Cornerstones of Cost Management (Cornerstones Series)

4th Edition

ISBN: 9781305970663

Author: Don R. Hansen, Maryanne M. Mowen

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

thumb_up100%

Chapter 8, Problem 40P

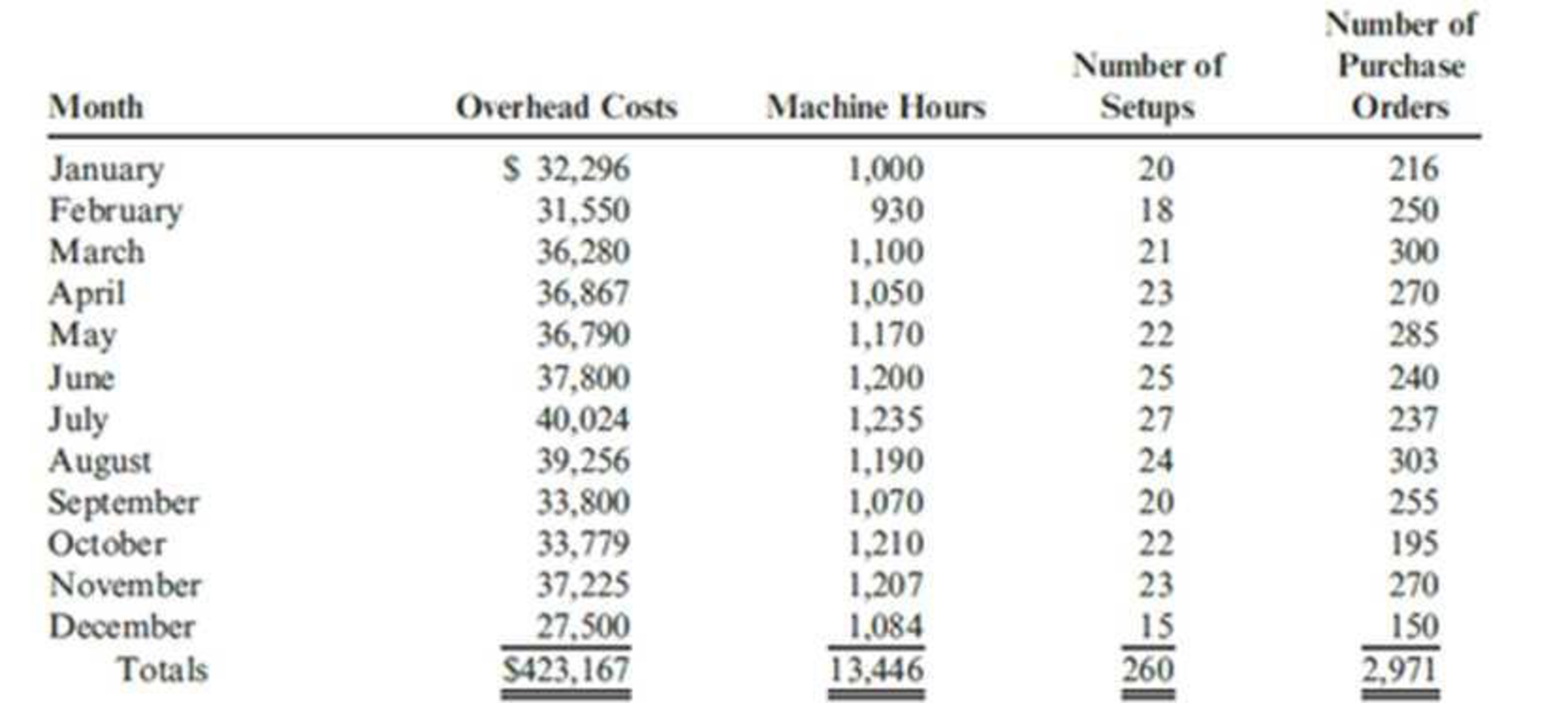

The controller for Muir Company’s Salem plant is analyzing overhead in order to determine appropriate drivers for use in flexible budgeting. She decided to concentrate on the past 12 months since that time period was one in which there was little important change in technology, product lines, and so on. Data on overhead costs, number of machine hours, number of setups, and number of purchase orders are in the following table.

Required:

- 1. Calculate an overhead rate based on machine hours using the total overhead cost and total machine hours. (Round the overhead rate to the nearest cent and predicted overhead to the nearest dollar.) Use this rate to predict overhead for each of the 12 months.

- 2. Run a regression equation using only machine hours as the independent variable. Prepare a flexible budget for overhead for the 12 months using the results of this regression equation. (Round the intercept and x-coefficient to the nearest cent and predicted overhead to the nearest dollar.) Is this flexible budget better than the budget in Requirement 1? Why or why not?

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

For many years, Yotsuya Company has used a manufacturing overhead rate based on direct labor hours. A new plant accountant has suggested that the company may be able to assign overhead costs to products more accurately by using an activity-based costing system. The accountant explains that by creating an overhead rate for each production activity that causes overhead costs, the resulting product costs will reflect an accurate measure of overhead cost. The direct material cost is P120 per unit. The budgeted hours is 8,030 direct labor hours. The accountant has identified activity centers to which overhead costs are assigned. The cost pool amounts for theses centers and their selected activity drivers for 2019:

Activity Centers

Costs

Activity Drivers

Materials handling

P60,000

1,200 times handled

Scheduling and setups

80,000

400 setups

Design section

10,750

100 changes

No. of parts

50,000

500 parts

P200,750

The company’s products…

asked that you review the company's costing system and "do what you can to help us get better control of our manufacturing

overhead costs." You find that the company has never used a flexible budget, and you suggest that preparing such a budget would be

an excellent first step in overhead planning and control.

After much effort and analysis, you determined the following cost formulas and gathered the following actual cost data for March:

Utilities

Maintenance

Supplies

Indirect labor

Depreciation

Cost Formula

$16,000+ $0.19 per machine-hour

$38,900

$1.30 per machine-hour

$0.40 per machine-hour

$94,000+ $1.20 per machine-hour

$67,500

Actual

Cost in

March

$ 22,390

Required:

1. Calculate the activity variances for March.

2. Calculate the spending variances for March.

$60,000

$ 8,200

$120, 100

$ 69,200

During March, the company worked 19,000 machine-hours and produced 13,000 units. The company had originally planned to work

21,000 machine-hours during March.

The management of Krach Corporation would like to investigate the possibility of basing its predetermined overhead rate on activity at capacity. The company's controller has provided an

example to illustrate how this new system would work. In this example, the allocation base is machine-hours and the estimated amount of the allocation base for the upcoming year is

23,000 machine-hours. Capacity is 27,000 machine-hours and the actual level of activity for the year is assumed to be 13,500 machine-hours. All of the manufacturing overhead is fixed

and both the estimated amount at the beginning of the year and the actual amount at the end of the year are assumed to be $78,300 per year. For simplicity, it is assumed that this is the

estimated manufacturing overhead for the year as well as the manufacturing overhead at capacity. It is further assumed that this is also the actual amount of manufacturing overhead for

the year.

If the company bases its predetermined overhead rate on capacity,…

Chapter 8 Solutions

Cornerstones of Cost Management (Cornerstones Series)

Ch. 8 - Define budget. How are budgets used in planning?Ch. 8 - Prob. 2DQCh. 8 - Prob. 3DQCh. 8 - What is the master budget? An operating budget? A...Ch. 8 - Explain the role of a sales forecast in budgeting....Ch. 8 - All budgets depend on the sales budget. Is this...Ch. 8 - What is an accounts receivable aging schedule? Why...Ch. 8 - Suppose that the vice president of sales is a...Ch. 8 - Suppose that the controller of your companys...Ch. 8 - Prob. 10DQ

Ch. 8 - Prob. 11DQCh. 8 - Discuss the shortcomings of the traditional master...Ch. 8 - Define static budget. Give an example that shows...Ch. 8 - What are the two meanings of a flexible budget?...Ch. 8 - What are the steps involved in building an...Ch. 8 - FlashKick Company manufactures and sells soccer...Ch. 8 - Refer to Cornerstone Exercise 8.1, through...Ch. 8 - Refer to Cornerstone Exercise 8.2 for the...Ch. 8 - Prob. 4CECh. 8 - Johnston Company cleans and applies powder coat...Ch. 8 - Play-Disc makes Frisbee-type plastic discs. Each...Ch. 8 - Refer to Cornerstone Exercise 8.6. Required: 1....Ch. 8 - Timothy Donaghy has developed a unique formula for...Ch. 8 - Green Earth Landscaping Company provides monthly...Ch. 8 - Coral Seas Jewelry Company makes and sells costume...Ch. 8 - Shalimar Company manufactures and sells industrial...Ch. 8 - Khloe Company imports gift items from overseas and...Ch. 8 - Nashler Company has the following budgeted...Ch. 8 - Refer to Cornerstone Exercise 8.13. In March,...Ch. 8 - Palmgren Company produces consumer products. The...Ch. 8 - Prob. 16ECh. 8 - Crescent Company produces stuffed toy animals; one...Ch. 8 - Audio-2-Go, Inc., manufactures MP3 players. Models...Ch. 8 - Tiger Drug Store carries a variety of health and...Ch. 8 - Rosita Flores owns Rositas Mexican Restaurant in...Ch. 8 - Prob. 21ECh. 8 - Janet Wooster owns a retail store that sells new...Ch. 8 - Historically, Ragman Company has had no...Ch. 8 - Del Spencer is the owner and founder of Del...Ch. 8 - Refer to Exercise 8.24. Del Spencers purchases...Ch. 8 - Ingles Corporation is a manufacturer of tables...Ch. 8 - In an attempt to improve budgeting, the controller...Ch. 8 - Refer to Exercise 8.27. At the end of the year,...Ch. 8 - Olympus, Inc., manufactures three models of...Ch. 8 - Refer to Exercise 8.29. Suppose Gene determines...Ch. 8 - Trumbull Co. plans to produce 100,000 toy cars...Ch. 8 - Which of the following describes the order in...Ch. 8 - A companys controller is adjusting next years...Ch. 8 - A companys sales for the coming months are as...Ch. 8 - The budget that adjusts unit sales for beginning...Ch. 8 - Ponderosa, Inc., produces wiring harness...Ch. 8 - Bernard Creighton is the controller for Creighton...Ch. 8 - Greiner Company makes and sells high-quality glare...Ch. 8 - Prob. 39PCh. 8 - The controller for Muir Companys Salem plant is...Ch. 8 - Refer to Problem 8.40 for data. Required: 1. Run a...Ch. 8 - Norton Company, a manufacturer of infant furniture...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Firenza Company manufactures specialty tools to customer order. Budgeted overhead for the coming year is: Previously, Sanjay Bhatt, Firenza Companys controller, had applied overhead on the basis of machine hours. Expected machine hours for the coming year are 50,000. Sanjay has been reading about activity-based costing, and he wonders whether or not it might offer some advantages to his company. He decided that appropriate drivers for overhead activities are purchase orders for purchasing, number of setups for setup cost, engineering hours for engineering cost, and machine hours for other. Budgeted amounts for these drivers are 5,000 purchase orders, 500 setups, and 2,500 engineering hours. Sanjay has been asked to prepare bids for two jobs with the following information: The typical bid price includes a 40 percent markup over full manufacturing cost. Required: 1. Calculate a plantwide rate for Firenza Company based on machine hours. What is the bid price of each job using this rate? 2. Calculate activity rates for the four overhead activities. What is the bid price of each job using these rates? 3. Which bids are more accurate? Why?arrow_forwardThe management of Wheeler Company has decided to develop cost formulas for its major overhead activities. Wheeler uses a highly automated manufacturing process, and power costs are a significant manufacturing cost. Cost analysts have decided that power costs are mixed; thus, they must be broken into their fixed and variable elements so that the cost behavior of the power usage activity can be properly described. Machine hours have been selected as the activity driver for power costs. The following data for the past eight quarters have been collected: Required: 1. Prepare a scattergraph by plotting power costs against machine hours. Does the scatter-graph show a linear relationship between machine hours and power cost? 2. Using the high and low points, compute a power cost formula. 3. Use the method of least squares to compute a power cost formula. Evaluate the coefficient of determination. 4. Rerun the regression and drop the point (20,000; 26,000) as an outlier. Compare the results from this regression to those for the regression in Requirement 3. Which is better?arrow_forwardBig Mikes, a large hardware store, has gathered data on its overhead activities and associated costs for the past 10 months. Nizam Sanjay, a member of the controllers department, believes that overhead activities and costs should be classified into groups that have the same driver. He has decided that unloading incoming goods, counting goods, and inspecting goods can be grouped together as a more general receiving activity, since these three activities are all driven by the number of receiving orders. The 10 months of data shown below have been gathered for the receiving activity. Required: 1. Prepare a scattergraph, plotting the receiving costs against the number of purchase orders. Use the vertical axis for costs and the horizontal axis for orders. 2. Select two points that make the best fit, and compute a cost formula for receiving costs. 3. Using the high-low method, prepare a cost formula for the receiving activity. 4. Using the method of least squares, prepare a cost formula for the receiving activity. What is the coefficient of determination?arrow_forward

- The controller of the South Charleston plant of Ravinia, Inc., monitored activities associated with materials handling costs. The high and low levels of resource usage occurred in September and March for three different resources associated with materials handling. The number of moves is the driver. The total costs of the three resources and the activity output, as measured by moves for the two different levels, are presented as follows: Required: 1. Determine the cost behavior formula of each resource. Use the high-low method to assess the fixed and variable components. 2. Using your knowledge of cost behavior, predict the cost of each item for an activity output level of 9,000 moves. 3. Construct a cost formula that can be used to predict the total cost of the three resources combined. Using this formula, predict the total materials handling cost if activity output is 9,000 moves. In general, when can cost formulas be combined to form a single cost formula?arrow_forwardDouglas Davis, controller for Marston, Inc., prepared the following budget for manufacturing costs at two different levels of activity for 20X1: During 20X1, Marston worked a total of 80,000 direct labor hours, used 250,000 machine hours, made 32,000 moves, and performed 120 batch inspections. The following actual costs were incurred: Marston applies overhead using rates based on direct labor hours, machine hours, number of moves, and number of batches. The second level of activity (the right column in the preceding table) is the practical level of activity (the available activity for resources acquired in advance of usage) and is used to compute predetermined overhead pool rates. Required: 1. Prepare a performance report for Marstons manufacturing costs in the current year. 2. Assume that one of the products produced by Marston is budgeted to use 10,000 direct labor hours, 15,000 machine hours, and 500 moves and will be produced in five batches. A total of 10,000 units will be produced during the year. Calculate the budgeted unit manufacturing cost. 3. One of Marstons managers said the following: Budgeting at the activity level makes a lot of sense. It really helps us manage costs better. But the previous budget really needs to provide more detailed information. For example, I know that the moving materials activity involves the use of forklifts and operators, and this information is lost when only the total cost of the activity for various levels of output is reported. We have four forklifts, each capable of providing 10,000 moves per year. We lease these forklifts for five years, at 10,000 per year. Furthermore, for our two shifts, we need up to eight operators if we run all four forklifts. Each operator is paid a salary of 30,000 per year. Also, I know that fuel costs about 0.25 per move. Assuming that these are the only three items, expand the detail of the flexible budget for moving materials to reveal the cost of these three resource items for 20,000 moves and 40,000 moves, respectively. Based on these comments, explain how this additional information can help Marston better manage its costs. (Especially consider how activity-based budgeting may provide useful information for non-value-added activities.)arrow_forwardYoung Company is beginning operations and is considering three alternatives to allocate manufacturing overhead to individual units produced. Young can use a plantwide rate, departmental rates, or activity-based costing. Young will produce many types of products in its single plant, and not all products will be processed through all departments. In which one of the following independent situations would reported net income for the first year be the same regardless of which overhead allocation method had been selected? a. All production costs approach those costs that were budgeted. b. The sales mix does not vary from the mix that was budgeted. c. All manufacturing overhead is a fixed cost. d. All ending inventory balances are zero.arrow_forward

- Flaherty, Inc., has just completed its first year of operations. The unit costs on a normal costing basis are as follows: During the year, the company had the following activity: Actual fixed overhead was 12,000 less than budgeted fixed overhead. Budgeted variable overhead was 5,000 less than the actual variable overhead. The company used an expected actual activity level of 12,000 direct labor hours to compute the predetermined overhead rates. Any overhead variances are closed to Cost of Goods Sold. Required: 1. Compute the unit cost using (a) absorption costing and (b) variable costing. 2. Prepare an absorption-costing income statement. 3. Prepare a variable-costing income statement. 4. Reconcile the difference between the two income statements.arrow_forwardThingOne Company has the following information available for the past year. They use machine hours to allocate overhead. What is the variable overhead efficiency variance?arrow_forwardSilven Company has identified the following overhead activities, costs, and activity drivers for the coming year: Silven produces two models of cell phones with the following expected activity demands: 1. Determine the total overhead assigned to each product using the four activity drivers. 2. Determine the total overhead assigned to each model using the two most expensive activities. The costs of the two relatively inexpensive activities are allocated to the two expensive activities in proportion to their costs. 3. Using ABC as the benchmark, calculate the percentage error and comment on the accuracy of the reduced system. Explain why this approach may be desirable.arrow_forward

- Evans, Inc., has a unit-based costing system. Evanss Miami plant produces 10 different electronic products. The demand for each product is about the same. Although they differ in complexity, each product uses about the same labor time and materials. The plant has used direct labor hours for years to assign overhead to products. To help design engineers understand the assumed cost relationships, the Cost Accounting Department developed the following cost equation. (The equation describes the relationship between total manufacturing costs and direct labor hours; the equation is supported by a coefficient of determination of 60 percent.) Y=5,000,000+30X,whereX=directlaborhours The variable rate of 30 is broken down as follows: Because of competitive pressures, product engineering was given the charge to redesign products to reduce the total cost of manufacturing. Using the above cost relationships, product engineering adopted the strategy of redesigning to reduce direct labor content. As each design was completed, an engineering change order was cut, triggering a series of events such as design approval, vendor selection, bill of materials update, redrawing of schematic, test runs, changes in setup procedures, development of new inspection procedures, and so on. After one year of design changes, the normal volume of direct labor was reduced from 250,000 hours to 200,000 hours, with the same number of products being produced. Although each product differs in its labor content, the redesign efforts reduced the labor content for all products. On average, the labor content per unit of product dropped from 1.25 hours per unit to one hour per unit. Fixed overhead, however, increased from 5,000,000 to 6,600,000 per year. Suppose that a consultant was hired to explain the increase in fixed overhead costs. The consultants study revealed that the 30 per hour rate captured the unit-level variable costs; however, the cost behavior of other activities was quite different. For example, setting up equipment is a step-fixed cost, where each step is 2,000 setup hours, costing 90,000. The study also revealed that the cost of receiving goods is a function of the number of different components. This activity has a variable cost of 2,000 per component type and a fixed cost that follows a step-cost pattern. The step is defined by 20 components with a cost of 50,000 per step. Assume also that the consultant indicated that the design adopted by the engineers increased the demand for setups from 20,000 setup hours to 40,000 setup hours and the number of different components from 100 to 250. The demand for other non-unit-level activities remained unchanged. The consultant also recommended that management take a look at a rejected design for its products. This rejected design increased direct labor content from 250,000 hours to 260,000 hours, decreased the demand for setups from 20,000 hours to 10,000 hours, and decreased the demand for purchasing from 100 component types to 75 component types, while the demand for all other activities remained unchanged. Required: 1. Using normal volume, compute the manufacturing cost per labor hour before the year of design changes. What is the cost per unit of an average product? 2. Using normal volume after the one year of design changes, compute the manufacturing cost per hour. What is the cost per unit of an average product? 3. Before considering the consultants study, what do you think is the most likely explanation for the failure of the design changes to reduce manufacturing costs? Now use the information from the consultants study to explain the increase in the average cost per unit of product. What changes would you suggest to improve Evanss efforts to reduce costs? 4. Explain why the consultant recommended a second look at a rejected design. Provide computational support. What does this tell you about the strategic importance of cost management?arrow_forwardScattergraph, High–Low Method, and Predicting Cost for a Different Time Period from the One Used to Develop a Cost Formula Farnsworth Company has gathered data on its overhead activities and associated costs for the past 10 months. Tracy Heppler, a member of the controller's department, has convinced management that overhead costs can be better estimated and controlled if the fixed and variable components of each overhead activity are known. One such activity is receiving raw materials (unloading incoming goods, counting goods, and inspecting goods), which she believes is driven by the number of receiving orders. Ten months of data have been gathered for the receiving activity and are as follows: Month Receiving Orders Receiving Cost ($) 1 1,000 27,000 2 700 22,500 3 1,500 42,000 4 1,200 25,500 5 1,300 37,500 6 1,100 31,500 7 1,600 43,500 8 1,400 36,000 9 1,700 40,500 10 900 24,000 Required: 1. On your own paper, prepare a scattergraph based on the 10…arrow_forwardThe management of Garn Corporation would like to investigate the possibility of basing its predetermined overhead rate on activity at capacity rather than on the estimated activity for the coming year. The Corporation's controller has provided an example to illustrate how this new system would work. In this example, the allocation base is machine-hours and the estimated activity for the upcoming year is 69,000 machine-hours. Capacity is 85,000 machine-hours. AlIl of the manufacturing overhead is fixed and is $4,105,500 per year within the range of 69,000 to 85,000 machine-hours. If the Corporation bases its predetermined overhead rate on capacity but the actual level of activity for the year turns out to be 69,700 machine-hours, the cost of unused capacity shown on the income statement prepared for internal management purposes would be closest to: Multiple Choice $772,800 $780,640 $738,990 $41,650arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Excel Applications for Accounting Principles

Accounting

ISBN:9781111581565

Author:Gaylord N. Smith

Publisher:Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:9781947172609

Author:OpenStax

Publisher:OpenStax College

Responsibility Accounting| Responsibility Centers and Segments| US CMA Part 1| US CMA course; Master Budget and Responsibility Accounting-Intro to Managerial Accounting- Su. 2013-Prof. Gershberg; Author: Mera Skill; Rutgers Accounting Web;https://www.youtube.com/watch?v=SYQ4u1BP24g;License: Standard YouTube License, CC-BY