Concept explainers

Videos

Cost Flows through Accounts

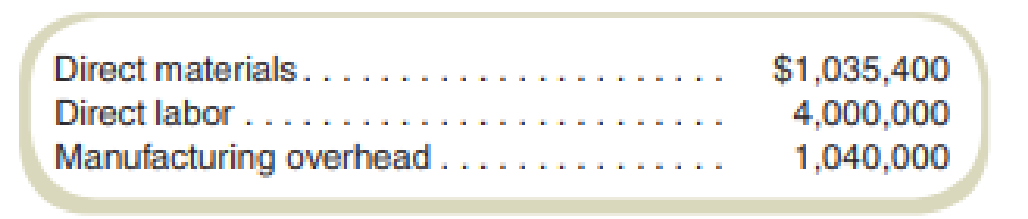

Brighton Services repairs locomotive engines. It employs 100 full-time workers at $20 per hour. Despite operating at capacity, last year’s performance was a great disappointment to the managers. In total, 10 jobs were accepted and completed, incurring the following total costs:

Of the $1,040,000 manufacturing

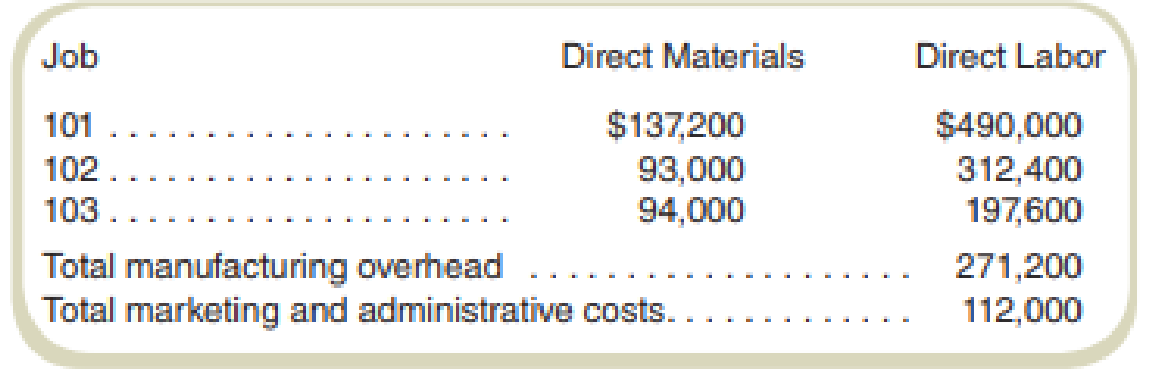

This year, Brighton Services expects to operate at the same activity level as last year, and overhead costs and the wage rate are not expected to change. For the first quarter of this year, Brighton Services completed two jobs and was beginning the third (Job 103). The costs incurred follow:

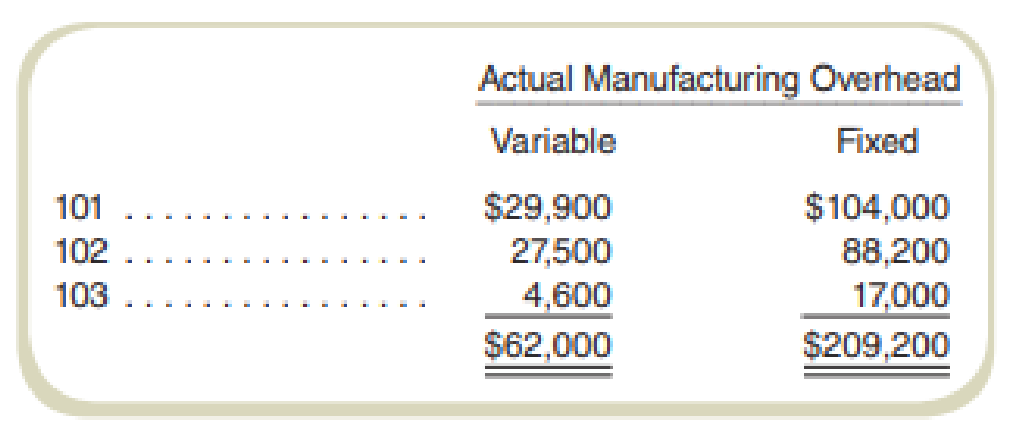

You are a consultant associated with Lodi Consultants, which Brighton Services has asked for help. Lodi’s senior partner has examined Brighton Services’s accounts and has decided to divide actual factory overhead by job into fixed and variable portions as follows:

In the first quarter of this year, 40 percent of marketing and administrative cost was variable and 60 percent was fixed. You are told that Jobs 101 and 102 were sold for $850,000 and $550,000, respectively. All over- or underapplied overhead for the quarter is written off to Cost of Goods Sold.

Required

- a. Present in T-accounts the actual

manufacturing cost flows for the three jobs in the first quarter of this year. - b. Using last year’s overhead costs and direct labor-hours as this year’s estimate, calculate predetermined overhead rates per direct labor-hour for variable and fixed overhead.

- c. Present in T-accounts the normal manufacturing cost flows for the three jobs in the first quarter of this year. Use the overhead rates derived in requirement (b).

- d. Prepare income statements for the first quarter of this year under the following costing systems:

- (1) Actual.

- (2) Normal.

a.

Compute in T-accounts: the actual manufacturing cost flows for the three jobs in the first quarter of this year.

Explanation of Solution

T-accounts in job costing: The ledger accounts are also termed as T-accounts which are prepared after the recording of the journal entry of the transactions. The balances of raw materials, work-in-process, finished goods inventory and overheads from the journal book are transferred to the respective T-accounts.

T-account of materials inventory:

| Materials inventory | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| $ 137,200 | |||||

| $ 93,000 | |||||

| $ 94,000 | |||||

Table: (1)

T-account of wages payable:

| Wages payable | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| $ 490,000 | |||||

| $ 312,400 | |||||

| $ 197,600 | |||||

Table: (2)

T-account of variable manufacturing overhead:

| Variable manufacturing overhead | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| $ 62,000 | $ 29,900 | ||||

| $ 27,500 | |||||

| $ 4,600 | |||||

Table: (3)

T-account of fixed manufacturing overhead:

| Fixed manufacturing overhead | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| $ 209,200 | $ 104,000 | ||||

| $ 88,200 | |||||

| $ 17,000 | |||||

Table: (4)

T-account of work-in-process inventory:

| Work-in-process inventory | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| $ 324,200 | $ 761,100 | ||||

| $ 1,000,000 | $ 521,100 | ||||

| $ 62,000 | |||||

| $ 209,200 | |||||

Table: (5)

T-account of finished goods inventory:

| Finished goods inventory | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| $ 761,100 | |||||

| $ 521,100 | $ 1,282,200 | ||||

Table: (6)

T-account of the cost of goods sold:

| Cost of goods sold | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| $ 1,282,200 | |||||

Table: (7)

b.

Calculate predetermined overhead rates per direct labor-hour for variable and fixed overhead by using last year’s overhead costs and direct labor-hours.

Explanation of Solution

Predetermined overhead rate: The predetermined overhead rate is the rate computed for applying manufacturing overheads to the work-in-process inventory. This rate can be computed by dividing the total amount of manufacturing overheads by the base of allocation. The formula for calculating the predetermined overhead rate is:

Compute the predetermined variable overhead rate:

Compute the predetermined fixed overhead rate:

Working note 1:

Compute the total direct labor-hours:

Working note 2:

Compute the variable manufacturing overhead:

Working note 3:

Compute the fixed manufacturing overhead:

c.

Present in T-accounts the normal manufacturing cost flows for the three jobs in the first quarter of this year by using the overhead rates derived as per the previous part.

Explanation of Solution

T-accounts in job costing: The ledger accounts are also termed as T-accounts which are prepared after the recording of the journal entry of the transactions. The balances of raw materials, work-in-process, finished goods inventory and overheads from the journal book are transferred to the respective T-accounts.

T-account of materials inventory:

| Materials inventory | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| $ 137,200 | |||||

| $ 93,000 | |||||

| $ 94,000 | |||||

Table: (8)

T-account of wages payable:

| Wages payable | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| $ 490,000 | |||||

| $ 312,400 | |||||

| $ 197,600 | |||||

Table: (9)

T-account of variable manufacturing overhead:

| Variable manufacturing overhead | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| $ 62,000 | $ 38,220 | ||||

| $ 16,000 | $ 24,367 | ||||

| $ 15,413 | |||||

Table: (10)

T-account of fixed manufacturing overhead:

| Fixed manufacturing overhead | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| $ 182,000 | $ 89,180 | ||||

| $ 56,857 | |||||

| $ 35,963 | |||||

| $ 27,200 | |||||

Table: (11)

T-account of work-in-process inventory:

| Work-in-process inventory | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| $ 324,200 | $ 754,600 | ||||

| $ 1,000,000 | $ 486,624 | ||||

| $ 78,000 | |||||

| $ 182,000 | |||||

Table: (12)

T-account of finished goods inventory:

| Finished goods inventory | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| $ 754,600 | |||||

| $ 486,624 | $ 1,241,224 | ||||

Table: (13)

T-account of the cost of goods sold:

| Cost of goods sold | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| $ 1,241,224 | |||||

Table: (14)

T-account of under-or over-applied overhead

| Under-or over-applied overhead | |||||

| Date | Particulars | Amount | Date | Particulars | Amount |

| $ 27,200 | $ 16,000 | ||||

Table: (15)

d.

Prepare the income statement for the first quarter of this year using actual and normal systems.

Explanation of Solution

Normal system of costing: Under normal costing, the cost of a job is determined by using the actual direct material, and the labor cost by adding overhead applied using a predetermined rate and an actual allocation base.

Actual system of costing: The cost of a job is determined by using the actual direct material, and the labor cost by adding overhead applied using an actual overhead rate and an actual allocation base under actual costing.

Income statement using actual system:

| Particulars | Amount |

| Sales Revenue | $ 1,400,000 |

| Less: Cost of goods sold | ($ 1,282,200) |

| Gross margin | $ 117,800 |

| Less: (Under-) Over applied overhead | $ 0 |

| Marketing and administrative costs | ($ 112,000) |

| Operating profit (loss) | $ 5,800 |

Income statement using normal system:

| Particulars | Normal |

| Sales Revenue | $ 1,400,000 |

| Less: Cost of goods sold | ($ 1,241,224) |

| Gross margin | $ 158,776 |

| Less: (Under-) Over applied overhead | $ 11,200 |

| Marketing and administrative costs | ($ 112,000) |

| Operating profit (loss) | $ 35,576 |

Want to see more full solutions like this?

Chapter 7 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- Handbrain Inc. is considering a change to activity-based product costing. The company produces two products, cell phones and tablet PCs, in a single production department. The production department is estimated to require 2,000 direct labor hours. The total indirect labor is budgeted to be 200,000. Time records from indirect labor employees revealed that they spent 30% of their time setting up production runs and 70% of their time supporting actual production. The following information about cell phones and tablet PCs was determined from the corporate records: a. Determine the indirect labor cost per unit allocated to cell phones and tablet PCs under a single plantwide factory overhead rate system using the direct labor hours as the allocation base. b. Determine the budgeted activity costs and activity rates for the indirect labor under activity-based costing. Assume two activitiesone for setup and the other for production support. c. Determine the activity cost per unit for indirect labor allocated to each product under activity-based costing. d. Why are the per-unit allocated costs in (a) different from the per-unit activity cost assigned to the products in (c)?arrow_forwardSmokeCity, Inc., manufactures barbeque smokers. Based on past experience, SmokeCity has found that its total annual overhead costs can be represented by the following formula: Overhead cost = 543,000 + 1.34X, where X equals number of smokers. Last year, SmokeCity produced 20,000 smokers. Actual overhead costs for the year were as expected. Required: 1. What is the driver for the overhead activity? 2. What is the total overhead cost incurred by SmokeCity last year? 3. What is the total fixed overhead cost incurred by SmokeCity last year? 4. What is the total variable overhead cost incurred by SmokeCity last year? 5. What is the overhead cost per unit produced? 6. What is the fixed overhead cost per unit? 7. What is the variable overhead cost per unit? 8. Recalculate Requirements 5, 6, and 7 for the following levels of production: (a) 19,500 units and (b) 21,600 units. (Round your answers to the nearest cent.) Explain this outcome.arrow_forwardPocono Cement Forms expects $900,000 in overhead during the next year. It does not know whether it should apply overhead on the basis of its anticipated direct labor hours of 60,000 or its expected machine hours of 30,000. Determine the product cost under each predetermined allocation rate if the last job incurred $1,550 in direct material cost, 90 direct labor hours, and 75 machine hours. Wages are paid at $16 per hour.arrow_forward

- Natur-Gro, Inc., manufactures composters. Based on past experience, Natur-Gro has found that its total annual overhead costs can be represented by the following formula: Overhead cost = 264,000 + 1.42X, where X equals number of composters. Last year, Natur-Gro produced 30,000 composters. Actual overhead costs for the year were as expected. Total overhead for per unit was a. 1.42 b. 8.80 c. 11.63 d. 10.22arrow_forwardRoper Furniture manufactures office furniture and tracks cost data across their process. The following are some of the costs that they incur. Classify these costs as fixed or variable costs, and as product costs or period costs. Wood used to produce desks ($125,00 per desk) Production labor used to produce desks ($15 per hour) Production supervisor salary ($45,000 per year) Depreciation on factory equipment ($60,000 per year) Selling and administrative expenses ($45,000 per year) Rent on corporate office ($44,000 per year) Nails, glue, and other materials required to produce desks (varies per desk) Utilities expenses for production facility Sales staff commission (5% of gross sales)arrow_forwardBolger and Co. manufactures large gaskets for the turbine industry. Bolgers per-unit sales price and variable costs for the current year are as follows: Bolgers total fixed costs aggregate to 360,000. Bolgers labor agreement is expiring at the end of the year, and management is concerned about the effects of a new labor agreement on its break-even point in units. The controller performed a sensitivity analysis to ascertain the estimated effect of a 10-per-unit direct labor increase and a 10,000 reduction in fixed costs. Based on these data, the break-even point would: a. decrease by 1,000 units. b. decrease by 125 units. c. increase by 375 units. d. increase by 500 units.arrow_forward

- Flaherty, Inc., has just completed its first year of operations. The unit costs on a normal costing basis are as follows: During the year, the company had the following activity: Actual fixed overhead was 12,000 less than budgeted fixed overhead. Budgeted variable overhead was 5,000 less than the actual variable overhead. The company used an expected actual activity level of 12,000 direct labor hours to compute the predetermined overhead rates. Any overhead variances are closed to Cost of Goods Sold. Required: 1. Compute the unit cost using (a) absorption costing and (b) variable costing. 2. Prepare an absorption-costing income statement. 3. Prepare a variable-costing income statement. 4. Reconcile the difference between the two income statements.arrow_forwardRemarkable Enterprises requires four units of part A for every unit of Al that it produces. Currently, part A is made by Remarkable, with these per-unit costs in a month when 4,000 units were produced: Variable manufacturing overhead is applied at $1.60 per unit. The other $0.50 of overhead consists of allocated fixed costs. Remarkable will need 8,000 units of part A for the next years production. Altoona Corporation has offered to supply 8,000 units of part A at a price of $8.00 per unit. If Remarkable accepts the offer, all of the variable costs and $2,000 of the fixed costs will be avoided. Should Remarkable accept the offer from Altoona Corporation?arrow_forwardBobcat uses a traditional cost system and estimates next years overhead will be $800.000, as driven by the estimated 25,000 direct labor hours. It manufactures three products and estimates the following costs: If the labor rate is $30 per hour, what is the per-unit cost of each product?arrow_forward

- 2. Gemini is having trouble understanding its manufacturing overhead costs. A couple of years ago, management used the conference method and determined that the its monthly manufacturing overhead costs consisted of $10,000 plus $50 for every machine hour. The actual costs and those based on the conference method were significantly different from each other the last few months. Management has asked you to analyze its costs to better predict manufacturing overhead costs. Management has the following data from the past year for you. Manufacturing Month Machine Hours Overhead Costs 1 1,200 $74,000 2 1,000 70,000 1,400 82,000 4 1,700 86,000 1,650 87,500 6 1,800 87,000 1,900 92,000 8 1,800 90,000 9. 2,000 98,000 10 3,000 130,000 11 2,200 102,000 12 2,600 109,000 1. Use the High-Low method and estimate the linear cost relationship for manufacturing overhead costs. 2. Compare the predicted costs for months 11 and 12 using your cost relationship to that previously used. Which is better and why?…arrow_forwardMariposa, Inc., produces machine tools and currently uses a plantwide overhead rate, based on machine hours. Harry Whipple, the plant manager, has heard that departmental overhead rates can offer significantly better cost assignments than can a plantwide rate. Mariposa has the following data for its two departments for the coming year: Department A Department B Overhead costs (expected) $528,000 $132,000 Normal activity (machine hours) 110,000 55,000 Required: 1. Compute a predetermined overhead rate for the plant as a whole based on machine hours.$fill in the blank 1 per machine hour 2. Compute predetermined overhead rates for each department using machine hours. Round your answers to one decimal place. Department A $fill in the blank 2 per machine hour Department B $fill in the blank 3 per machine hour 3. Suppose that a machine tool (Product X75) used 60 machine hours from Department A and 140 machine hours from Department B. A second machine tool (Product Y15)…arrow_forwardThe Macon Company uses the high-low method to determine its cost equation. The following information was gathered for the past year: Machine Hours Direct Labor Costs Busiest month (June) 24,000 $ 282,400 Slowest month (December) 18,000 $ 220,000 If Macon expects to use 20,000 machine hours next month, what are the estimated direct labor costs?arrow_forward

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub