Assume that the daily postings to the individual accounts in the accounts payable subsidiary ledger and the accounts receivable subsidiary ledger have been made. 3. Post the appropriate individual entries to the general ledger. 4. Total each of the columns of the special journals, and post the appropriate totals to the general ledger; insert the account balances. 5. Prepare a trial balance.arrow_forwardTransactions related to revenue and cash receipts completed by Albany Architects Co. during the period November 230, 2016, are as follows: Instructions 1. Insert the following balances in the general ledger as of November 1: 2. Insert the following balances in the accounts receivable subsidiary ledger as of November 1: 3. Prepare a single-column revenue journal (p. 40) and a cash receipts journal (p. 36). Use the following column headings for the cash receipts journal: Fees Earned Cr., Accounts Receivable Cr., and Cash Dr. The Fees Earned column is used to record cash fees. Insert a check mark () in the Post. Ref. column when recording cash fees. 4. Using the two special journals and the two-column general journal (p. 1), journalize the transactions for November. Post to the accounts receivable subsidiary ledger, and insert the balances at the points indicated in the narrative of transactions. Determine the balance in the customers account before recording a cash receipt. 5. Total each of the columns of the special journals, and post the individual entries and totals to the general ledger. Insert account balances after the last posting. 6. Determine that the sum of the customer balances agrees with the accounts receivable controlling account in the general ledger. 7. Why would an automated system omit postings to a controlling account as performed in step 5 for Accounts Receivable?arrow_forward

- Question: Banksia Company completed the following transactions during 2018-2019. The annual accounting period ends 30 June 2019.a) Purchased inventory on credit at cost of AUD 16,800; perpetual inventory system is used.b) Received a customer deposit of AUD 18,000 from ABC Ltd for services to be rendered in the future.c) Borrowed AUD 900,000 from the bank on 1 March 2019 by giving the bank a six-month, 9% interest bearing note payable.d) Performed AUD 8,000 of the services paid for by ABC Ltd; the rest will be rendered in August 2019.e) Received the electricity bill for AUD 24,200, which will be paid in early July.f) On 1 June 2019 received rent in advance of AUD 21,600 from XYZ Ltd for a 3 month lease of premises from 1 June until 31 August 2019.g) Wages accrued in the last weekly payroll amounted to AUD 23,000 and will be paid on 5 July 2019.Required:1) Prepare the journal entries for each of these transactions. 2) Prepare all adjusting entries required on 30 June 2019.arrow_forwardView Policies Current Attempt in Progress Vaughn Bikes Ltd. reports cash sales of $6,600 on October 1. (a) Record the sales assuming they are subject to 13% HST. (b) Record the sales assuming they are subject to 5% GST and 9.975% QST. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. List all debit entries before credit entries. Round answers to 0 decimal places, e.g. 5,275.) No. Date Account Titles and Explanation Debit Credit (a) Oct. 1 (b) Oct. 1 eTextbook and Media List of Accountsarrow_forwardRequired information [The following information applies to the questions displayed below.] Tyrell Company entered into the following transactions involving short-term liabilities. Year 1 April 20 Purchased $39,500 of merchandise on credit from Locust, terms n/30. May 19 Replaced the April 20 account payable to Locust with a 90-day, 8%, $35,000 note payable along with paying $4,500 in cash. July 8 Borrowed $63,000 cash from NBR Bank by signing a 120-day, 12%, $63,000 note payable. Paid the amount due on the note to Locust at the _?- maturity date. ? November 28 December 31 Paid the amount due on the note to NBR Bank at the maturity date. Borrowed $24,000 cash from Fargo Bank by signing a 60-day, 7%, $24,000 note payable. Recorded an adjusting entry for accrued interest on the note to Fargo Bank. Year 2 _ ? Paid the amount due on the note to Fargo Bank at the maturity date. 5. Prepare journal entries for all the preceding transactions and events. Note: Do not round your intermediate…arrow_forward

- Revenue and Cash Receipts Journals Lasting Summer Inc. has $1,840 in the October 1 balance of the accounts receivable account consisting of $850 from Champion Co. and $990 from Wayfarer Co. Transactions related to revenue and cash receipts completed by Lasting Summer Inc. during the month of October 20Y5 are as follows: Oct. 3. Issued Invoice No. 622 for services provided to Palace Corp., $1,930. 5. Received cash from Champion Co., on account, for $850. 8. Issued Invoice No. 623 for services provided to Sunny Style Inc., $3,330. 12. Received cash from Wayfarer Co., on account, for $990. 18. Issued Invoice No. 624 for services provided to Amex Services Inc., $2,340. 23. Received cash from Palace Corp. for Invoice No. 622 of October 3. 28. Issued Invoice No. 625 to Wayfarer Co., on account, for $1,970. 30. Received cash from Rogers Co. for services provided, $70. a. Prepare a single-column revenue journal to record these transactions. Enter…arrow_forwardеВook Print Item Record journal entries for the following transactions of Telesco Enterprises. Jan. 1, 2018 Issued a $331,700 note to customer Abe Willis as terms of a merchandise sale. The merchandise's cost to Telesco is $125,900. Note contract terms included a 36-month maturity date, and a 8% annual interest rate. Dec. 31, 2018 Telesco records interest accumulated for 2018. Dec. 31, 2019 Telesco records interest accumulated for 2019. Dec. 31, 2020 Abe Willis honors the note and pays in full with cash. If an amount box does not require an entry, leave it blank. Jan. 1, 2018 To record sale in exchange for Notes Receivable: Willis, 36-month maturity, 8% interest rate Jan. 1, 2018 To record the cost of sale Dec. 31, 2018 To record interest accumulated in 2018 88 Dec. 31, 2019 To record interest accumulated in 2019 Dec. 31, 2020 Previousarrow_forwardCurrent Attempt in Progress Presented below is information related to Sheridan Company for its first month of operations. Jan. 06 Jan. 10 Jan. 23 Balance of Credit Purchases Gorst Company Tian Company Accounts Payable $9,000 11,800 Maddox Company 12,300 $ Gorst Company Jan. 11 Determine the balances that appear in the accounts payable subsidiary ledger. What Accounts Payable balance appears in the general ledger at the end of January? $ Jan. 16 Jan. 29 Cash Paid Gorst Company Tian Company Maddox Company Subsidary Ledger Tian Company 69 $6,800 11,800 7,400 $ Maddox Company $ General Ledgearrow_forward

- Required information [The following information applies to the questions displayed below.] Tyrell Company entered into the following transactions involving short-term liabilities. Year 1 April 20 Purchased $40,250 of merchandise on credit from Locust, terms n/30. May 19 Replaced the April 20 account payable to Locust with a 90-day, 10%, $35,000 note payable along with paying $5,250 in cash. July 8 Borrowed $80,000 cash from NBR Bank by signing a 120-day, 9%, $80,000 note payable. Paid the amount due on the note to Locust at the maturity date. Paid the amount due on the note to NBR Bank at the maturity date. November 28 Borrowed $42,000 cash from Fargo Bank by signing a 60-day, 88, $42,000 note payable. December 31 Recorded an adjusting entry for accrued interest on the note to Fargo Bank. Year 2 ? Paid the amount due on the note to Fargo Bank at the maturity date. 4. Determine the interest expense recorded in Year 2. Note: Do not round your Intermediate calculations. Use 360 days a…arrow_forwardThe Lawrence Company records its trade accounts payable net of any cash discounts. At the end of 2016, Lawrence had a balance of $300,000 in its trade accounts payable account before any adjustments related to the following items: 1. Goods shipped to Lawrence FOB shipping point were in transit on December 31. The invoice price of the goods was $50,000, with a 2% discount allowed for prompt payment. 2. Goods shipped to Lawrence FOB destination on December 29 arrived on January 2, 2017. The invoice price of the goods was $9,000, with a 4% discount allowed for payment within 20 days. 3. On December 10, Lawrence had recorded a shipment received. The recorded invoice price was $24,750, net, with a 1% discount allowed for payment within 14 days. At the end of the year, payment had not been made. At what amount should Lawrence report trade accounts payable on its December 31, 2016 balance sheet? a. $349,000 b. $357,930 c. $357,680 d. $349,250arrow_forwardRequired information [The following information applies to the questions displayed below.] Tyrell Company entered into the following transactions involving short-term liabilities. Year 1 April 20 Purchased $40,250 of merchandise on credit from Locust, terms n/30. May 19 Replaced the April 20 account payable to Locust with a 90-day, 109, $35,000 note payable along with paying $5,250 in cash. July 8 Borrowed $80,000 cash from NBR Bank by signing a 120-day, 98, $80,000 note payable. ?Paid the amount due on the note to Locust at the maturity date. ? Paid the amount due on the note to NBR Bank at the maturity date. November 28 Borrowed $42,000 cash from Fargo Bank by signing a 60-day, 8%, $42,000 note payable. December 31 Recorded an adjusting entry for accrued interest on the note to Fargo Bank. Year 2 Paid the amount due on the note to Fargo Bank at the maturity date. 5. Prepare journal entries for all the preceding transactions and events. View transaction list Journal entry worksheet…arrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning