Concept explainers

Videos

Accounting for the Use and Disposal of Long-Lived Assets

Nicole’s Getaway Spa (NGS) purchased a hydrotherapy tub system to add to the wellness programs at NGS. The machine was purchased at the beginning of the year at a cost of $7,000. The estimated useful life was five years and the residual value was $500. Assume that the estimated productive life of the machine is 13,000 hours. Expected annual production was year 1, 3,100 hours; year 2, 2,500 hours; year 3, 3,400 hours; year 4, 2,200 hours; and year 5, 1,800 hours.

Required:

- 1. Complete a

depreciation schedule for each of the alternative methods.- a. Straight-line.

- b. Units-of-production.

- c. Double-declining-balance.

- 2. Assume NGS sold the hydrotherapy tub system for $2,100 at the end of year 3. Prepare the

journal entry to account for the disposal of this asset under the three different methods. - 3. The following amounts were

forecast for year 3: Sales Revenues $42,000; Cost of Goods Sold $33,000; Other Operating Expenses $4,000; and Interest Expense $800. Create an income statement for year 3 for each of the different depreciation methods, ending at Income before Income Tax Expense. (Don’t forget to include a loss or gain on disposal for each method.)

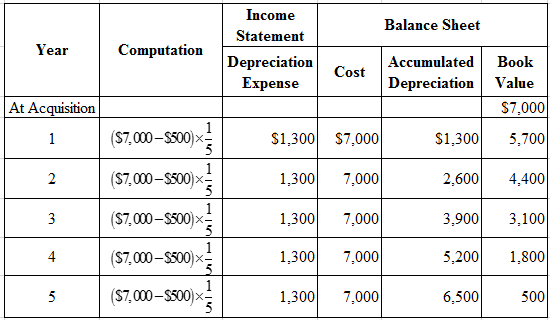

(1) (a)

Prepare the depreciation expense schedule under straight-line method

Explanation of Solution

Straight-line method: The depreciation method which assumes that the consumption of economic benefits of long-term asset could be distributed equally throughout the useful life of the asset is referred to as straight-line method.

Formula for straight-line depreciation method:

Depreciation expense: Depreciation expense is a non-cash expense, which is recorded on the income statement reflecting the consumption of economic benefits of long-term asset.

Accumulated depreciation: The total amount of depreciation expense deducted, from the time asset acquired till date, as reported in the account as on a particular date, is referred to as accumulated depreciation.

Formula for accumulated depreciation:

Book value: The amount of acquisition cost of less accumulated depreciation as on a particular date is referred to as book value.

Formula for book value:

Depreciation schedule under straight-line method:

Figure (1)

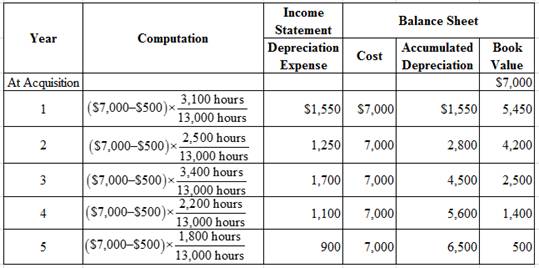

(1) (b)

Prepare the depreciation expense schedule under units-of-production

Explanation of Solution

Units-of-production method: The depreciation method which assumes that the consumption of economic benefits of long-term asset is based on the production capacity or output is referred to as units-of-production method.

Formula for units-of-production depreciation method:

Depreciation schedule under units-of-production method:

Figure (2)

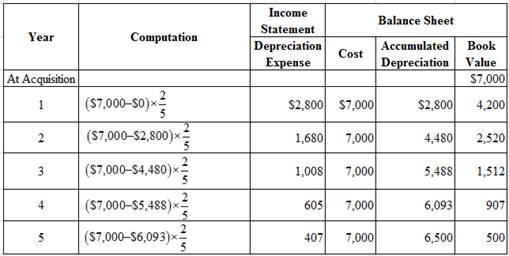

(1) (c)

Prepare the depreciation expense schedule under double-declining-balance method

Explanation of Solution

Double-declining-balance method: The depreciation method which assumes that the consumption of economic benefits of long-term asset is high in the early years but gradually declines towards the end of its useful life, is referred to as double-declining-balance method.

Formula for double-declining-balance depreciation method:

Depreciation schedule under double-declining-balance method:

Figure (3)

Note:

Compute depreciation expense in Year 5.

(2)

Prepare the journal entries for the sale of equipment under three methods

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Prepare journal entry for the sale of building, under straight-line method.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| Cash | 2,100 | |||||

| Accumulated Depreciation | 3,900 | |||||

| Loss on Disposal | 1,000 | |||||

| Equipment | 7,000 | |||||

| (To record sale of equipment) | ||||||

Table (1)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Accumulated Depreciation–Building is a contra-asset account. Since the building is sold, the accumulated depreciation balance is reversed to reduce the balance in the account; hence, the account is debited.

- Loss on Disposal is an expense account. Since losses and expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Building is an asset account. Since building is sold, asset account decreased, and a decrease in asset is credited.

Working Notes:

Determine the gain on sale.

Step 1: Compute book value on the date of sale.

Step 2: Compute gain (loss) on sale.

Prepare journal entry for the sale of building, under units-of-production method.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| Cash | 2,100 | |||||

| Accumulated Depreciation | 4,500 | |||||

| Loss on Disposal | 400 | |||||

| Equipment | 7,000 | |||||

| (To record sale of equipment) | ||||||

Table (2)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Accumulated Depreciation–Building is a contra-asset account. Since the building is sold, the accumulated depreciation balance is reversed to reduce the balance in the account; hence, the account is debited.

- Loss on Disposal is an expense account. Since losses and expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Building is an asset account. Since building is sold, asset account decreased, and a decrease in asset is credited.

Working Notes:

Determine the gain on sale.

Step 1: Compute book value on the date of sale.

Step 2: Compute gain (loss) on sale.

Prepare journal entry for the sale of equipment, under double-declining-balance method.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| Cash | 2,100 | |||||

| Accumulated Depreciation | 5,488 | |||||

| Equipment | 7,000 | |||||

| Gain on Disposal | 588 | |||||

| (To record sale of truck) | ||||||

Table (3)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Accumulated Depreciation–Equipment is a contra-asset account. Since the equipment is sold, the accumulated depreciation balance is reversed to reduce the balance in the account; hence, the account is debited.

- Equipment is an asset account. Since equipment is sold, asset account decreased, and a decrease in asset is credited.

- Gain on Disposal is a revenue account. Since gains and revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Determine the gain on sale.

Step 1: Compute book value on the date of sale.

Step 2: Compute gain (loss) on sale.

(3)

Prepare the income statement of NG Spa for the Year 3, under three depreciation methods

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare income statement for NG Spa for the Year 3.

| NG Spa | |||

| Income Statement | |||

| For Year 3 | |||

| Particulars | Straight-Line | Units-of-Production | Double-Declining-Balance |

| Sales revenue | $42,000 | $42,000 | $42,000 |

| Cost of goods sold | 33,000 | 33,000 | 33,000 |

| Gross profit | 9,000 | 9,000 | 9,000 |

| Operating expenses: | |||

| Depreciation expense | $1,300 | $1,700 | $1,008 |

| Other operating expenses | 4,000 | 4,000 | 4,000 |

| Loss (Gain) on disposal | 1,000 | 400 | (588) |

| Total operating expenses | 6,300 | 6,100 | 4,420 |

| Income from operations | 2,700 | 2,900 | 4,580 |

| Interest expense | 800 | 800 | 800 |

| Income before income tax expense | $1,900 | $2,100 | $3,780 |

Table (4)

Want to see more full solutions like this?

Chapter 9 Solutions

Fundamentals Of Financial Accounting

- IMPACT OF IMPROVEMENTS AND REPLACEMENTS ON THE CALCULATION OF DEPRECIATION On January 1, 20-1, two flight simulators were purchased by a space camp for 77,000 each with a salvage value of 5,000 each and estimated useful lives of eight years. On January 1, 20-2, the hydraulic system for Simulator A was replaced for 6,000 cash and an updated computer for more advanced students was installed in Simulator B for 9,000 cash. The hydraulic system is expected to extend the life of Simulator A three years beyond the original estimate. REQUIRED 1. Using the straight-line method, prepare general journal entries for depreciation on December 31, 20-1, for Simulators A and B. 2. Enter the transactions for January 20-2 in a general journal. 3. Assuming no other additions, improvements, or replacements, calculate the depreciation expense for each simulator for 20-2 through 20-8.arrow_forwardDuring the current year, Arkells Inc. made the following expenditures relating to plant machinery. Renovated five machines for $100,000 to improve efficiency in production of their remaining useful life of five years Low-cost repairs throughout the year totaled $70,000 Replaced a broken gear on a machine for $10,000 A. What amount should be expensed during the period? B. What amount should be capitalized during the period?arrow_forwardapplies to the questions displayed below.] Nicole's Getaway Spa (NGS) purchased a hydrotherapy tub system to add to the wellness programs at NGS. The machine was purchased at the beginning of the year at a cost of $15,500. The estimated useful life was five years and the residual value was $1,500. Assume that the estimated productive life of the machine is 10,000 hours. Expected annual production was year 1, 2,350 hours; year 2, 2,500 hours; year 3, 2,050 hours; year 4, 2,100 hours; and year 5, 1,000 hours. 3. Assume NGS sold the hydrotherapy tub system for $4,650 at the end of year 3. The following amounts were forecast for year 3: Sales Revenues $52,000; Cost of Goods Sold $41,000; Other Operating Expenses $4,500; and Interest Expense $700. Create an income statement for year 3 for each of the different depreciation methods, ending at Income before Income Tax Expense. (Don't forget to include a loss or gain on disposal for each method.). (Do not round intermediate calculations. Round…arrow_forward

- Required information [The following information applies to the questions displayed below. Nicole's Getaway Spa (NGS) purchased a hydrotherapy tub system to add to the wellness programs at NGS. The machine was purchased at the beginning of the year at a cost of $8,500. The estimated useful life was five years and the residual value was $500. Assume that the estimated productive life of the machine is 10,000 hours. Expected annual production was year 1, 2,250 hours: year 2, 2,350 hours; year 3, 2,300 hours: year 4, 2.100 hours; and year 5, 1,000 hours. Required: 1. Complete a depreciation schedule for each of the alternative methods. a. Straight-line. b. Units-of-production.. c. Double-declining-balance.arrow_forwardRequired information [The following information applies to the questions displayed below.] Nicole's Getaway Spa (NGS) purchased a hydrotherapy tub system to add to the wellness programs at NGS. The machine was purchased at the beginning of the year at a cost of $8,500. The estimated useful life was five years and the residual value was $500. Assume that the estimated productive life of the machine is 10,000 hours. Expected annual production was year 1, 2,250 hours, year 2, 2,350 hours: year 3, 2,300 hours; year 4. 2.100 hours; and year 5, 1,000 hours. Required: 1. Complete a depreciation schedule for each of the alternative methods. a. Straight-line. b. Units-of-production. c. Double-declining-balance Complete this question by entering your answers in the tabs below. Req 1A Req 1C Complete a depreciation schedule for straight-line method. (Do not round intermediate calculations. Round your final answers to the nearest dollar amount.) Req 18 Year At Acquisition Year 1 Year 2 Year 3 Year…arrow_forwardUniversity Car Wash purchased new soap dispensing equipment that cost $249,000 including installation. The company estimates that the equipment will have a residual value of $25,500. University Car Wash also estimates it will use the machine for six years or about 12,500 total hours. Actual use per year was as follows: Year 1 2 3 4 5 6 Total Year 1 2 3 4 5 6 Problem 7-5A (Algo) Part 3 3. Prepare a depreciation schedule for six years using the activity-based method. (Round your "Depreciation Rate" to 2 decimal places and use this amount in all subsequent calculations.) Hours Used 2,900 1,800 1,900 2,100 1,900 1,900 $ UNIVERSITY CAR WASH Depreciation Schedule-Activity-Based End of Year Amounts Depreciation Expense 0 Accumulated Depreciation Book Valuearrow_forward

- Clean Air Company makes and sells cloth masks. The company purchased a new automated sewing machine at the beginning of Year 1 for $87,000. The machine is expected to have a two-year useful life and a $21,700 salvage value. The expected mask production is estimated at 130,600 masks. Actual mask production for the two years was as follows: Year 1 Year 2 Total Required: 72,000 65,000 137,000 Compute the depreciation expense for each of the two years, using units-of-production depreciation. Year 1 Year 2 Depreciation expense Charrow_forwardA high-precision programmable router for shaping furniture components is purchased by Henredon for $190,000. It is expected to last 12 years. Calculate the depreciation deduction and book value for each year using MACRS-GDS allowances. a. What is the MACRS-GDS property class? b. Assume the complete allowable depreciation schedule is used. c. Assume the asset is sold during the 5th year of use.arrow_forwardUniversity Car Wash purchased new soap dispensing equipment that cost $234,000 including installation. The company estimates that the equipment will have a residual value of $27,000. University Car Wash also estimates it will use the machine for six years or about 12,000 total hours. Actual use per year was as follows: Year Hours Used 1 2,800 2 1,900 3 2,000 4 2,000 5 1,800 6 1,500 3. Prepare a depreciation schedule for six years using the activity-based method. (Round your "Depreciation Rate" to 2 decimal places and use this amount in all subsequent calculations.)arrow_forward

- A high-precision programmable router for shaping office furniture components (office furniture manufacturing equipment) is purchased by Henredon for $350,000. It is expected to last 12 years. Calculate the depreciation deduction and book value for each year using MACRS-GDS allowances. a. What is the MACRS-GDS property class? Provide your answer in year (format example: 3 year) Calculate the depreciation deduction using MACRS- GDS allowances for year 5 = $. (Please provide your response to the nearest integer with no comma or $ sign.) Calculate the book value using MACRS-GDS allowances for year 5 = $. (Please provide your response to the nearest integer with no comma or $ sign.) Assume the asset is sold during the 5th year of use. Calculate the depreciation deduction using MACRS-GDS allowances for year 5 = $. (Please provide your response to the nearest integer with no comma or $ sign.)arrow_forwardcommunity hospital in a rual community operates the ambulance service. the hospital purchases a new ambulance for $150,000. they estimate a useful life of 10 years and a salvage value of $20,000. what is the annual charge for depreciation on this asset?arrow_forwardA granary purchases a conveyor used in the manufacture of grain for transporting, filling, or emptying. It is purchased and installed for $72,000 with a market value for salvage purposes that decreases at a rate of 20% per year with a minimum of value $2,350. Operation and maintenance is expected to cost $14,400 in the first year, increasing $1,200 per year thereafter. The granary uses a MARR of 15%. What is the optimum replacement interval for the conveyor? ___________ years.arrow_forward

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT