Videos

Flexible budgeting, performance measurement, and ethics

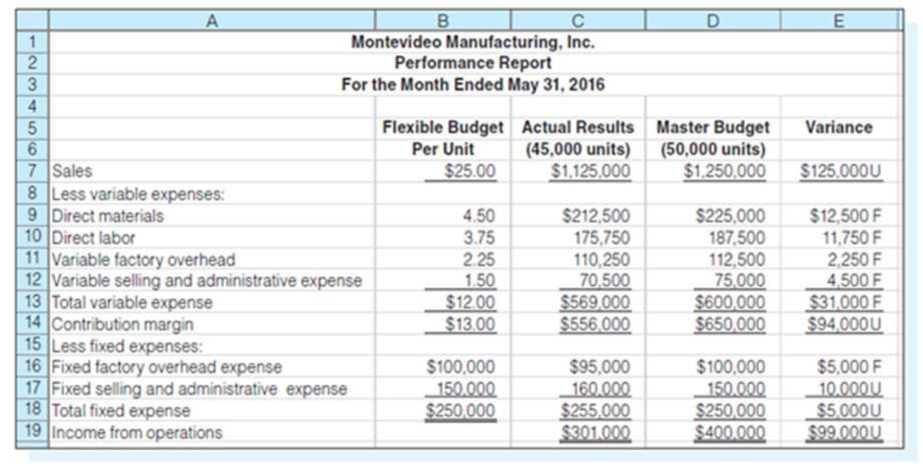

Montevideo Manufacturing, Inc. produces a single type of small motor. The bookkeeper who does not have an in-depth understanding of accounting principles prepared the following performance report with the help of the production manager.

In a conversation with the sales manager, the production manager was overheard saying, “You sales guys really messed up our May performance, and it is only because production did such a great

Required:

- 1. Do you agree with the production manager that the manufacturing area did a good job of controlling costs?

- 2. Prepare a flexible budget for Montevideo Manufacturing’s expenses at the following activity levels: 45,000 units, 50,000 units, and 55,000 units.

- 3. Prepare a revised performance report, using the most appropriate flexible budget from (2) above.

- 4. Now what is your response to the production manager’s claim?

- 5. Assume that you have just been hired as the new accountant. You observe that the production manager is about to receive a large bonus based on the favorable materials, labor, and factory overhead variances indicated in the flexible budget prepared by the bookkeeper. Using the IMA Statement of Ethical Professional Practice as your guide, what standards, if any, apply to your responsibilities in this matter?

Want to see the full answer?

Check out a sample textbook solution

Chapter 7 Solutions

Principles of Cost Accounting

Additional Business Textbook Solutions

Horngren's Financial & Managerial Accounting, The Financial Chapters (Book & Access Card)

Managerial Accounting (5th Edition)

Accounting For Governmental & Nonprofit Entities

Advanced Financial Accounting

Financial Accounting: Tools for Business Decision Making, 8th Edition

Auditing And Assurance Services

- Andrew Jarvis started his manufacturing business earlier this year and has been preparing management accounts using variable (marginal) costing. He has approached you as a Certified Chartered Management Accountant, to help his finance team prepare annual financial statements. As part of your discussions with the company’s finance team, you mentioned that you will use absorption costing to prepare the financial statements. Peter Cullen, the Finance Manager, said that he was unfamiliar with this method of costing and has asked you for more information about it.REQUIREMENT:Draft a Report for Peter Cullen that:a) Describes and explains the basis of variable (marginal) and absorption costing systems.b) Explains the effect on profit of using variable (marginal) and absorption costing. c) Outlines TWO advantages and TWO disadvantages of both variable (marginal) AND absorption costing systems.arrow_forwardAndrew Jarvis started his manufacturing business earlier this year and has been preparing management accounts using variable (marginal) costing. He has approached you as a Certified Chartered Management Accountant, to help his finance team prepare annual financial statements. As part of your discussions with the company’s finance team, you mentioned that you will use absorption costing to prepare the financial statements. Peter Cullen, the Finance Manager, said that he was unfamiliar with this method of costing and has asked you for more information about it. Draft a Report for Peter Cullen that:a) Describes and explains the basis of variable (marginal) and absorption costing systems. b) Explains the effect on profit of using variable (marginal) and absorption costing. c) Outlines TWO advantages and TWO disadvantages of both variable (marginal) AND absorption costing systems.arrow_forwardThe Managerial ProcessEach of the following scenarios requires the use of accountinginformation to carry out one or more managerial accounting objectives.a. Laboratory Manager: An HMO approached me recently andoffered us its entire range of blood tests. It provided a price listrevealing the amount it is willing to pay for each test. In manycases, the prices are below what we normally charge. I need toknow the costs of the individual tests to assess the feasibility ofaccepting its offer and perhaps suggest price adjustments on someof the tests.b. Operating Manager: This report indicates that we have 30% moredefects than originally targeted. An investigation into the cause hasrevealed the problem. We were using a lower-quality material thanexpected, and the waste has been higher than normal. Byswitching to the quality level originally specified, we can reducethe defects to the planned level. c. Divisional Manager: Our market share has increased because ofhigher-quality products. Current…arrow_forward

- Discuss how allocation of customer-related overhead cost can lead to better decision making within firms with reference to the case below. ‘An insurance company, A-Insure Limited, decided to use CPA to identify profitable and non-profitable customers after it grew concerned about the poor financial performance of one of its policy options. A-Insure collected customer data through original policy proposal forms which were stored electronically in a customer database. It was able to conduct a complex cross correlation between known cost drivers and the demographic and other characteristics of policy holders. The cost drivers were: • commission payments to financial advisers who sold the policy • early surrender of the policy by the policy holder • changing of bank details and consequent chasing of missed premiums • responding to customer queries. The analysis identified that the policy was unprofitable when sold to recently retired clients but was profitable when sold to other client…arrow_forwardDropping a customer, activity-based costing, ethics. Justin Anders is the management accountant for Carey Restaurant Supply (CRS). Sara Brinkley, the CRS sales manager, and Justin are meeting to discuss the profitability of one of the customers, Donnelly’s Pizza. Justin hands Sara the following analysis of Donnelly’s activity during the last quarter, taken from CRS’s activity-based costing system: Sara looks at the report and remarks, “I’m glad to see all my hard work is paying off with Donnelly’s. Sales have gone up 10% over the previous quarter!” Justin replies, “Increased sales are great, but I’m worried about Donnelly’s margin, Sara. We were showing a profit with Donnelly’s at the lower sales level, but now we’re showing a loss. Gross margin percentage this quarter was 40%, down five percentage points from the prior quarter. I’m afraid that corporate will push hard to drop them as a customer if things don’t turn around.” “That’s crazy,” Sara responds. “A lot of that overhead for…arrow_forwardThese are measures not found in the chart of accounts, such as customer satisfaction scores or product quality measures. A. Quality measures B. Non-financial measures C. Financial Measures D. Balanced Scorecard A manager would like to see reduction of the following operational measures, except: A. Spoilage B. Number of customer complaints C. Queue time D. Manufacturing Efficiencyarrow_forward

- You work for Alphabet Holdings Plc as a junior management accountant. The board of directors are considering ways to improve the suboptimal performance of an investment in a manufacturing company called DEF products Ltd. As you can see from the table below the directors are considering closing products Bozon and Carbon in an effort to improve overall profitability. You spot that marginal costing would show the results differently and may affect the directors’ decision. Requirements for Question 2 Use your knowledge of management accounting and marginal costing to calculate the contribution of each product Use your findings from part (a) and appropriate academic references to explain whether the company should stop making product Bozon Use your findings from part (a) and appropriate academic references to explain whether the company should stop making product Carbon Discuss how and why marginal costing calculates contribution to pay overheads and why this is…arrow_forwardKathy Shorts, president of Oliver Company, was concerned with the trend in sales and profitability. The company had been losing customers at an alarming rate. Furthermore, the company was barely breaking even. Investigation revealed that poor quality was at the root of the problem. At the end of 20x5, Kathy decided to begin a quality improvement program. As a first step, she identified the following costs in the accounting records as quality related: Required: 1. Prepare a quality cost report by quality cost category. 2. Calculate the relative distribution percentages for each quality cost category. Comment on the distribution. 3. Using the Taguchi loss function, an average loss per unit is computed to be 15 per unit. What are the hidden costs of external failure? How does this affect the relative distribution? 4. Shortss quality manager decided not to bother with the hidden costs. What do you think was his reasoning? Any efforts to reduce measured external failure costs will also reduce the hidden costs. Do you agree or disagree? Explain.arrow_forwardIn 20X1, Don Blackburn, president of Price Electronics, received a report indicating that quality costs were 31% of sales. Faced with increasing pressures from imported goods. Don resolved to take measures to improve the overall quality of the companys products. After hiring a consultant in 20X1, the company began an aggressive program of total quality control. At the end of 20X5, Don requested an analysis of the progress the company had made in reducing and controlling quality costs. The accounting department assembled the following data: Required: 1. Compute the quality costs as a percentage of sales by category and in total for each year. 2. Prepare a multiple-year trend graph for quality costs, both by total costs and by category. Using the graph, assess the progress made in reducing and controlling quality costs. Does the graph provide evidence that quality has improved? Explain. 3. Using the 20X1 quality cost relationships (assume all costs are variable), calculate the quality costs that would have prevailed in 20X4. By how much did profits increase in 20X4 because of the quality improvement program? Repeat for 20X5.arrow_forward

- Assume you have been hired by Cabelas Sporting Goods. As part of your new role in the accounting department, you have been tasked to set up a responsibility accounting structure for the company. As your first task, your supervisor has asked you to give an example of a cost center, profit center, and an investment center within the Cabelas organization. Your supervisor is a little unsure of the difference between a profit center and investment center and would like you to explain the difference.arrow_forwardRizzo Goal Inc. produces and sells hockey equipment, often custom made for online orders. The company has the following performance metrics on its balanced scorecard: days from ordered to delivered, number of shipping errors, customer retention rate, and market share. A measure map illustrates that the days from ordered to delivered and the number of shipping errors are both expected to directly affect the customer retention rate, which affects market share. Additional internal analysis finds that: Every shipping error over three shipping errors per month reduces the customer retention rate by 1.5%. On average, each day above three days from ordered to delivered yields a reduction in the customer retention rate of 1%. Each day before three days from order to delivery yields an increase in the customer retention rate of 1%, on average. Rizzo Goal Inc.s current customer retention rate is 60%. The company estimates that for every 1% increase or decrease in the customer retention rate, market share changes 0.5% in the same direction. Rizzo Goal Inc.s current market share is 21.4%. Ignoring any other factors, if the company has six shipping errors this month and an average of 3.5 days from ordered to delivered, determine (a) the new customer retention rate and (b) the new market share that Rizzo Goal Inc. expects to have.arrow_forwardThe Managerial Process Each of the following scenarios requires the use of accounting information to carry out one or more managerial accounting objectives. a. Laboratory Manager: An HMO approached me recently and offered us its entire range of blood tests. It provided a price list revealing the amount it is willing to pay for each test. In many cases, the prices are below what we normally charge. I need to know the costs of the individual tests to assess the feasibility of accepting its offer and perhaps suggest price adjustments on some of the tests. b. Operating Manager: This report indicates that we have 30% more defects than originally targeted. An investigation into the cause has revealed the problem. We were using a lower-quality material than expected, and the waste has been higher than normal. By switching to the quality level originally specified, we can reduce the defects to the planned level. c. Divisional Manager: Our market share has increased because of higher-quality products. Current projections indicate that we should sell 25% more units than last year. I want a projection of the effect that this increase in sales will have on profits. I also want to know our expected cash receipts and cash expenditures on a month-by-month basis. I have a feeling that some short-term borrowing may be necessary. d. Plant Manager: Foreign competitors are producing goods with lower costs and delivering them more rapidly than we can to customers in our markets. We need to decrease the cycle time and increase the efficiency of our manufacturing process. There are two proposals that should help us accomplish these goals, both of which involve investing in computer-aided manufacturing. I need to know the future cash flows associated with each system and the effect each system has on unit costs and cycle time. e. Manager: At the last board meeting, we established an objective of earning a 25% return on sales. I need to know how many units of our product we need to sell to meet this objective. Once I have the estimated sales in units, we need to outline a promotional campaign that will take us where we want to be. However, in order to compute the targeted sales in units, I need to know the expected unit price and a lot of cost information. f. Manager: Perhaps the Harrison Medical Clinic should not offer a full range of medical services. Some services seem to be having a difficult time showing any kind of profit. I am particularly concerned about the mental health service. It has not shown a profit since the clinic opened. I want to know what costs can be avoided if I drop the service. I also want some assessment of the impact on the other services we offer. Some of our patients may choose this clinic because we offer a full range of services. Required: Select the managerial accounting objective(s) that are applicable for each scenario: planning, controlling (including performance evaluation), or decision making.arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College