Videos

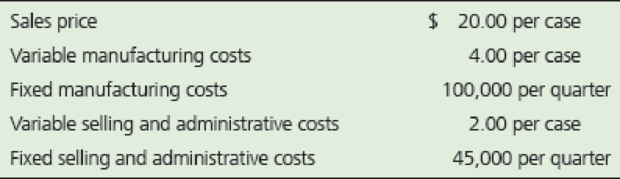

CF Industries Holdings, Inc. is one of the largest manufacturers and distributors of nitrogen fertilizer and other nitrogen products in the world. The corporation often produces and stores large amounts of inventory during periods of low demand to ensure that there is enough product to meet the demand of peak seasons. Assume that one line of fertilizer (with no beginning Finished Goods Inventory) had the following data during a time period of low demand:

Given that the time period has low demand, assume the company produced 1,000,000 cases but only sold 250,000 cases.

Requirement

- 1. Prepare the income statement for the quarter using variable costing.

- 2. Prepare the income statement for the quarter using absorption costing.

- 3. Why, if at all, is there a difference between operating income under the two methods?

Want to see the full answer?

Check out a sample textbook solution

Chapter 21 Solutions

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Additional Business Textbook Solutions

Managerial Accounting: Tools for Business Decision Making

Financial Accounting: Tools for Business Decision Making, 8th Edition

Fundamentals of Cost Accounting

Financial Accounting

Horngren's Accounting (11th Edition)

Principles of Accounting Volume 1

- The Chromosome Manufacturing Company produces two products, X and Y. The company president, Gene Mutation, is concerned about the fierce competition in the market for product X. He notes that competitors are selling X for a price well below Chromosome's price of P12.70. At the same time, he notes that competitors are pricing product Y almost twice as high as Chromosome's price of P12.50. Mr. Mutation has obtained the following data for a recent time period: PRODUCT X PRODUCT Y Number of Units 11,000 3,000 Direct Materials Cost Per Unit 3.23 3.09 Direct Labor Cost Per Unit 2.22 2.10 Direct Labor Hours 10,000 2,500 Machine Hours 2,100 2,800 Inspection Hours 80 100 Purchase Orders 10 10 Mr. Mutation has learned that overhead costs are assigned to products on the basis of direct labor hours. The overhead costs for his time period consisted of the following items: Overhead Cost Item Amount Inspecting Costs…arrow_forwardMarshall Company is a large manufacturer of office furniture. The company has recently adopted lean accounting and has identified two value streams-office chairs and office tables. Total sales in the most recent period for the two streams are $245 and $310 million, respectively. In the most recent accounting period, Marshall had the following operating costs, which were traced to the two value streams as follows (in thousands): Operating costs: Materials Labor Equipment-related costs Occupancy costs Sales Operating costs: Total operating costs Value-stream profit before inventory change In addition to the traceable operating costs, the company had manufacturing costs of $116.750 million, and selling and administrative costs of $25 million that could not be traced to either value stream. Due to the implementation of lean methods, the firm has been able to reduce Inventory In both value streams significantly. Marshall has calculated the fixed cost of prior-period Inventory that is…arrow_forwardA corporation has an excess input VAT due to its excessive local purchases of goods and services. This excess input VAT is accumulating every month and reached a significant value. The management is considering to deal with the excess input VAT. Assume that the excess input VAT is directly attributable to its Zero-rated VAT Sales, explain the options that could possibly be considered by the management.arrow_forward

- The head of operations of a manufacturing company has conducted an analysis with respect to the capacity of his production line. The major findings are the following: Theoretical capacity is 530 units per day. The effective capacity is 515 units per day The process capacity is 450 units per day. Two projects have been proposed to increase the capacity. The first proposal focuses on improving maintenance in order to reduce machine breakdowns. The second proposal focuses on increasing the capacity of the inventory buffer between various stages. Given that there is only enough budget to implement one of the proposals, which proposal should be selected based on the given information. Clearly motivate your answer. Please do fast.. ASAP ..fast pleasearrow_forwardThe Eastern division sells goods internally to the Western division of the same company. The quoted external price in industry publications from a supplier near Eastern is $200 per ton plus transportation. It costs $20 per ton to transport the goods to Western. Eastern's actual market cost per ton to buy the direct materials to make the transferred product is $100. Actual per ton direct labor is $50. Other actual costs of storage and handling are $40. Assuming there is an excess capcity in the Eastern Division, the minimum and maximum transfer price are:arrow_forwardKimball Company has developed the following cost formulas: Materialusage:Ym=80X;r=0.95Laborusage(direct):Yl=20X;r=0.96Overheadactivity:Yo=350,000+100X;r=0.75Sellingactivity:Ys=50,000+10X;r=0.93 where X=Directlaborhours The company has a policy of producing on demand and keeps very little, if any, finished goods inventory (thus, units produced equals units sold). Each unit uses one direct labor hour for production. The president of Kimball Company has recently implemented a policy that any special orders will be accepted if they cover the costs that the orders cause. This policy was implemented because Kimballs industry is in a recession and the company is producing well below capacity (and expects to continue doing so for the coming year). The president is willing to accept orders that minimally cover their variable costs so that the company can keep its employees and avoid layoffs. Also, any orders above variable costs will increase overall profitability of the company. Required: 1. Compute the total unit variable cost. Suppose that Kimball has an opportunity to accept an order for 20,000 units at 220 per unit. Should Kimball accept the order? (The order would not displace any of Kimballs regular orders.) 2. Explain the significance of the coefficient of correlation measures for the cost formulas. Did these measures have a bearing on your answer in Requirement 1? Should they have a bearing? Why or why not? 3. Suppose that a multiple regression equation is developed for overhead costs: Y = 100,000 + 100X1 + 5,000X2 + 300X3, where X1 = direct labor hours, X2 = number of setups, and X3 = engineering hours. The coefficient of determination for the equation is 0.94. Assume that the order of 20,000 units requires 12 setups and 600 engineering hours. Given this new information, should the company accept the special order referred to in Requirement 1? Is there any other information about cost behavior that you would like to have? Explain.arrow_forward

- To help in the analysis, Kaylin gathered the following data for LLHC for 20X1: Tons sold: 10 Average cartons per shipment: 2 Average shipments per ton: 7 1) Comment on Ryan’s proposal to drop some high-volume products and place more emphasis on low-volume products. Discuss the role of the accounting system in supporting this type of decision-making.arrow_forwardMaximin currently manufactures and sells two types of a product, the Max and the Min. Both of these products use the same raw materials but in different quantities. The Max is a superior version of the Min and uses more materials and labour. However, due to superior quality, the retail price for the Max is double than that of the Min. You have been provided with details of last year's sales and costs below, when the company operated at 80% capacity. It is assumed all units produced are sold, i.e., there is no stock. Product Max Min Selling price p.u. Variable cost p.u. €16 €8 €8 €5 Sales (units) 1.2m 0.8m Total fixed costs amounted to €4.2m. If the company operates at more than 80% capacity, it will then have to employ a further 1 manager and 2 supervisors, each with an annual salary of €60,000 for the manager and €40,000 for the supervisor respectively, in order to comply with the local legislation. Due to the economic recession, the companys market researchers are predicting that…arrow_forwardZuzu is a large manufacturer of snack cakes. The company operates distribution centers in Chicago. The distribution center bakes and packages the snack cakes and ships them to grocery warehouses throughout the country. Because of the high standards set for both quality and appearance, there is a reasonable number of “seconds” that do not meet standards and are sold to company outlets for sale at reduced prices. In recent years, the company’s average yield has been 90% of first-quality products for sale to grocery warehouses. The remaining 10% is sent to the outlet store. Zuzu’s performance-evaluation system pays its distribution center managers substantial bonuses if the company achieves annual budgeted profit numbers. In the last quarter of 2017, Noah Spalding, Zuzu’s controller, noted a significant increase in yield percentage of the Chicago distribution center, from 90% to 98%. This increase resulted in a 10% increase in the center’s profits. During a recent trip to the Chicago…arrow_forward

- Zuzu is a large manufacturer of snack cakes. The company operates distribution centers in Chicago. The distribution center bakes and packages the snack cakes and ships them to grocery warehouses throughout the country. Because of the high standards set for both quality and appearance, there is a reasonable number of “seconds” that do not meet standards and are sold to company outlets for sale at reduced prices. In recent years, the company’s average yield has been 90% of first-quality products for sale to grocery warehouses. The remaining 10% is sent to the outlet store. Zuzu’s performance-evaluation system pays its distribution center managers substantial bonuses if the company achieves annual budgeted profit numbers. In the last quarter of 2017, Noah Spalding, Zuzu’s controller, noted a significant increase in yield percentage of the Chicago distribution center, from 90% to 98%. This increase resulted in a 10% increase in the center’s profits. During a recent trip to the Chicago…arrow_forwardSupermart Food Stores (SFS) has experienced net operating losses in its frozen food products line in the last few periods. Management believes that the store can improve its profitability if SFS discontinues frozen foods. The operating results from the most recent period are: Order processing Receiving Shelf-stocking Customer support Sales Cost of goods sold SFS estimates that store support expenses, in total, are approximately 20% of revenues. The controller says that not every sales dollar requires or uses the same amount of store support activities. A preliminary analysis reveals store support activities for these three product lines are: Frozen Foods $ 120,000 185,000 Activity (cost driver) Order processing (number of purchase orders) Receiving (number of deliveries) Shelf-stocking (number of hours per delivery) Customer support (total units sold) The controller estimates activity-cost rates for each activity as follows: $ 88 per purchase order 110 per delivery per hour per item…arrow_forwardTool Industries manufactures large workbenches for industrial use. Sam Hartnet, the Vice President for marketing at Tool Industries, concluded from market analysis that sales were dwindling for Tool's workbenches due to aggressive pricing by competitors. Tool's workbench sells for $1,140 whereas the competition's comparable workbench sells for $1,060. Sam determined that a price drop to $1,060 would be necessary to protect its market share and maintain an annual sales level of 13,000 workbenches.Cost data based on sales of 13,000 workbenches: Budgeted Quantity Actual Quantity Actual Cost Direct materials (pounds) 175,000 168,000 $ 3,450,000 Direct labor (hours) 72,800 71,500 825,000 Machine setups (number of setups) 900 880 250,000 Mechanical assembly (machine hours) 273,000 281,250 3,750,000 If the profit per unit is maintained, the target cost per unit is (rounded to the nearest whole dollar): Multiple Choice $489. $557. $516. $424.…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning