Concept explainers

Videos

The

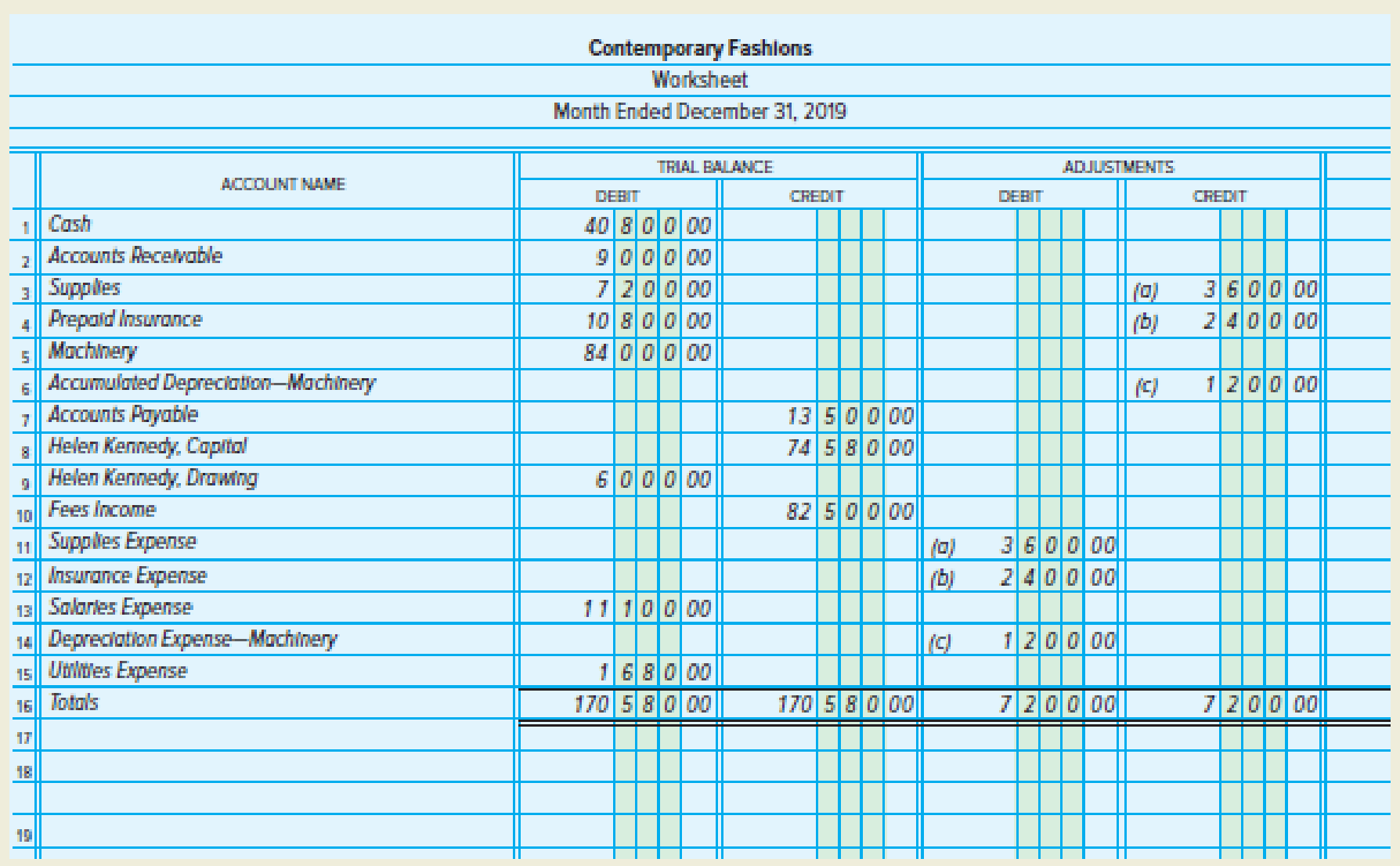

ADJUSTMENTS

- a. Supplies used, $3,600

- b. Expired insurance, $2,400

- c.

Depreciation expense for machinery, $1,200

INSTRUCTIONS

- 1. Complete the worksheet.

- 2. Prepare an income statement.

- 3. Prepare a statement of owner’s equity.

- 4. Prepare a

balance sheet . - 5. Journalize the

adjusting entries in the general journal, page 3. - 6. Journalize the closing entries in the general journal, page 4.

- 7. Prepare a postclosing trial balance.

Analyze: If the adjusting entry for expired insurance had been recorded in error as a credit to Insurance Expense and a debit to Prepaid Insurance for $2,400, what reported net income would have resulted?

1.

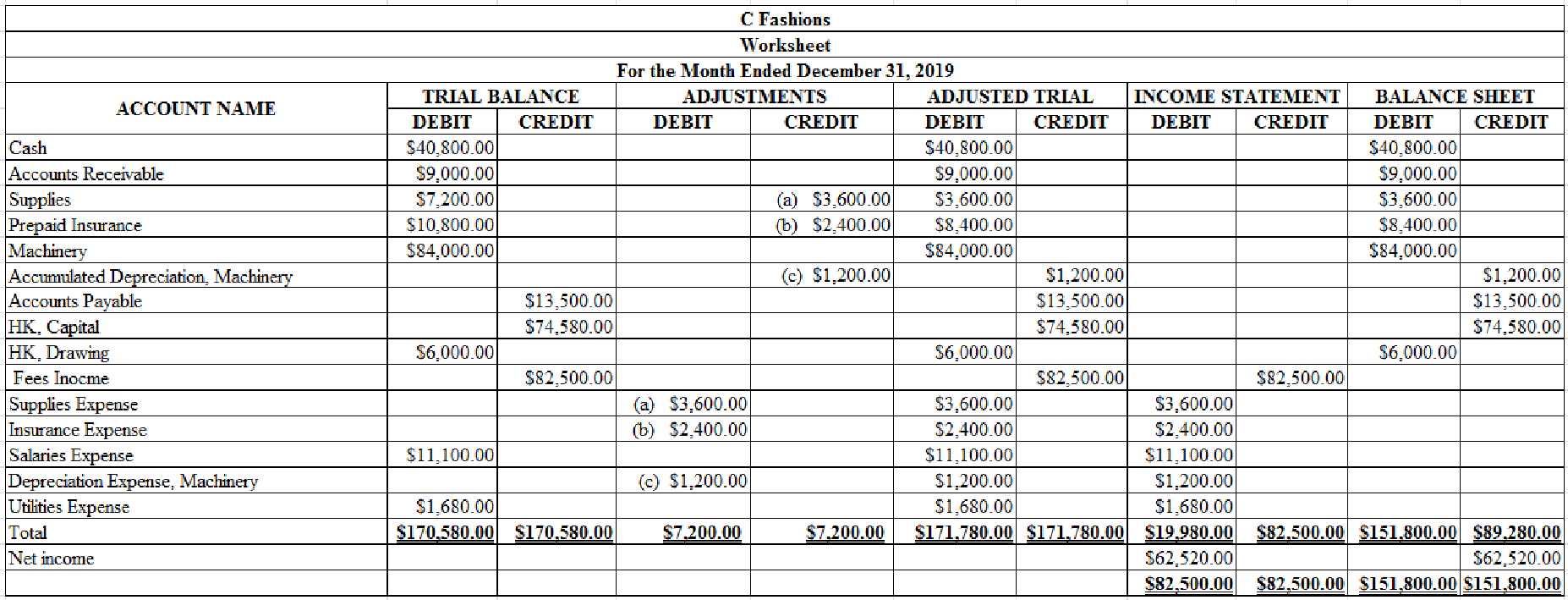

Complete the worksheet for C Fashions for the month ended December 31, 2019.

Explanation of Solution

Worksheet: Worksheet is an accounting tool that helps accountants to record adjustments and up-date balances required to prepare financial statements. Worksheet is a central place where trial balance, adjustments, adjusted trial balance, income statement, and balance sheet are presented.

Complete the worksheet for C Fashions for the month ended December 31, 2019.

Table (1)

2.

Prepare income statement for C Fashions for the month of December 31, 2019.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operation and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare an income statement for C Fashions for the month ended December 31, 2019.

| C Fashions | ||

| Income Statement | ||

| For the Month Ended December 31, 2019 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenues: | ||

| Fees Income | 82,500 | |

| Expenses: | ||

| Supplies Expense | 3,600 | |

| Insurance Expense | 2,400 | |

| Salaries Expense | 11,100 | |

| Depreciation Expense, Machinery | 1,200 | |

| Utilities Expense | 1,680 | |

| Total expenses | 19,980 | |

| Net income | $62,520 | |

Table (2)

3.

Prepare statement of owners’ equity for C Fashions for the month of December 31, 2019.

Explanation of Solution

Statement of owners’ equity: This statement reports the beginning owner’s equity and all the changes which led to ending owners’ equity. Additional capital, net income from income statement is added to, and drawings are deducted from beginning owner’s equity to arrive at the end result, ending owner’s equity.

Prepare a statement of owners’ equity for C Fashions for the month ended December 31, 2019.

| C Fashions | ||

| Statement of Owners’ Equity | ||

| For the Month Ended December 31, 2019 | ||

| Particulars | Amount ($) | Amount ($) |

| HK, Capital, December 1, 2019 | $74,580 | |

| Net income for December | 62,520 | |

| Less: Withdrawals for December | 6,000 | |

| Increase in capital | 56,520 | |

| HK, Capital, December 31, 2019 | $131,100 | |

Table (3)

4.

Prepare balance sheet for C Fashions for the month of December 31, 2019.

Explanation of Solution

Balance sheet: This financial statement reports a company’s resources (assets) and claims of creditors (liabilities) and owners (owners’ equity) over those resources. The resources of the company are assets which include money contributed by owners and creditors. Hence, the main elements of the balance sheet are assets, liabilities, and owners’ equity.

Prepare the balance sheet for C Fashions as at December 31, 2019.

| C Fashions | ||

| Balance Sheet | ||

| December 31, 2019 | ||

| Assets | Amount ($) | Amount ($) |

| Cash | $40,800 | |

| Accounts Receivable | 9,000 | |

| Supplies | 3,600 | |

| Prepaid Insurance | 8,400 | |

| Machinery | $84,000 | |

| Less: Accumulated Depreciation | 1,200 | 82,800 |

| Total Assets | $144,600 | |

| Liabilities and owner’s equity | ||

| Liabilities | ||

| Accounts Payable | 13,500 | |

| Owners’ Equity | ||

| HK, Capital | 131,100 | |

| Total Liabilities and Owners’ Equity | $144,600 | |

Table (4)

5.

Prepare adjusting entry for the given transactions in general ledger.

Explanation of Solution

Adjusting entries: Adjusting entries are those entries which are recorded at the end of the year, to update the income statement accounts (revenue and expenses) and balance sheet accounts (assets, liabilities, and owners’ or stockholders’ equity) to maintain the records according to accrual basis principle and matching concept.

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Prepare adjusting entry for supplies.

| GENERAL JOURNAL | Page 3 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| December 31, 2019 | Supplies expense | 3,600 | ||

| Supplies | 3,600 | |||

| (To record supplies used) | ||||

Table (5)

Description:

- Supplies Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Supplies are an asset account. Since amount of supplies is used, asset account decreased, and a decrease in asset is credited.

Prepare adjusting entry for insurance expense:

| GENERAL JOURNAL | Page 3 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| December 31, 2019 | Insurance expense | 2,400 | ||

| Prepaid Insurance | 2,400 | |||

| (To record part of prepaid insurance expired) | ||||

Table (6)

Description:

- Insurance Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Prepaid Insurance is an asset account. Since amount of insurance is expired, asset account decreased, and a decrease in asset is credited.

Prepare adjusting entry for depreciation expense-Machinery:

| GENERAL JOURNAL | Page 3 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| December 31, 2019 | Depreciation expense-Machinery | 1,200 | ||

| Accumulated depreciation-Machinery | 1,200 | |||

| (To record depreciation expense) | ||||

Table (7)

Description:

- Depreciation Expense, Machinery is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Accumulated Depreciation, Machinery is a contra-asset account, and contra-asset accounts would have a normal credit balance, hence, the account is credited.

6.

Prepare closing entries for the given transactions in general ledger.

Explanation of Solution

Closing entries: The journal entries prepared to close the temporary accounts to capital account are referred to as closing entries. The revenue, expense, and drawing accounts are referred to as temporary accounts because the information and figures in these accounts is held temporarily and consequently transferred to permanent account at the end of accounting year.

Steps in closing procedure:

- 1. Close the revenue accounts to Income Summary account.

- 2. Close the expense accounts to Income Summary account.

- 3. Close the Income Summary account and transfer the net income or net loss balance to the Capital account.

- 4. Close the Drawing account to Capital account.

Close the revenue accounts to Income Summary account.

| GENERAL JOURNAL | Page 4 | |||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| 2019 | Fees Income | 82,500 | ||||

| December | 31 | Income Summary | 82,500 | |||

| (Record closing of revenue to Income Summary account) | ||||||

Table (8)

Description:

- Fees income is a revenue account. Revenue account has a normal credit balance. Since revenue is closed to Income Summary account, the account is debited.

- Income Summary is a clearing account which closes revenue, expense, drawings, and net of revenues and expenses to capital accounts. The account is credited to hold the transferred balance from revenue account.

Close the expense accounts to Income Summary account.

| GENERAL JOURNAL | Page 4 | |||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| 2019 | Income Summary | 19,980 | ||||

| December | 31 | Supplies Expense | 3,600 | |||

| Insurance Expense | 2,400 | |||||

| Salaries Expense | 11,100 | |||||

| Depreciation Expense, Machinery | 1,200 | |||||

| Utilities Expense | 1,680 | |||||

| (Record closing of expenses to Income Summary account) | ||||||

Table (9)

Description:

- Income Summary is a clearing account which closes revenue, expense, drawings, and net of revenues and expenses to capital accounts. The account is debited to hold the transferred balance from expense accounts.

- Supplies Expense, Insurance Expense, Salaries Expense, Depreciation Expense, and Utilities Expense are expense accounts. Expense account has a normal debit balance. Since expenses are closed to Income Summary account, the accounts are credited.

Close the net income to Income Summary account.

| GENERAL JOURNAL | Page 4 | |||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| 2019 | Income Summary | 62,520 | ||||

| December | 31 | HK, Capital | 62,520 | |||

| (Record closing of net income to capital account) | ||||||

Table (10)

Description:

- Income Summary is a clearing account which closes revenue, expense, drawings, and net of revenues and expenses to capital accounts. Since net income is closed, the account is reversed; hence, the Income Summary account is debited.

- HK, Capital is a capital account. Since net income is transferred to the account, the value increased, and an increase in capital is credited.

Working Note 1:

Compute net income.

Close the Drawing account to Capital account.

| GENERAL JOURNAL | Page 4 | |||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| 2019 | HK, Capital | 6,000 | ||||

| December | 31 | HK, Drawing | 6,000 | |||

| (Record closing of drawing to capital account) | ||||||

Table (11)

Description:

- HK, Capital is a capital account. Since drawings are transferred to the account, the value decreased, and a decrease in capital is debited.

- HK, Drawing is a capital account. Since drawings are transferred, the account is credited to reverse the previously debited effect.

7.

Prepare a post-closing trial balance for C Fashions at December 31, 2019.

Explanation of Solution

Post-closing trial balance: Post-closing trial balance is a summary of all the assets, liabilities, and capital accounts and their balances, after the closing entries are prepared. So, post-closing trial balance reports the balances of permanent accounts only.

Prepare a post-closing trial balance for C Fashions at December 31, 2019.

|

C Fashions Post- closing Trial Balance December 31, 2019 | ||

| Account Title |

Debit ($) |

Credit ($) |

| Cash | 40,800 | |

| Accounts Receivable | 9,000 | |

| Supplies | 3,600 | |

| Prepaid Insurance | 8,400 | |

| Machinery | 84,000 | |

| Accumulated Depreciation | 1,200 | |

| Accounts Payable | 13,500 | |

| HK, Capital | 131,100 | |

| Total | 145,800 | 145,800 |

Table (12)

Analyze: If expired insurance is wrongly adjusted as a credit to insurance expense and a debit to prepaid insurance for $2,400, then the net income would be increased by $4,800. The amount of net income would be reported as $67,320

Want to see more full solutions like this?

Chapter 6 Solutions

COLLEGE ACCOUNTING (LL)W/ACCESS>CUSTOM<

- Prepare adjusting journal entries, as needed, considering the account balances excerpted from the unadjusted trial balance and the adjustment data. A. amount due for employee salaries, $4,800 B. actual count of supplies inventory, $ 2,300 C. depreciation on equipment, $3,000arrow_forwardBased on the data presented in Exercise 6-25, journalize the closing entries. On March 31, 2019, the balances of the accounts appearing in the ledger of Racine Furnishings Company, a furniture wholesaler, are as follows: a. Prepare a multiple-step income statement for the year ended March 31, 2019. b. Compare the major advantages and disadvantages of the multiple-step and single-step forms of income statements.arrow_forwardFollowing is the adjusted trial balance data for Garage Parts Unlimited as of December 31, 2019. A. Use the data provided to compute net sales for 2019. B. Compute the gross margin or 2019. C. Compute the gross profit margin ratio (rounded to nearest hundredth) D. Prepare a simple income statement for the year ended December 31, 2019. E. Prepare a multi-step income statement for the year ended December 31, 2019.arrow_forward

