Concept explainers

Videos

Requirement – 1

To analyze: The given transaction, and explain their effect on the

Requirement – 1

Explanation of Solution

Accounting equation is an accounting tool expressed in the form of equation, by creating a relationship between the resources or assets of a company, and claims on the resources by the creditors and the owners. Accounting equation is expressed as shown below:

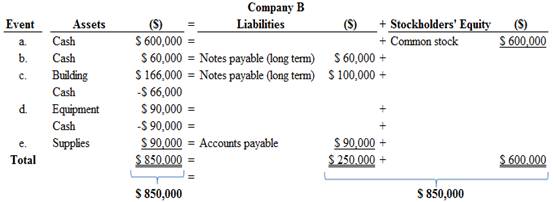

Accounting equation for each transaction is as follows:

Figure (1)

Figure (1)

Therefore, the total assets are equal to the liabilities and stockholder’s equity.

Requirement – 2

To record: The

Requirement – 2

Explanation of Solution

Journal:

Journal is the method of recording monetary business transactions in chronological order. It records the debit and credit aspects of each transaction to abide by the double-entry system.

Rules of Debit and Credit:

Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

- Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, expenses.

Journal entries of Company B are as follows:

a. Issuance of common stock:

| Date | Accounts title and explanation | Ref. | Debit ($) | Credit ($) |

| Cash (+A) | 600,000 | |||

| Common stock (+SE) | 600,000 | |||

| (To record the issuance of common stock) |

Table (1)

- Cash is an assets account and it increased the value of asset by $600,000. Hence, debit the cash account for $600,000.

- Common stock is a component of stockholder’s equity and it increased the value of stockholder’s equity by $600,000, Hence, credit the common stock for $600,000.

b. Cash borrowed from bank (long term)

| Date | Accounts title and explanation | Ref. | Debit ($) | Credit ($) |

| Cash (+A) | 60,000 | |||

| Notes payable (+L) | 60,000 | |||

| (To record cash borrowed from bank) |

Table (2)

- Cash is an assets account and it increased the value of asset by $60,000. Hence, debit the cash account for $60,000.

- Notes payable is a liability account, and it increased the value of liabilities by $60,000. Hence, credit the notes payable for $60,000.

c. Building purchased on account and in cash:

| Date | Accounts title and explanation | Ref. | Debit ($) | Credit ($) |

| Building (+A) | 166,000 | |||

| Cash (-A) | 66,000 | |||

| Notes payable (+L) | 100,000 | |||

| (To record purchase of building on account and in cash) |

Table (3)

- Building is an assets account and it increased the value of asset by $166,000. Hence, debit the building account for $166,000.

- Cash is an assets account and it decreased the value of asset by $66,000. Hence, credit the cash account for $66,000.

- Notes payable is a liability account, and it increased the value of liabilities by $100,000. Hence, credit the notes payable for $100,000.

d. Equipment purchased:

| Date | Accounts title and explanation | Ref. | Debit ($) | Credit ($) |

| Equipment (+A) | 90,000 | |||

| Cash (-A) | 90,000 | |||

| (To record purchase of equipment in cash) |

Table (4)

- Equipment is an assets account and it increased the value of asset by $90,000. Hence, debit the equipment account for $90,000.

- Cash is an assets account and it decreased the value of asset by $90,000. Hence, credit the cash account for $90,000.

e. Purchase of supplies on account:

| Date | Accounts title and explanation | Ref. | Debit ($) | Credit ($) |

| Supplies (+A) | 90,000 | |||

| Accounts payable (+L) | 90,000 | |||

| (To record purchase of supplies on account) |

Table (5)

- Supplies are an assets account and it increased the value of asset by $90,000. Hence, debit the supplies account for $90,000.

- Accounts payable is a liability account and it increased the value of liability by $90,000. Hence, credit the liability account by $90,000.

Requirement – 3

To prepare: T-account for each account listed in the requirement 2.

Requirement – 3

Explanation of Solution

T-account:

T-account refers to an individual account, where the increasesor decreases in the value of specific asset, liability, stockholder’s equity, revenue, and expenditure items are recorded.

This account is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.’ An account consists of the three main components which are as follows:

- (a) The title of the account

- (b) The left or debit side

- (c) The right or credit side

T-accounts of Company B are as follows:

| Cash (A) | |||

| Beg. | 90,000 | ||

| (a) | 600,000 | 66,000 | (c) |

| (b) | 60,000 | 90,000 | (d) |

| End. | 594,000 | ||

| Supplies (A) | |||

| Beg. | 9,000 | ||

| (e) | 90,000 | ||

| End. | 99,000 | ||

| Equipment (A) | |||

| Beg. | 148,000 | ||

| (d) | 90,000 | ||

| End. | 238,000 | ||

| Buildings (A) | |||

| Beg. | 500,000 | ||

| (c) | 166,000 | ||

| End. | 666,000 | ||

| Land (A) | |||

| Beg. | 444,000 | ||

| End. | 444,000 | ||

| Accounts payable (L) | |||

| 50,000 | Beg. | ||

| 90,000 | (e) | ||

| 140,000 | End. | ||

| Note payable (L) | ||||

| 5,000 | Beg. | |||

| 60,000 | (b) | |||

| 100,000 | (c) | |||

| 165,000 | End. | |||

| Common stock (SE) | |||

| 170,000 | Beg. | ||

| 600,000 | (a) | ||

| 770,000 | End. | ||

| Retained earnings (SE) | |||

| 966,000 | Beg. | ||

| 966,000 | End. | ||

Requirement – 4

To prepare: The

Requirement – 4

Explanation of Solution

Trial balance:

Trial balance is the summary of accounts, and their debit and credit balances at a given time. It is usually prepared at end of the accounting period. Debit balances are listed in left column and credit balances are listed in right column. The totals of debit and credit column should be equal. Trial balance is useful in the preparation of the financial statements.

Trial balance of Company B is as follows:

| Company B | ||

| Adjusted Trial Balance | ||

| At July, 31 | ||

| Accounts | Debit ($) | Credit ($) |

| Cash | 594,000 | |

| Supplies | 99,000 | |

| Equipment | 238,000 | |

| Building | 666,000 | |

| Land | 444,000 | |

| Accounts payable | 140,000 | |

| Notes payable | 165,000 | |

| Common stock | 770,000 | |

| Retained earnings | 966,000 | |

| Totals | $2,041,000 | $2,041,000 |

Table (6)

Therefore, the total of debit, and credit columns of trial balance is $2,041,000 and agree.

Requirement – 5

To prepare: The classified balance sheet of Company B at July 31.

Requirement – 5

Explanation of Solution

Classified balance sheet:

This is the financial statement of a company which shows the grouping of similar assets and liabilities under subheadings.

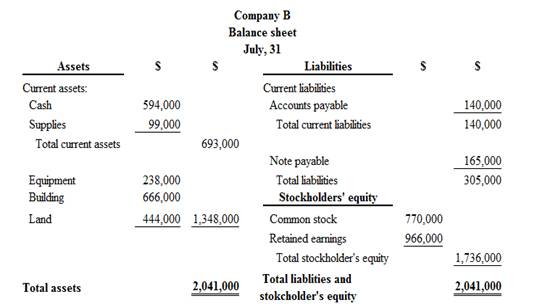

Classified balance sheet of Company B is as follows:

Figure (2)

Therefore, the total assets of Company B are$2,041,000, and the total liabilities and stockholders’ equity are $2,041,000.

Requirement – 6

Whether the assets amount of Company B is primarily come from liabilities or stockholders’ equity.

Requirement – 6

Explanation of Solution

The invested amount of assets are primarily come from stockholder’s’ equity of Company B, because the stockholder’s equity (common stock) financed $1,736,000 of the Company B’s total assets, and liabilities financed $305,000.

Want to see more full solutions like this?

Chapter 2 Solutions

Fundamentals of Financial Accounting

- Weave Company received a bank statement for the month of August. The bank statement showed the following information: Balance 1 August $68,326 Deposits 45,300 Cheques processed (63,222) Service charges (50) Monthly deposit into saving account directly (26,120) Deducted by bank from account (780) Balance, 31st August $49,574 Weave Co’s general ledger account had a balance of $78,304 at the end of August. (i) Deposits shown in the general ledger account but not in the bank amounting to $8,200; (ii) all cheques written by the company were processed by the bank except for those totaling $8,420; (iii) A $2,000 cheque to a supplier correctly recorded by the bank but was incorrectly recorded by the company as $200 credit to cash. Required: 1. Prepare a bank reconciliation statement for the month of August. 2. Prepare the necessary journal entries at the end of August to adjust the general ledger cash account.arrow_forwardManually journalize the following: a. Bank transfer from any bank to 1612CN amounting P30,000 b. cash Payment amounting P1000 to Acme Corporation. c. the company issued ordinary share capital worth of P 5,000, payment received and deposited on its GBP Bank Account 1 Dr. GBP Bank Account 1 P 5,000 Cr. Ordinary Share Capital P 5,000 d. the company recorded a Salary Expense worth of P 2500, paid for through the company's GBP Bank Account 1. Dr. Salaries and Wages P 2500 Cr. GBP Bank Account 1 P 2500 2 e. the company will pay a total of P 1500 from the Petty Cash fund for transportation related expenses. This transaction is still subject to supervisor's approval.arrow_forwardInfinity Emporium Company received the monthly statement for its bank account, showing a balance of $67,300 on August 31. The balance in the Cash account in the company's accounting system at that date was $72,628. The company's accountant reviewed the statement and the company's accounting records and noted the following. 1. 2. 3. After comparing the cheques written by the company with those deducted from the bank account in August, the accountant determined that all six cheques (totalling $6,180) that had been outstanding at the end of July were processed by the bank in August. However, five cheques written in August, totalling $4,500, were outstanding on August 31. A review of the deposits showed that a deposit made by the company on July 31 for $11,532 was recorded by the bank on August 1, and an August 31 deposit of $13,300 was recorded in the company's accounting system but had not yet been recorded by the bank. The August bank statement also showed: a service fee of $24 a…arrow_forward

- Accompanying a bank statement for Santee Company is a credit memo for $24,516 representing the principal ($22,700) and interest ($1,816) on a note that had been collected by the bank. The company had been notified by the bank at the time of the collection but had made no entries. Required: On March 1, journalize the entry that should be made by the company to bring the accounting records up to date. Refer to the chart of accounts for the exact wording of the account titles. CNOW journals do not use lines for journal explanations. Every line on a journal page is used for debit or credit entries. CNOW journals will automatically indent a credit entry when a credit amount is entered.arrow_forwardProvide journal entries to record each of the following transactions. For each, identify whether the transaction represents a source of cash (S), a use of cash (U), or neither (N). A. Paid $22,000 cash on bonds payable. B. Collected $12,600 cash for a note receivable. C. Declared a dividend to shareholders for $16,000, to be paid in the future. D. Paid $26,500 to suppliers for purchases on account. E. Purchased treasury stock for $18,000 cash.arrow_forwardPrepare journal entries to record the following transactions for the month of November: A. on first day of the month, issued common stock for cash, $20,000 B. on third day of month, purchased equipment for cash, $10,500 C. on tenth day of month, received cash for accounting services, $14,250 D. on fifteenth day of month, paid miscellaneous expenses, $3,200 E. on last day of month, paid employee salaries, $8,600arrow_forward

- Prepare journal entries to record the following transactions that occurred in April: A. on first day of the month, issued common stock for cash, $15,000 B. on eighth day of month, purchased supplies, on account, $1,800 C. on twentieth day of month, billed customer for services provided, $950 D. on twenty-fifth day of month, paid salaries to employees, $2,000 E. on thirtieth day of month, paid for dividends to shareholders, $500arrow_forwardJournal Entries Following is a list of transactions entered into during the first month of operations of Gardener Corporation, a new landscape service. Prepare in journal form the entry to record each transaction. April 1: Articles of incorporation are filed with the state, and 100,000 shares of common stock are issued for $100,000 in cash. April 4: A six-month promissory note is signed at the bank. Interest at 9% per annum will be repaid in six months along with the principal amount of the loan of $50,000. April 8: Land and a storage shed are acquired for a lump sum of $80,000. On the basis of an appraisal, 25% of the value is assigned to the land and the remainder to the building. April 10: Mowing equipment is purchased from a supplier at a total cost of $25,000. A down payment of $10,000 is made, with the remainder due by the end of the month. April 18: Customers are billed for services provided during the first half of the month. The total amount billed of $5,500 is due within ten days. April 27: The remaining balance due on the mowing equipment is paid to the supplier. April 28: The total amount of $5,500 due from customers is received. April 30: Customers are billed for services provided during the second half of the month. The total amount billed is $9,850. April 30: Salaries and wages of $4,650 for the month of April are paid.arrow_forwardPROBLEM 1: You obtained the following information on the current account of BUGOY CORP. During your examination of its financial statements for the year ended December 31, 2021. The bank statement on November 30, 2021 showed a balance of P918,000. Among the bank credits in November was customer's note for P300,000 collected for the account of the company which the company recognized in December among its receipts. Included in the bank debits were cost of checkbooks amounting to P3,600 and a P120,000 check which was charged by the bank in error against Bugoy's account. Also in November you ascertained that there were deposits in transit amounting to P240,000 and outstanding checks totaling P510,000. The bank statement for the month of December showed total credits of P1,248,000 and total charges of P612,000. The Company's books for December showed total debits of P2,206,800, total credits of P1,221,600 and a balance of P1,456,800. Bank debit memos for December were: No. 121 for service…arrow_forward

- Record all of these transactions in a cash disbursement journal table, such as this one: Date Explanation A/R Sub Account # Cash (debit) Sales Revenue (credit) Account Receivable (credit) Other (credit) Other Account Name Dec 1: Purchased 12,000 shares of treasury stock for $120,000 (Check #500 payable to Tennett Corp). The company expects to reissue these shares at a later date. Dec 1: Lent $50,000 in cash to one of its suppliers (Check #501 payable to Woodson Corp). The supplier signed a 1-year, 12% promissory note with a face value of $50,000. The note’s face value plus interest is due on 12/1/X6 Dec 4: Paid the Nelson Industries invoice for the balance owed. Dec 5: Paid the November utilities bill of $5,500 (this was already recognized as an expense in November). (Check #503 payable to Progress Energy) Dec 11: Paid Centennial, Inc. for the balance…arrow_forwardYou obtained the following information on the current account of Par Company during your examination of its financial statements for the year ended December 31, 2021. The bank statement on November 30, 2021 showed a balance of P 306,000 . Among the bank credits in November was customer’s noted for P 100,000 collected for the account of the company which the company recognized in December among its receipts. Included in the bank debits were costs of checkbooks amounting to P 1,200 and a P 40,000 check which was charged by the bank in error against Par Company account. Also in November, you ascertained that there were deposits in transit amounting to P 80,000 and outstanding checks totaling P 170,000. The bank statement for the month of December showed total credits of P 416,000 and total charges of P 204,000. The company’s books for December showed total debits of P 735,600 , total credits of P 407,200 and a balance of P485,600. Bank debit memos for December were: No. 121 for service…arrow_forwardThe Seattle First Company’s bank statement for the month of September indicated a balance of $13,375. The company’s cash account in the general ledger showed a balance of $10,030 on September 30. Other relevant information includes the following: Deposits in transit on September 30 total $9,850. The bank statement shows a debit memorandum for a check printing charge of $95. Check number 238 payable to Simon Company was recorded in the accounting records for $496 and cleared the bank for this same amount. A review of the records indicated that the Simon account now has a $72 credit balance and the check to them should have been $568. Outstanding checks as of September 30 totaled $11,600. Check No. 276 was correctly written and paid by the bank for $574. The check was recorded in the accounting records as a debit to accounts payable and a credit to cash for $754. The bank returned a NSF check in the amount of $1,110. The bank included a credit memorandum for $2,620 representing a…arrow_forward

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage- Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,