Videos

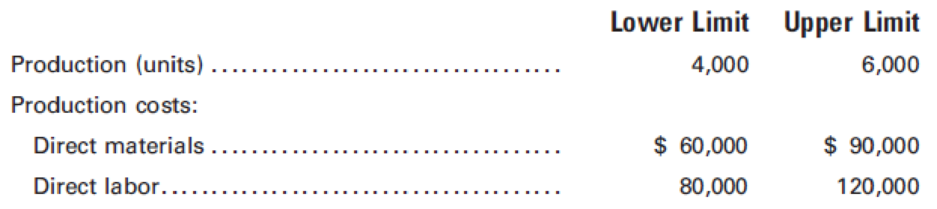

Grand Canyon Manufacturing Inc. produces and sells a product with a price of $100 per unit. The following cost data have been prepared for its estimated upper and lower limits of activity:

Overhead:

Selling and administrative expenses:

Required:

- 1. Classify each cost element as either variable, fixed, or semi-variable. (Hint: Recall that variable expenses must go up in direct proportion to changes in the volume of activity.)

- 2. Calculate the break-even point in units and dollars. (Hint: First use the high-low method illustrated in Chapter 4 to separate costs into their fixed and variable components.)

- 3. Prepare a break-even chart.

- 4. Prepare a contribution income statement, similar in format to the statement appearing on page 540, assuming sales of 5,000 units.

- 5. Recompute the break-even point in units, assuming that variable costs increase by 20% and fixed costs are reduced by $50,000.

1.

Classify the each cost element as either variable, fixed or semi-variable.

Explanation of Solution

Classify the each cost element as either variable, fixed or semi-variable as follows:

- Variable costs vary with the number of units produced or for the services provided. For example, the labor costs increase if the number of labor hours is increased, and the labor costs decrease if the number of labor hours is decreased. Direct material, direct labor and indirect material are considered as the variable costs.

- Fixed Cost is a cost which is constant in the short run, it is not related to any change in the production of goods or service, it will be fixed disregarding of increase or decrease in output. Fixed cost is generally incurred on fixed assets in long run. Depreciation, office salary and advertising are considered as the fixed cost.

- Semi variable costs are the cost that changes based on the changes in the production, but it is not proportionately. Indirect labor, sales salaries and other expense are considered as semi-variable cost.

2.

Calcualte the break even point in units and dollars.

Explanation of Solution

Calcualte the break even point in units and dollars as follows:

Working note (1):

Calcualte the vairable cost per unit:

Working note (2):

Calculate the variable cost for 4,000 units.

Working note (3):

Calcualte the fixed cost:

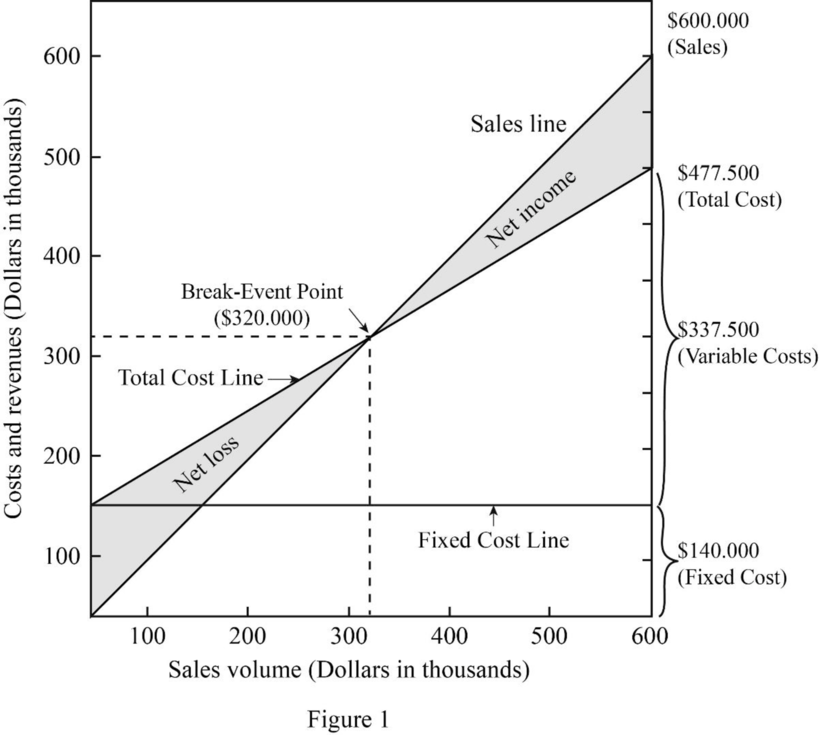

3.

Prepare a break-even chart.

Explanation of Solution

Prepare a break-even chart as follows:

4.

Prepare a contribution income statement of company G.

Explanation of Solution

Prepare a contribution income statement of company G as follows:

| Company G | |

| Income statement | |

| For the year ended --- | |

| Particulars | Amount ($) |

| Sales | $ 500,000 |

| Less: Variable cost | $281,250 |

| Contribution margin | $218,250 |

| Less: Fixed costs (3) | $140,000 |

| Net operating income | $ 78,750 |

Table (1)

5.

Calculate the break-even point in units, assume that the variable costs is increased by 20% and fixed cost is decreased by $50,000.

Explanation of Solution

Calculate the break-even point in units, assume that the variable costs is increased by 20% and fixed cost is decreased by $50,000 as follows:

Working note (4):

Calcualte the decrase in fixed cost:

Working note (5):

Calcualte the increase in variable cost:

Want to see more full solutions like this?

Chapter 10 Solutions

Principles of Cost Accounting

Additional Business Textbook Solutions

INTERMEDIATE ACCOUNTING

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Cost Accounting (15th Edition)

Managerial Accounting: Tools for Business Decision Making

Intermediate Accounting

Introduction To Managerial Accounting

- The management of Hartman Company is trying to determine the amount of each of two products to produce over the coming planning period. The following information concerns labor availability, labor utilization, and product profitability: a. Develop a linear programming model of the Hartman Company problem. Solve the model to determine the optimal production quantities of products 1 and 2. b. In computing the profit contribution per unit, management does not deduct labor costs because they are considered fixed for the upcoming planning period. However, suppose that overtime can be scheduled in some of the departments. Which departments would you recommend scheduling for overtime? How much would you be willing to pay per hour of overtime in each department? c. Suppose that 10, 6, and 8 hours of overtime may be scheduled in departments A, B, and C, respectively. The cost per hour of overtime is 18 in department A, 22.50 in department B, and 12 in department C. Formulate a linear programming model that can be used to determine the optimal production quantities if overtime is made available. What are the optimal production quantities, and what is the revised total contribution to profit? How much overtime do you recommend using in each department? What is the increase in the total contribution to profit if overtime is used?arrow_forwardLillibridge & Friends, Incorporated provides you with the following data for its single product: Sales price per unit Fixed costs (per quarter): Selling, general, and administrative (SG&A) Manufacturing overhead Variable costs (per unit): Direct labor Direct materials Manufacturing overhead SG&A Number of units produced per quarter a. Prime cost per unit b. Contribution margin per unit c. Gross margin per unit d. Conversion cost per unit e. Variable cost per unit f. Full absorption cost per unit g. Variable production cost per unit h. Full cost per unit Required: Compute the amounts for each of the following assuming that the production levels are within the relevant range if the number of units is 500,000 per quarter. Also calculate if the number of units increases to 600,000 per quarter. Note: Do not round intermediate calculations. Round your answers to 2 decimal places. $ $ $ 160 1,500,000 4,500,000 500,000 units 600,000 units 41.00 $ 41.00 83.00 $ $ $ $ 19 22 20 16 500,000 units…arrow_forwardLillibridge & Friends, Incorporated provides you with the following data for its single product: Sales price per unit Fixed costs (per quarter): Selling, general, and administrative (SG&A) Manufacturing overhead Variable costs (per unit): Direct labor Direct materials Manufacturing overhead SG&A Number of units produced per quarter a. Prime cost per unit b. Contribution margin per unit c. Gross margin per unit d. Conversion cost per unit e. Variable cost per unit f. Full absorption cost per unit Required: Compute the amounts for each of the following assuming that the production levels are within the relevant range if the number of units is 500,000 per quarter. Also calculate if the number of units increases to 600,000 per quarter. Note: Round your answers to 2 decimal places. g. Variable production cost per unit h. Full cost per unit 500,000 units $ $ S $ 50 1,500,000 4,500,000 600,000 units $ 19.00 17.00 $ 13.00 $ 8 11 9 5 500,000 units 19.00 17.00 14.50arrow_forward

- Lillibridge & Friends, Incorporated provides you with the following data for its single product: Sales price per unit Fixed costs (per quarter): Selling, general, and administrative (SG&A) Manufacturing overhead Variable costs (per unit): Direct labor Direct materials Manufacturing overhead SG&A Number of units produced per quarter a. Prime cost per unit b. Contribution margin per unit c. Gross margin per unit d. Conversion cost per unit e. Variable cost per unit f. Full absorption cost per unit g. Variable production cost per unit h. Full cost per unit 500,000 units $50 1,500,000 4,500,000 Required: Compute the amounts for each of the following assuming that the production levels are within the relevant range if the number of units is 500,000 per quarter. Also calculate if the number of units increases to 600,000 per quarter. Note: Round your answers to 2 decimal places. 8 600,000 units 11 9 5 500,000 unitsarrow_forwardThe cost per unit associated with the production of Xen Merchandising are the following: Direct Materials - P1,000; Direct Wages - P200; Variable Overhead - P1,500; and Fixed Overhead - P2,000. Given the data, what is the product cost?arrow_forwardTashiro Inc. has decided to use the high-low method to estimate the total cost and the fixed and variable cost components of the total cost. The data for various levels of production are as follows: Units Produced Total Costs 2,210 $196,560 910 126,360 1,370 167,920 a. Determine the variable cost per unit and the total fixed cost. Variable cost (Round to two decimal places.) $fill in the blank 1 per unit Total fixed cost $fill in the blank 2 b. Based on part (a), estimate the total cost for 1,120 units of production. Total cost for 1,120 units: $fill in the blank 3arrow_forward

- The graphs below represent cost behavior patterns that might occur in a company’s cost structure. The vertical axis represents total cost, and the horizontal axis represents activity output Required:For each of the following situations, choose the graph from the group a–1 that best illustrates the cost pattern involved. Also, for each situation, identify the driver that measures activity output.1. The cost of power when a fixed fee of $500 per month is charged plus an additional charge of $0.12 per kilowatt-hour used.2. Commissions paid to sales representatives. Commissions are paid at the rate of 5 percent of sales made up to total annual sales of $500,000, and 7 percent of sales above $500,000.3. A part purchased from an outside supplier costs $12 per part for the first 3,000 parts and $10 per part for all parts purchased in excess of 3,000 units.4. The cost of surgical gloves, which are purchased in increments of 100 units (gloves come in boxes of 100 pairs).5. The cost of tuition…arrow_forwardThe Gangwere Company has assembled the following data pertaining to certain costs that cannot be easily identified as either fixed or variable. Gangwere Company has heard about a method of measuring cost functions called the high-low method and has decided to use it in this situation. Month Cost Hours January $44,900 3,500 February 24,400 2,000 March 31,280 2,450 April 36,400 3,000 May 44,160 3,900 June 42,400 3,740How is the cost function stated? Question 12 options: a) y = $3,600 + $10.40X b) y = $10,112 + $8.64X c) y = $26,672 + $1.84X d) y = $21,360 + $10.40arrow_forwardThe Mortise Company has assembled the following data pertaining to certain costs that cannot be easily identified as either fixed or variable. Mortise has heard about a method of measuring cost functions called the high-low method and has decided to use it in this situation. Month Cost Hours January $40,000 3,600 February 38,500 3,000 March 36,280 3,300 April 38,000 3,500 May 69,850 5,850 June 45,000 4,250 a. What is the slope coefficient? b. What is the constant for the estimated cost equation? c. What is the estimated cost function for the above data? d. What is the estimated total cost at an operating level of 3,100 hours?arrow_forward

- [The following information applies to the questions displayed below.] Preble Company manufactures one product. Its variable manufacturing overhead is applied to production based on direct labor-hours and its standard cost card per unit is as follows: Direct material: 5 pounds at $8.00 per pound Direct labor: 3 hours at $15 per hour Variable overhead: 3 hours at $9 per hour Total standard variable cost per unit The company also established the following cost formulas for its selling expenses: Variable Cost per Unit Sold Advertising Sales salaries and commissions Shipping expenses Fixed Cost per Month $ 350,000 $ 400,000 $ 40.00 45.00 27.00 $112.00 The planning budget for March was based on producing and selling 21,000 units. However, during March the company actually produced and sold 26,000 units and incurred the following costs: Direct labor cost $ 27.00 $18.00 a. Purchased 160,000 pounds of raw materials at a cost of $6.50 per pound. All of this material was used in production. b.…arrow_forward[The following information applies to the questions displayed below.] Preble Company manufactures one product. Its variable manufacturing overhead is applied to production based on direct labor-hours and its standard cost card per unit is as follows: Direct material: 5 pounds at $8.00 per pound Direct labor: 3 hours at $15 per hour Variable overhead: 3 hours at $9 per hour Total standard variable cost per unit The company also established the following cost formulas for its selling expenses: Variable Cost per Unit Sold Advertising Sales salaries and commissions Shipping expenses $ 40.00 45.00 27.00 $112.00 Fixed Cost per Month $ 350,000 $ 400,000 The planning budget for March was based on producing and selling 21,000 units. However, during March the company actually produced and sold 26,000 units and incurred the following costs: $ 27.00 $18.00 a. Purchased 160,000 pounds of raw materials at a cost of $6.50 per pound. All of this material was used in production. b. Direct-laborers…arrow_forward[The following information applies to the questions displayed below.] Preble Company manufactures one product. Its variable manufacturing overhead is applied to production based on direct labor-hours and its standard cost card per unit is as follows: Direct material: 5 pounds at $8.00 per pound Direct labor: 3 hours at $15 per hour Variable overhead: 3 hours at $9 per hour Total standard variable cost per unit The company also established the following cost formulas for its selling expenses: Variable Cost per Unit Sold Advertising Sales salaries and commissions Shipping expenses $ 40.00 45.00 27.00 $112.00 Fixed Cost per Month $ 350,000 $ 400,000 $ 27.00 $18.00 The planning budget for March was based on producing and selling 21,000 units. However, during March the company actually produced and sold 26,000 units and incurred the following costs:arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning