Videos

Interest Rate Risk [LO2] Both Bond Sam and Bond Dave have 6.5 percent coupons, make semiannual payments, and are priced at par value. Bond Sam has 3 years to maturity, whereas Bond Dave has 20 years to maturity. If interest rates suddenly rise by 2 percent what is the percentage change in the price of Bond Sam? Of Bond Dave? If rates were to suddenly fall by 2 percent instead, what would the percentage change in the price of Bond Sam be then? Of Bond Dave? Illustrate your answers by graphing

To determine: The percentage change in bond price

Introduction:

A bond refers to the debt securities issued by the governments or corporations for raising capital. The borrower does not return the face value until maturity. However, the investor receives the coupons every year until the date of maturity.

Bond price or bond value refers to the present value of the future cash inflows of the bond after discounting at the required rate of return.

Answer to Problem 19QP

The percentage change in bond price is as follows:

| Yield to maturity | Bond S | Bond D |

| 4.5% | (5.19%) | (19.07%) |

| 8.5% | 5.55% | 26.19% |

The interest rate risk is high for a bond with longer maturity, and the interest rate risk is low for a bond with shorter maturity period. The maturity period of Bond S is 3 years, and the maturity period of Bond D is 20 years. Hence, the Bond D’s bond price fluctuates higher than the bond price of Bond S due to longer maturity.

Explanation of Solution

Given information:

There are two bonds namely Bond S and Bond D. The coupon rate of both the bonds is 6.5 percent. The bonds pay the coupons semiannually. The price of the bond is equal to its par value. Assume that the par value of both the bonds is $1,000. Bond S will mature in 3 years, and Bond D will mature in 20 years.

Formulae:

The formula to calculate the bond value:

Where,

“C” refers to the coupon paid per period

“F” refers to the face value paid at maturity

“r” refers to the yield to maturity

“t” refers to the periods to maturity

The formula to calculate the percentage change in price:

Determine the current price of Bond S:

Bond S is selling at par. It means that the bond value is equal to the face value. It also indicates that the coupon rate of the bond is equal to the yield to maturity of the bond. As the par value is $1,000, the bond value or bond price of Bond S will be $1,000.

Hence, the current price of Bond S is $1,000.

Determine the current yield to maturity on Bond S:

As the bond is selling at its face value, the coupon rate will be equal to the yield to maturity of the bond. The coupon rate of Bond S is 6.5 percent.

Hence, the yield to maturity of Bond S is 6.5 percent.

Determine the current price of Bond D:

Bond D is selling at par. It means that the bond value is equal to the face value. It also indicates that the coupon rate of the bond is equal to the yield to maturity of the bond. As the par value is $1,000, the bond value or bond price of Bond D will be $1,000.

Hence, the current price of Bond D is $1,000.

Determine the current yield to maturity on Bond D:

As the bond is selling at its face value, the coupon rate will be equal to the yield to maturity of the bond. The coupon rate of Bond D is 6.5 percent.

Hence, the yield to maturity of Bond D is 6.5 percent.

The percentage change in the bond value of Bond S and Bond D when the interest rates rise by 2 percent:

Compute the new interest rate (yield to maturity) when the interest rates rise:

The interest rate refers to the yield to maturity of the bond. The initial yield to maturity of the bonds is 6.5 percent. If the interest rates rise by 2 percent, then the new interest rate or yield to maturity will be 8.5 percent

Compute the bond value when the yield to maturity of Bond S rises to 8.5 percent:

The coupon rate of Bond S is 6.5 percent, and its face value is $1,000. Hence, the annual coupon payment is $65

The yield to maturity is 8.5 percent. As the calculations are semiannual, the yield to maturity should also be semiannual. Hence, the semiannual yield to maturity is 4.25 percent

The remaining time to maturity is 3 years. As the coupon payment is semiannual, the semiannual periods to maturity are 6

Hence, the bond price of Bond S will be $948.0026 when the interest rises to 8.5 percent.

Compute the percentage change in the price of Bond S when the interest rates rise to 8.5 percent:

The new price after the increase in interest rate is $948.0026. The initial price of the bond was $1,000.

Hence, the percentage decrease in the price of Bond S is (5.19 percent) when the interest rates rise to 8.5 percent.

Compute the bond value when the yield to maturity of Bond D rises to 8.5 percent:

The coupon rate of Bond D is 6.5 percent, and its face value is $1,000. Hence, the annual coupon payment is $65

The yield to maturity is 8.5 percent. As the calculations are semiannual, the yield to maturity should also be semiannual. Hence, the semiannual yield to maturity is 4.25 percent

The remaining time to maturity is 20 years. As the coupon payment is semiannual, the semiannual periods to maturity are 40

Hence, the bond price of Bond D will be $809.2273 when the interest rises to 8.5 percent.

Compute the percentage change in the price of Bond D when the interest rates rise to 8.5 percent:

The new price after the increase in interest rate is $809.2273. The initial price of the bond was $1,000.

Hence, the percentage decrease in the price of Bond D is (19.07 percent) when the interest rates rise to 8.5 percent.

The percentage change in the bond value of Bond S and Bond D when the interest rates decline by 2 percent:

Compute the new interest rate (yield to maturity) when the interest rates decline:

The interest rate refers to the yield to maturity of the bond. The initial yield to maturity of the bonds is 6.5 percent. If the interest rates decline by 2 percent, then the new interest rate or yield to maturity will be 4.5 percent

Compute the bond value when the yield to maturity of Bond S declines to 4.5 percent:

The coupon rate of Bond S is 6.5 percent, and its face value is $1,000. Hence, the annual coupon payment is $65

The yield to maturity is 4.5 percent. As the calculations are semiannual, the yield to maturity should also be semiannual. Hence, the semiannual yield to maturity is 2.25 percent

The remaining time to maturity is 3 years. As the coupon payment is semiannual, the semiannual periods to maturity are 6

Hence, the bond price of Bond S will be $1,055.5448 when the interest declines to 4.5 percent.

Compute the percentage change in the price of Bond S when the interest rates decline to 4.5 percent:

The new price after the increase in interest rate is $1,055.5448. The initial price of the bond was $1,000.

Hence, the percentage increase in the price of Bond S is 5.55 percent when the interest rates decline to 4.5 percent.

Compute the bond value when the yield to maturity of Bond D declines to 4.5 percent:

The coupon rate of Bond D is 6.5 percent, and its face value is $1,000. Hence, the annual coupon payment is $65

The yield to maturity is 4.5 percent. As the calculations are semiannual, the yield to maturity should also be semiannual. Hence, the semiannual yield to maturity is 2.25 percent

The remaining time to maturity is 20 years. As the coupon payment is semiannual, the semiannual periods to maturity are 40

Hence, the bond price of Bond D will be $1,261.9352 when the interest declines to 4.5 percent.

Compute the percentage change in the price of Bond D when the interest rates decline to 4.5 percent:

The new price after the increase in interest rate is $1,261.9352. The initial price of the bond was $1,000.

Hence, the percentage increase in the price of Bond D is 26.19 percent when the interest rates decline to 4.5 percent.

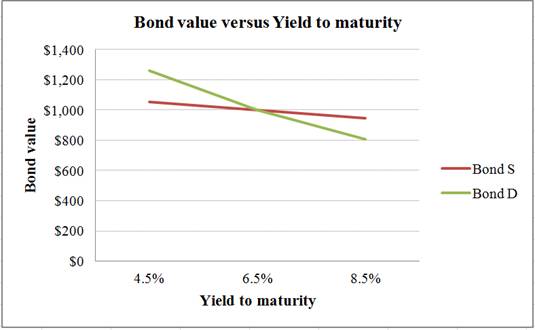

A summary of the bond prices and yield to maturity of Bond S and Bond D:

| Yield to maturity | Bond S | Bond D |

| 4.5% | $1,055.5448 | $1,261.9352 |

| 6.5% | $1,000.0000 | $1,000.0000 |

| 8.5% | $948.0026 | $809.2273 |

Table 1

A graph indicating the relationship between bond prices and yield to maturity based on Table 1:

Interpretation of the graph:

The above graph indicates that the price fluctuation is higher in a bond with higher maturity. Bond D has a maturity period of 20 years. As its maturity period is longer, its price sensitivity to the interest rates is higher. Bond S has a maturity period of 3 years. As its maturity period is shorter, its price sensitivity to the interest rates is lower. Hence, a bond with longer maturity is subject to higher interest rate risk.

Want to see more full solutions like this?

Chapter 7 Solutions

Fundamentals of Corporate Finance

- 5. Both Bond Sam and Bond Dave have 6 percent coupons, make semiannual payments, and are priced at par value. Bond Sam has 4 years to maturity, whereas Bond Dave has 19 years to maturity. a. If interest rates suddenly rise by 3 percent, what is the percentage change in the price of Bond Sam? b. If interest rates suddenly rise by 3 percent, what is the percentage change in the price of Bond Dave? c. If rates were to suddenly fall by 3 percent instead, what would the percentage change in the price of Bond Sam be then d. If rates were to suddenly fall by 3 percent instead, what would the percentage change in the price of Bond Dave be then?arrow_forward= = Problem 2 Currently the yield curve observed in the market is as follows: yı 6%, Y2 = 7%, and yз 9%. You are choosing between a two-year and three-year maturity bonds all paying annual coupons of 8%, once a year. You strongly believe that at the end of year 1 the yield curve will become flat at 9%. (1) Which bond (and why) should you buy if you plan to close out your position in one year right after receiving the coupon payment? (2) Suppose that you can either invest in a two-year bond described above, or invest in a 1-year bank deposit with an annual interest rate of 6%. As in (a), your investment horizon is 1 year. Which option would you choose and why?arrow_forward[EXCEL] Zero coupon bonds: Diane Carter is interested in buying a five-year zero coupon bond with a face value of $1,000. She understands that the market interest rate for similar investments is 9 percent. Assume annual coupon payments. What is the current value of this bond? Please use Excelarrow_forward

- Both Bond Tony and Bond Peter have 10 per cent coupons, make semi-annual payments, and are priced at par value. Bond Tony has 3 years to maturity, whereas Bond Peter has 20 years to maturity. If interest rates suddenly rise by 2 per cent, what is the percentage change in the price of Bond Tony? Of Bond Peter? AS F5 F6 F3 三 F1 F2 F4 Escarrow_forward5 The YTM on a bond is the interest rate you earn on your investment if interest rates don't change. If you actually sell the bond before it matures, your realized return is known as the holding period yield (HPY). a. Suppose that today you buy an annual coupon bond with a coupon rate of 8.2 percent for $845. The bond has 10 years to maturity and a par value of $1,000. What rate of return do you expect to earn on your investment? Note: Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16. b-1. Two years from now, the YTM on your bond has declined by 1 percent, and you decide to sell. What price will your bond sell for? Note: Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16. b-2. What is the HPY on your investment? Note: Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16. eBook a. Rate of return b-1. Price b-2. Holding…arrow_forward4. Calculating Returns [LO1] Suppose you bought a bond with an annual coupon of 7 percent one year ago for $1,010. The bond sells for $985 today. a. Assuming a $1,000 face value, what was your total dollar return on this investment over the past year? b. What was your total nominal rate of return on this investment over the past year? c. If the inflation rate last year was 3 percent, what was your total real rate of return on this investment?arrow_forward

- Bond J has a coupon rate of 3 percent. Bond K has a coupon rate of 9 percent. Both bonds have 18 years to maturity, make semiannual payments, and have a face value of $1000 and a YTM of 6 percent. a. If interest rates suddenly rise by 2 percent, what is the percentage price change of these bonds? What if rates suddenly fall by 2 percent instead? (Hint: % price change = 100% * (new price - old price)/old price) b. What does this problem tell you about the interest rate risk of lower coupon bonds? -arrow_forwardIllustrate your answers by graphing bond prices versus time to LO 2 19. Interest Rate Risk Both Bond Bill and Bond Ted have 5.8 percent coupons, make semiannual payments, and are priced at par value. Bond Bill has 5 years to maturity, whereas Bond Ted has 25 years to maturity. If interest rates suddenly rise by 2 percent, what is the percentage change in the price of Bond Bill? Of Bond Ted? Both bonds have a par value of $1,000. If rates were to suddenly fall by 2 percent instead, what would the percentage change in the price of Bond Bill be then? Of Bond Ted? Illustrate your answers by graphing bond prices versus YTM. What does this problem tell you about the interest rate risk of longer-term bonds?arrow_forwardEXPECTATIONS THEORY Assume that the real risk-free rate is 2% and that the risk premium is zero. If a 1-year Treasury bond yield is 5% and a 2-year Treasury bond yields 7%, what is the 1-year interest rate that is expected for Year 2? Calculate this yield using a geometric average. What inflation rate is expected during Year 2? Comment on why the average interest rate during the 2-year period differs from the 1-year interest rate expected for Year 2. 6-15 maturityarrow_forward

- Suppose that discount bond prices are as follows: 2 3 4 P. 0.9525 0.899 0.838 0.760 0.05 0.065 0.054 0.070 A customer would like to have a forward contract to borrow $20M two years from now for one vear. Can you (a bank) quote a rate for this forwardloan? Question 15 Your investment account earned 10.8% last year, inflation was 6.0% for last year. What was the real return on your account last year?arrow_forwardBond J has a coupon rate of 4%. Bond K has a coupon rate of 14%. Both bonds have 17 years to maturity, a par value of $1000 and a yield to maturity of 8% , and both make semi annual payments. If interest rates suddenly rise by 2%, what is the percentage price change in these bonds? What if rates suddenly fall by 2% instead? What does this problem tell you about interest rate risk of lower coupon bonds? Excel would be good. Thanks.arrow_forwardQ1: A 20-year bond has a coupon rate of 8 percent, and another bond of the same maturity has a coupon rate of 15 percent. If the bonds are alike in all other respects, which will have the greater relative market price decline if interest rates increase sharply? Why?arrow_forward

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education