Concept explainers

Videos

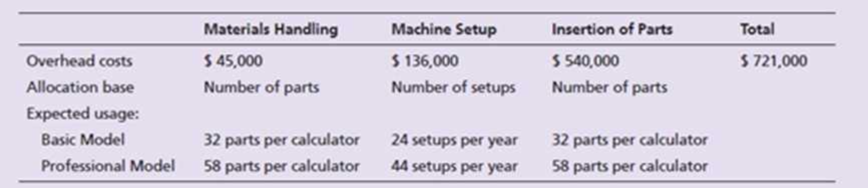

Koehler (see Exercise E19-15 and Exercise E19-16) makes handheld calculators in two models—basic and professional—and wants to further refine its costing system by allocating

Requirement 1

Koehler expects to produce 200,000 basic models and 200,000 professional models. Compute the predetermined overhead allocation rates using activity-based costing. How much overhead is allocated to the basic model? To the professional model?

Requirement 2

Compare your answers for Exercise E19-15, Exercise E19-16, and Exercise E19-17. What conclusions can you draw?

Want to see the full answer?

Check out a sample textbook solution

Chapter 19 Solutions

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Additional Business Textbook Solutions

INTERMEDIATE ACCOUNTING

Construction Accounting And Financial Management (4th Edition)

Principles Of Taxation For Business And Investment Planning 2020 Edition

Financial Accounting

Principles of Accounting Volume 2

PRINCIPLES OF TAXATION F/BUS.+INVEST.

- Evans, Inc., has a unit-based costing system. Evanss Miami plant produces 10 different electronic products. The demand for each product is about the same. Although they differ in complexity, each product uses about the same labor time and materials. The plant has used direct labor hours for years to assign overhead to products. To help design engineers understand the assumed cost relationships, the Cost Accounting Department developed the following cost equation. (The equation describes the relationship between total manufacturing costs and direct labor hours; the equation is supported by a coefficient of determination of 60 percent.) Y=5,000,000+30X,whereX=directlaborhours The variable rate of 30 is broken down as follows: Because of competitive pressures, product engineering was given the charge to redesign products to reduce the total cost of manufacturing. Using the above cost relationships, product engineering adopted the strategy of redesigning to reduce direct labor content. As each design was completed, an engineering change order was cut, triggering a series of events such as design approval, vendor selection, bill of materials update, redrawing of schematic, test runs, changes in setup procedures, development of new inspection procedures, and so on. After one year of design changes, the normal volume of direct labor was reduced from 250,000 hours to 200,000 hours, with the same number of products being produced. Although each product differs in its labor content, the redesign efforts reduced the labor content for all products. On average, the labor content per unit of product dropped from 1.25 hours per unit to one hour per unit. Fixed overhead, however, increased from 5,000,000 to 6,600,000 per year. Suppose that a consultant was hired to explain the increase in fixed overhead costs. The consultants study revealed that the 30 per hour rate captured the unit-level variable costs; however, the cost behavior of other activities was quite different. For example, setting up equipment is a step-fixed cost, where each step is 2,000 setup hours, costing 90,000. The study also revealed that the cost of receiving goods is a function of the number of different components. This activity has a variable cost of 2,000 per component type and a fixed cost that follows a step-cost pattern. The step is defined by 20 components with a cost of 50,000 per step. Assume also that the consultant indicated that the design adopted by the engineers increased the demand for setups from 20,000 setup hours to 40,000 setup hours and the number of different components from 100 to 250. The demand for other non-unit-level activities remained unchanged. The consultant also recommended that management take a look at a rejected design for its products. This rejected design increased direct labor content from 250,000 hours to 260,000 hours, decreased the demand for setups from 20,000 hours to 10,000 hours, and decreased the demand for purchasing from 100 component types to 75 component types, while the demand for all other activities remained unchanged. Required: 1. Using normal volume, compute the manufacturing cost per labor hour before the year of design changes. What is the cost per unit of an average product? 2. Using normal volume after the one year of design changes, compute the manufacturing cost per hour. What is the cost per unit of an average product? 3. Before considering the consultants study, what do you think is the most likely explanation for the failure of the design changes to reduce manufacturing costs? Now use the information from the consultants study to explain the increase in the average cost per unit of product. What changes would you suggest to improve Evanss efforts to reduce costs? 4. Explain why the consultant recommended a second look at a rejected design. Provide computational support. What does this tell you about the strategic importance of cost management?arrow_forwardSilven Company has identified the following overhead activities, costs, and activity drivers for the coming year: Silven produces two models of cell phones with the following expected activity demands: 1. Determine the total overhead assigned to each product using the four activity drivers. 2. Determine the total overhead assigned to each model using the two most expensive activities. The costs of the two relatively inexpensive activities are allocated to the two expensive activities in proportion to their costs. 3. Using ABC as the benchmark, calculate the percentage error and comment on the accuracy of the reduced system. Explain why this approach may be desirable.arrow_forwardPlata Company has identified the following overhead activities, costs, and activity drivers for the coming year: Plata produces two models of microwave ovens with the following activity demands: The companys normal activity is 21,000 machine hours. Calculate the total overhead cost that would be assigned to Model X using an activity-based costing system: a. 230,000 b. 240,000 c. 280,000 d. 190,000arrow_forward

- Bienestar Inc., has the following departmental structure for producing a well-known multivitamin: A consultant designed the following cellular manufacturing structure for the same product: The times above the processes represent the time required to process one unit of product. Required: 1. Calculate the time required to produce a batch of 15 bottles using a batch-processing departmental structure. 2. Calculate the time to process 15 units using cellular manufacturing. 3. How much manufacturing time will the cellular manufacturing structure save for a batch of 15 units?arrow_forwardFirenza Company manufactures specialty tools to customer order. Budgeted overhead for the coming year is: Previously, Sanjay Bhatt, Firenza Companys controller, had applied overhead on the basis of machine hours. Expected machine hours for the coming year are 50,000. Sanjay has been reading about activity-based costing, and he wonders whether or not it might offer some advantages to his company. He decided that appropriate drivers for overhead activities are purchase orders for purchasing, number of setups for setup cost, engineering hours for engineering cost, and machine hours for other. Budgeted amounts for these drivers are 5,000 purchase orders, 500 setups, and 2,500 engineering hours. Sanjay has been asked to prepare bids for two jobs with the following information: The typical bid price includes a 40 percent markup over full manufacturing cost. Required: 1. Calculate a plantwide rate for Firenza Company based on machine hours. What is the bid price of each job using this rate? 2. Calculate activity rates for the four overhead activities. What is the bid price of each job using these rates? 3. Which bids are more accurate? Why?arrow_forwardThe management of Wheeler Company has decided to develop cost formulas for its major overhead activities. Wheeler uses a highly automated manufacturing process, and power costs are a significant manufacturing cost. Cost analysts have decided that power costs are mixed; thus, they must be broken into their fixed and variable elements so that the cost behavior of the power usage activity can be properly described. Machine hours have been selected as the activity driver for power costs. The following data for the past eight quarters have been collected: Required: 1. Prepare a scattergraph by plotting power costs against machine hours. Does the scatter-graph show a linear relationship between machine hours and power cost? 2. Using the high and low points, compute a power cost formula. 3. Use the method of least squares to compute a power cost formula. Evaluate the coefficient of determination. 4. Rerun the regression and drop the point (20,000; 26,000) as an outlier. Compare the results from this regression to those for the regression in Requirement 3. Which is better?arrow_forward

- Compute It uses activity-based costing. Two of Compute It's production activities are kitting (assembling the raw materials needed for each computer in one kit) and boxing the completed products for shipment to customers. Assume that Compute It spends $960,000 per month on kitting and $32,000 per month on boxing. Compute It allocates the following: • Kitting costs based on the number of parts used in the computer • Boxing costs based on the cubic feet of space the computer requires Suppose Compute It estimates it will use 400,000 parts per month and ship products with a total volume of 6,400 cubic feet per month. Assume that each desktop computer requires 125 parts and has a volume of 2 cubic feet. The predetermined overhead allocation rate for kitting is $2.40 per part and the predetermined overhead allocation rate for boxing is $5.00 per cubic foot. What are the kitting and boxing costs assigned to one desktop computer? (Round all calculations to the nearest cent.) O A. O B. O C. O…arrow_forwardCompute It uses activity-based costing. Two of Compute It's production activities are kitting (assembling the raw materials needed for each computer in one kit) and boxing the completed products for shipment to customers. Assume that Compute It spends $960,000 per month on kitting and $32,000 per month on boxing. Compute It allocates the following: • Kitting costs based on the number of parts used in the computer • Boxing costs based on the cubic feet of space the computer requires Suppose Compute It estimates it will use 400,000 parts per month and ship products with a total volume of 6,400 cubic feet per month. Assume that each desktop computer requires 125 parts and has a volume of 2 cubic feet. The predetermined overhead allocation rate for kitting is $2.40 per part and the predetermined overhead allocation rate for boxing is $5.00 per cubic foot. What are the kitting and boxing costs assigned to one desktop computer? (Round all calculations to the nearest cent.) O A. O B. O C. O…arrow_forwardRooney Manufacturing produces two keyboards, one for laptop computers and the other for desktop computers. The production process is automated, and the company has found activity-based costing useful in assigning overhead costs to its products. The company has identified five major activities involved in producing the keyboards. Activity Materials receiving & handling Production setup Assembly Quality inspection Packing and shipping Activity measures for the two kinds of keyboards follow: Laptops Desktops Required Labor Cost $ 1,190 1,080 Laptop keyboards Desktop keyboards Allocation Base Cost of material Number of setups Number of parts Inspection time Number of orders Material Number of Number of Cost $6,000 7,000 Cost Per Unit Setups 26 13 Parts 46 25 Allocation Rate 1% of material cost $ 109.00 per setup $ 5.00 per part $ 1.30 per minute $10.00 per order Inspection Time 7,200 minutes 5,100 minutes Number of Orders 61 a. Compute the cost per unit of laptop and desktop keyboards,…arrow_forward

- Keyboard uses activity-based costing. Two of Keyboard's production activities are kitting (assembling the raw materials needed for each computer in one kit) and boxing the completed products for shipment to customers. Assume that Keyboard spends $10,000,000per month on kitting and $18,000,000 per month on boxing.Keyboardallocates the following: •Kitting costs based on the number of parts used in the computer •Boxing costs based on the cubic feet of space the computer requires Suppose Keyboard estimates it will use 250,000,000 parts per month and ship products with a total volume of 22,500,000 cubic feet per month. Assume that each desktop computer requires 175 parts and has a volume of 7 cubic feet. The predetermined overhead allocation rate for kitting is $0.04 per part and the predetermined overhead allocation rate for boxing is $0.80 per cubic foot. What are the kitting and boxing costs assigned to one desktop computer?arrow_forwardRundle Manufacturing produces two keyboards, one for laptop computers and the other for desktop computers. The production process is automated, and the company has found activity-based costing useful in assigning overhead costs to its products. The company has identified five major activities involved in producing the keyboards. Activity Materials receiving & handling Production setup Assembly Quality inspection Packing and shipping Activity measures for the two kinds of keyboards follow: Laptops Desktops Required Labor Cost $ 1,310 1,200 Laptop keyboards Desktop keyboards Allocation Base Cost of material Number of setups Number of parts Inspection time Number of orders Material Number of Number of Cost $ 6,300 7,600 Cost Per Unit Setups 29 13 Parts 49 26 Allocation Rate 3% of material cost $102.00 per setup $3.00 per part $ 1.60 per minute $9.00 per order Inspection Time 7,400 minutes 4,800 minutes a. Compute the cost per unit of laptop and desktop keyboards, assuming that Rundle made…arrow_forwardHorgen Corporation manufactures two products: Product M68B and Product H27T. The company is considering implementing an activity-based costing (ABC) system that allocates its manufacturing overhead to four cost pools. The following additional information is available for the company as a whole and for Products M68B and H27T. Activity Cost Pool Activity Measure Total Cost Total Activity Machining Machine-hours $ 299,000 13,000 MHs Machine setups Number of setups $ 240,000 400 setups Product design Number of products $ 80,000 2 products Order size Direct labor-hours $ 290,000 10,000 DLHs Activity Measure Product M68B Product H27T Machine-hours 6,000 7,000 Number of setups 250 150 Number of products 1 1 Direct labor-hours 4,000 6,000 Using the ABC system, how much total manufacturing overhead cost would be assigned to Product H27T?arrow_forward

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning