Concept explainers

Videos

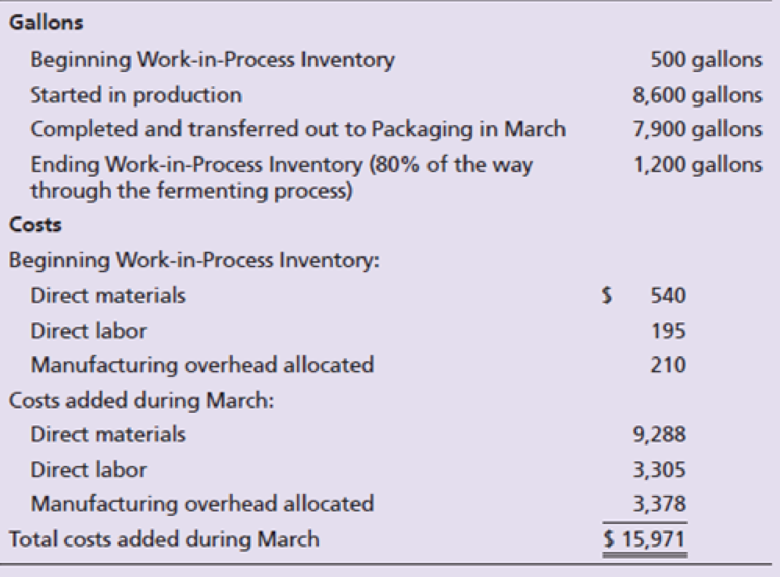

Shea Winery- in Pleasant Valley, New York, has two departments: Fermenting and Packaging. Direct materials are added at the beginning of the fermenting process (grapes) and at the end of the packaging process (bottles). Conversion costs are added evenly throughout each process. The company uses the weighted-average method. Data from the month of March for the Fermenting Department are as follows:

Requirements

- 1. Compute the Fermenting Department’s equivalent units of production for direct materials and for conversion costs.

- 2. Compute the total costs of the units (gallons)

- a. completed and transferred out to the Packaging Department.

- b. in the Fermenting Department ending Work-in-Process Inventory.

Refer to the data and your answers from Exercise El8-23.

Requirements

- 1. Prepare the journal entries to record the assignment of direct materials and direct labor and the allocation of manufacturing

overhead to the Fermenting Department. Assume labor costs are accrued and not yet paid. Also prepare thejournal entry ’to record the cost of the gallons completed and transferred out to the Packaging Department.

- 2.

Post the journal entries to the Work-in-Process Inventory—Fermenting T-account. W hat is the ending balance? - 3. What is the average cost per gallon transferred out of the Fermenting Department into the Packaging Department? Why would Shea Winery’s managers want to know this cost?

Trending nowThis is a popular solution!

Chapter 18 Solutions

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Additional Business Textbook Solutions

Principles of Accounting Volume 2

Auditing and Assurance Services (16th Edition)

Financial Accounting

Horngren's Financial & Managerial Accounting, The Financial Chapters (6th Edition)

Introduction To Managerial Accounting

- Pure Spring Company produces premium bottled water. In the second department, the Bottling Department, conversion costs are incurred evenly throughout the bottling process, but packaging materials are not added until the end of the process. Costs in beginning Work-in-Process Inventory include transferred in costs of $1,700, direct labor of $600, and manufacturing overhead of $900. March data for the Bottling Department follow: View the data. Read the requirements. Requirement 1. Prepare a production cost report for the Bottling Department for the month of March. The company uses the weighted-average method. (Complete all input fields. Enter a "0" for any zero balances. Round all cost per unit amounts to the nearest cent and all other amounts to the nearest whole dollar. Abbreviation used: EUP = equivalent units of production.) UNITS Units to account for: Total units to account for Units accounted for: Total units accounted for Pure Spring Company Production Cost Report - Bottling…arrow_forwardComputing EUP, assigning costs, with beginning WIP, no costs transferred in Shea Winery in Pleasant Valley, New York, has two departments: Fermenting and packaging. Direct materials are added at the beginning of the fermenting process (grapes) and at the end of the packaging process (bottles). Conversion costs are added evenly throughout each process. The company uses the weight-average method. Data from the month of March for the Fermenting Department are as follows: Requirements Compute the Fermenting Departments equivalent units of production for direct materials and for conversion costs. Compute the total costs of the units (gallons) completed and transferred out to the Packaging Department. in the Fermenting Department ending Work-in-Process Inventory.arrow_forwardSelzik Company makes super-premium cake mixes that go through two processing departments-Blending and Packaging. The following activity was recorded in the Blending Department during July: Production data: Units in process, July 1 (materials 100% complete; conversion 30% complete) Units started into production Units in process, July 31 (materials 100% complete; conversion 40% complete) Cost data: Work in process inventory, July 1: Materials cost Conversion cost Cost added during the month: Materials cost Conversion cost All materials are added at the beginning of work in the Blending Department. The company uses the FIFO method in its process costing system. Required: 1. Calculate the Blending Department's equivalent units of production for materials and conversion for July. 2. Calculate the Blending Department's cost per equivalent unit for materials and conversion for July. 3. Calculate the Blending Department's cost of ending work in process inventory for materials, conversion, and…arrow_forward

- Selzik Company makes super-premium cake mixes that go through two processing departments-Blending and Packaging. The following activity was recorded in the Blending Department during July: Production data: Units in process, July 1 (materials 100% complete; conversion 30% complete) Units started into production Units in process, July 31 (materials 100% complete; conversion 40% complete) Cost data: Work in process inventory, July 1: Materials cost Conversion cost Cost added during the month: Materials cost Conversion cost 10,000 170,000 20,000 All materials are added at the beginning of work in the Blending Department. The company uses the FIFO method in its process costing system. $ 8,500 $ 4,900 Required: 1. Calculate the Blending Department's equivalent units of production for materials and conversion for July. 2. Calculate the Blending Department's cost per equivalent unit for materials and conversion for July. 3. Calculate the Blending Department's cost of ending work in process…arrow_forwardSuper Sports Drinks, Inc. has two departments: Mixing and Bottling. Direct materials are added at the beginning of the mixing process and at the end of the bottling process. Conversions costs are added evenly throughout each process. Data for the month of May for the Mixing Department are as follows: Units Amount Beginning Work-in-Process Inventory 0 units Started in production 7,780 units Completed and transferred out to Bottling 4,110 units Ending Work-in-Process Inventory 60% through mixing process 3,670 units Costs Amount Beginning Work-in-Process Inventory $0.00 Costs added during May: Direct Materials $8,531 Direct Labor $2,264 Manufacturing overhead allocated $4,680 Total costs added during May $15,475 Complete the production report for the month of May.(Round your answers to two decimal places when needed and use rounded answers for all future calculations).arrow_forwardDante Carpet Manufacturing Inc. uses a process costing system and calculates per-unit costs using the weighted average method. The company has two sequential production departments, Extrusion and Weaving. The following data relates to production for both departments for its Rayon carpet brand for the month of January. Note that since carpet is sold by the square yard, each “unit" refers to a square yard of carpet: Extrusion department: Beginning Work in Process Inventory: 300 units, 40% complete with respect to conversion Ending Work in Process Inventory: 250 units, 20% complete with respect to conversion Weaving department: Beginning Work in Process Inventory: 200 units, 30% complete with respect to conversion Ending Work in Process Inventory: 400 units, 35% complete with respect to conversion All direct materials are added at the beginning of the extrusion process, and conversion costs are assumed to be incurred uniformly. No new materials are added in the weaving process-just…arrow_forward

- Vaasa Chemicals makes a product by way of two processes – Mixing & Refining. Its processcosting system in the Mixing Department has two direct cost categories (Chemical P &Chemical Q) and one conversion costs pool. Chemical P is introduced at the start of theoperations in the Mixing Department and Chemical Q is added when the product is threefourths (75%) completed in the Mixing Department. The following information pertains to theMixing department for July: Units Work in process inventory, July 1 0 Started production 50,000Completed and transferred to Refining Department 35,000Ending work in process inventory [two-thirds (66⅔%)of the way throughthe Mixing process]…arrow_forwardSuper Sports Drinks, Inc. has two departments: Mixing and Bottling. Direct materials are added at the beginning of the mixing process and at the end of the bottling process. Conversions costs are added evenly throughout each process. Data for the month of May for the Mixing Department are as follows: Units Amount Beginning Work-in-Process Inventory 0 units Started in production 8,150 units Completed and transferred out to Bottling 4,200 units Ending Work-in-Process Inventory 60% through mixing process 3,950 units Costs Amount Beginning Work-in-Process Inventory $0.00 Costs added during May: Direct Materials $8,581 Direct Labor $2,153 Manufacturing overhead allocated $4,470 Total costs added during May $15,204 Complete the production report for the month of May.(Round your answers to two decimal places when needed and use rounded answers for all future calculations).Super Sports Drinks, Inc. Equivalent Units UNITS Whole Units Transferred…arrow_forwardBeverly Plastics produces a part used in precision machining. The part is produced in two departments: Mixing and Refining. The raw material is introduced into the process in the Mixing Department. The cost of the material fluctuates significantly month to month based on market conditions. Information on costs and operations in the Refining Department for September follow: WIP inventory-Refining Beginning inventory (17,500 units, 10% complete with respect to Refining costs) Transferred-in costs (from Mixing) Refining conversion costs Current work (55,300 units started) Mixing costs Refining costs $ 245,055 9,676 $ 906,625 103,140 The ending inventory has 14,800 units, which are 90 percent complete with respect to Refining Department costs. Required: Complete the production cost report using the weighted-average method. Note: Round "Cost per equivalent unit" to 2 decimal places. Flow of units: Units to be accounted for: Beginning WIP inventory Units started this period Total units to…arrow_forward

- Beverly Plastics produces a part used in precision machining. The part is produced in two departments: Mixing and Refining. The raw material is introduced into the process in the Mixing Department. The cost of the material fluctuates significantly month to month based on market conditions. Information on costs and operations in the Refining Department for September follow: WIP inventory-Refining Beginning inventory (17,500 units, 10% complete with respect to Refining costs) Transferred-in costs (from Mixing) Refining conversion costs Current work (55,300 units started) Mixing costs Refining costs The ending inventory has 22,900 units, which are 90 percent complete with respect to Refining Department costs. Required: a. Complete the production cost report using the FIFO method. Note: Round "Cost per equivalent unit" to 2 decimal places. Flow of units: Units to be accounted for. Beginning WIP inventory Units started this period Total units to account for Units accounted for: Completed…arrow_forwardBeverly Plastics produces a part used in precision machining. The part is produced in two departments: Mixing and Refining. The raw material is introduced into the process in the Mixing Department. The cost of the material fluctuates significantly month to month based on market conditions. Information on costs and operations in the Refining Department for September follow: WIP inventory-Refining Beginning inventory (17,500 units, 10% complete with respect to Refining costs) Transferred-in costs (from Mixing) Refining conversion costs Current work (55,300 units started) Mixing costs Refining costs Required: Complete the production cost report using the weighted-average method. Note: Round "Cost per equivalent unit" to 2 decimal places. The ending inventory has 14,700 units, which are 90 percent complete with respect to Refining Department costs. Flow of units: Units to be accounted for: Beginning WIP inventory Units started this period Total units to account for Units accounted for:…arrow_forwardBeverly Plastics produces a part used in precision machining. The part is produced in two departments: Mixing and Refining. The raw material is introduced into the process in the Mixing Department. The cost of the material fluctuates significantly month to month based on market conditions. Information on costs and operations in the Refining Department for September follow: WIP inventory-Refining Beginning inventory (17,500 units, 10% complete with respect to Refining costs) Transferred-in costs (from Mixing) Refining conversion costs Current work (55,300 units started) Mixing costs Refining costs The ending Inventory has 14,200 units, which are 90 percent complete with respect to Refining Department costs. Required: Complete the production cost report using the weighted-average method. Note: Round "Cost per equivalent unit" to 2 decimal places. Flow of units: Units to be accounted for: Beginning WIP inventory Units started this period Total units to account for Units accounted for:…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning