Concept explainers

Videos

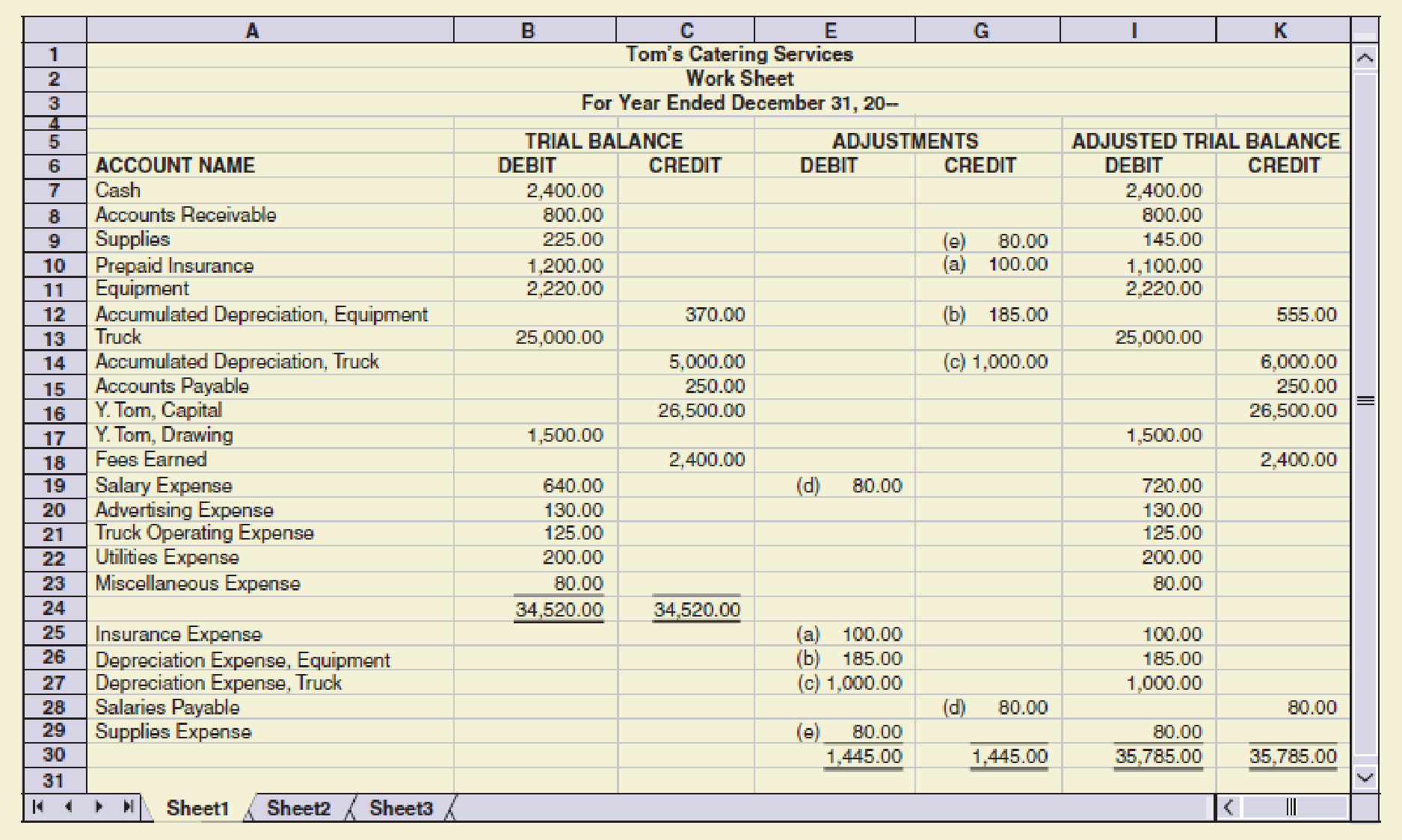

Tom’s Catering Services prepared the following work sheet for the year ended December 31, 20--.

Required

1. Complete the work sheet. (Skip this step if using QuickBooks or general ledger.)

2. Prepare an income statement.

3. Prepare a statement of owner’s equity; assume that there was an additional investment of $2,500 on December 1. (Skip this step if using QuickBooks. The additional investment assumption has already been completed in the data file.)

4. Prepare a

5. Journalize the closing entries with the four steps in the correct sequence.

6. Prepare a post-closing

Check Figure

Net income, $19,567

Trending nowThis is a popular solution!

Chapter 5 Solutions

College Accounting (Book Only): A Career Approach

- Prepare journal entries to record the following transactions that occurred in March: A. on first day of the month, purchased building for cash, $75,000 B. on fourth day of month, purchased inventory, on account, $6,875 C. on eleventh day of month, billed customer for services provided, $8,390 D. on nineteenth day of month, paid current month utility bill, $2,000 E. on last day of month, paid suppliers for previous purchases, $2,850arrow_forwardLeanders Landscaping Service maintains the following chart of accounts: The following transactions were completed by Leander: Required 1. Journalize the transactions in the general journal. Prepare a brief explanation for each entry. 2. If you are using working papers, write the name of the owner on the Capital and Drawing accounts. 3. Post the journal entries to the general ledger accounts. (Skip this step if you are using CLGL.) 4. Prepare a trial balance dated April 30, 20. If you are using CLGL, use the year 2020 when recording transactions and preparing reports.arrow_forwardFor this week's assignment, you are required to read the lecture notes and review the supporting resources, then complete the below financial statements from the information provided. Please support your analysis with at least 2 references. All assignments must be in the APA format. Scenario 1: The following are balance sheet accounts for ABC Event Company for end of year (December 31, 20XX). Please note that: (the company paid $2, 500 in cash for the equipment and financed the remaining $6,500 with a loan from the bank.) Accounts payable $ 6, 500 Accounts receivable 4, 800 Cash 1,500 Equipment 9,000 Equipment Software 500 Notes payable 6, 500 Owner's equity? Required: Find the missing account balance. Prepare a simplified balance sheet from the information. Consider the ABC Event Company scenario in the lecture notes. Provide a brief description of your analysis. Scenario 2: Income Statement for ABC Event Company ABC Event Company's food and beverage costs for the year were $35,000.…arrow_forward

- Locate Gap Inc.’s 2020 Annual Report (for fiscal year 2/2/20-1/30/21) There are 10 sections of questions. You will find the information necessary to answer the questions in “Item 8. Financial Statements and Supplementary Data,” of the report. Read through the questions carefully and answer in the space provided. What are the following amounts at 1/30/21: Total Assets : Total Liabilities: Total Owner’s Equity : At 1/30/21: What is the percentage of debt used to finance Gap? What is the percentage of owner’s equity used to finance Gap? What is the significance of these two percentages?arrow_forwardWilliams Mechanic Services prepared the following work sheet for the year ended March 31,20--. Required 1. Complete the work sheet. (Skip this step if using CLGL.) 2. Prepare an income statement. 3. Prepare a statement of owners equity. Assume that there was an additional investment of 5,000 on March 13. 4. Prepare a balance sheet. 5. Journalize the closing entries using the four steps in the correct sequence. 6. Prepare a post-dosing trial balance. Check Figure Post-closing trial balance total, 31,765arrow_forwardMy text book is Hospitality Industry Financial Accounting (4th edition). I am in chapter 12 -- CURRENT LIABILITIES AND PAYROLL now. There is a question asks me to do two following works: 1. Prepare the necessary journal entry to record the payroll of Hotel Properties, Inc., on February 15, 20X1. 2. Prepare the journal entry that would be made on the date the payroll was actually paid. The scenario is "You have been asked to prepare the entry to record the payroll on February 15, 20X1, for Hotel Properties, Inc. The gross wages are $8,000 for administrative salaries and $6,000 for sales salaries. The federal income tax rate is 28 percent, the state income tax rate is 4.6 percent, and the FICA rate is 7.65 percent for all employees. All wages are subject to these taxes. In addition to taxes withheld, the employer has withheld $128 for the employees contribution to health insurance plan."arrow_forward

- My text book is Hospitality Industry Financial Accounting (4th edition). I am in chapter 12 -- CURRENT LIABILITIES AND PAYROLL now. There is a question asks me to do two tasks. 1. Prepare the necessary journal entry to record the payroll of Hotel Properties, Inc., on February 15, 20x1. 2. Prepare the journal entry that would be made on the date the payroll was actually paid. The scenario is the following: You have been asked to prepare the entry to record the payroll on February 15, 20x1, for Hotel Properties, Inc. The gross wages are $8,000 for administrative salaries and $6,000 for sales salaries. The federal income tax rate is 28 percent, the state income tax rate is 4.6 percent, and the FICA rate is 7.65 percent for all employee. All wages are subject to these taxes. In addition to taxes withheld, the employer has withheld $128 for the employees' contribution to a health insutance plan.arrow_forwardSolar Solutions began operations on January 1, 2015, and is now in its sixth year of operations. It is a retail sales company with a large amount of online sales. The adjusted trial balance as of December 31, 2020 appears below, along with prior year balance sheet data and some additional transaction data for 2020. SOLAR SOLUTIONS Adjusted Trial Balance 12/31/2020 2020 2019 Account Title Adjusted Trial Balance Post-Closing Trial Balance Debit Credit Debit Credit Cash $ 122,200 55,000 125,600 Accounts Receivable 35,000 Prepaid Insurance 5,000 6,000 |Inventory Office Equipment Machinery & Tools Accumulated Depreciation Accounts Payable Salaries Payable Sales Tax Payable Note Payable-Long Term Common Stock, $10 par 46,000 15,600 63,000 47,000 59,000 21,000 21,000 16,000 11,200 16,800 2,600 2,700 2,000 4,000 31,000 22,100 240,000 160,000 Retained Earnings 28,600 28,600 Dividends 10,000 Sales Revenue Cost of Goods Sold Rent Expense Salaries Expense 235,000 127,600 20,000 36,000 Insurance…arrow_forwardBeacon Signals Company maintains and repairs warning lights, such as those found on radio towers and lighthouses. Beacon Signals Company prepared the following end-of-period spreadsheet at December 31, 2019, the end of the fiscal year: Required: Prepare an income statement for the year ended December 31. Prepare a statement of owner’s equity for the year ended December 31. No additional investments were made during the year. Prepare a balance sheet as of December 31. Based upon the end-of-period spreadsheet, journalise the closing entries. Prepare a post-closing trial balance.arrow_forward

- Required:Prepare the following accounts in the general ledger of Hogwarts Traders for the financial year ended 31 December 2019 ONLY. Start with the opening balances. Balance the accounts at the end of the month. Ignore VAT.‐ Vehicles‐ Accumulated depreciation: Vehicles‐ Depreciation ‐ Asset Disposal ‐ Profit/Loss on sale of vehicles.Show all your workings.arrow_forwardFor the months November, December, and January, I have been tasked to find the Current Liabilites, net income, debt ratio, and Return on equity. I have already began work on this assignment and would like some confirmation of my findings as well as work shown for how your answers were found so I can see my errors if any were made. Thank you.arrow_forwardYou have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance. After showing your analysis to the controller, he tells you to change the aging category of a large account from over 120 days to current status and to prepare a new invoice to the customer with a revised date that agrees with the new category. This will change the required allowance for uncollectible accounts…arrow_forward

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage- Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College