- The following selected accounts and their current balances appear in the ledger of Clairemont Co. for the fiscal year ended May 31, 2019: Instructions 1. Prepare a multiple-step income statement. 2. Prepare a statement of owners equity. 3. Prepare a balance sheet, assuming that the current portion of the note payable is 50,000. 4. Briefly explain how multiple-step and single-step income statements differ.arrow_forwardOn March 31, 2019, the balances of the accounts appearing in the ledger of Racine Furnishings Company, a furniture wholesaler, are as follows: a. Prepare a multiple-step income statement for the year ended March 31, 2019. b. Compare the major advantages and disadvantages of the multiple-step and single-step forms of income statements.arrow_forwardLeanders Landscaping Service maintains the following chart of accounts: The following transactions were completed by Leander: Required 1. Journalize the transactions in the general journal. Prepare a brief explanation for each entry. 2. If you are using working papers, write the name of the owner on the Capital and Drawing accounts. 3. Post the journal entries to the general ledger accounts. (Skip this step if you are using CLGL.) 4. Prepare a trial balance dated April 30, 20. If you are using CLGL, use the year 2020 when recording transactions and preparing reports.arrow_forward

- Assume the following data for Oshkosh Company before its year-end adjustments: Journalize the adjusting entries for the following: a. Estimated customer refunds and allowances b. Estimated customer returnsarrow_forwardThe following accounts appear in the ledger of Celso and Company as of June 30, the end of this fiscal year. The data needed for the adjustments on June 30 are as follows: ab.Merchandise inventory, June 30, 54,600. c.Insurance expired for the year, 475. d.Depreciation for the year, 4,380. e.Accrued wages on June 30, 1,492. f.Supplies on hand at the end of the year, 100. Required 1. Prepare a work sheet for the fiscal year ended June 30. Ignore this step if using CLGL. 2. Prepare an income statement. 3. Prepare a statement of owners equity. No additional investments were made during the year. 4. Prepare a balance sheet. 5. Journalize the adjusting entries. 6. Journalize the closing entries. 7. Journalize the reversing entry as of July 1, for the wages that were accrued in the June adjusting entry. Check Figure Net income, 14,066arrow_forwardRequired: Prepare the following, December 31, 2019, financial statements: Income Statement Retained Earnings Statement Balance Sheet December 31, 2019, adjusted trial balance is provided below. Prepare the fiscal year-end closing entries. a. Prepare the January 1, 2020 opening trial balance. b. Prepare the journal entries for the first six months of 2020. provided is a summary of activities accounting entries that need to be prepared 2. The owners would like to know the current (as of 6/30/20) cash and the inventory balance. They would like you to provide a “T” account showing the activity in each account.arrow_forward

- Devlin Company has prepared following partially completed worksheet for the year ended December 31, 2019: 1. Complete the worksheet. (Round to the nearest dollar.) 2. Prepar company's financial statements. 3. Prepare (a) adjusting and (b ) closing entries in the general journal.arrow_forwardOn November 30, 2019, Davis Company and the following account balances: 1. Prepare general journal entries to record preceding transactions. 2. Post to general ledger T-accou11ts. 3. Prepare a year-end trial balance on a worksheet and complete the worksheet using the following information: (a) accrued salaries at year-end total $1,200; (b ) for simplicity, the building and equipment are being depreciated using the stright-line method over an estimated life of 20 years with no residual all c) supplies on hand at the end of the year total $630; (d ) bad debts expense for the year totals $830; and (e ) the income tax rate is 30%; income taxes are payable in the first quarter of 2020. 4. Prepare company's financial statements for 2019 . 5. Prepare 2019 (a) adjusting and (b) closing entries in the general journal.arrow_forwardPrepare the January 1, 2020 opening trial balance. Prepare the journal entries for the first six months of 2020. The owners would like to know the current (as of 6/30/20) cash and inventory They would like you to provide a “T” account showing the activity in each account.arrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

- Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College