Concept explainers

Videos

Recording and Posting Accrual Basis

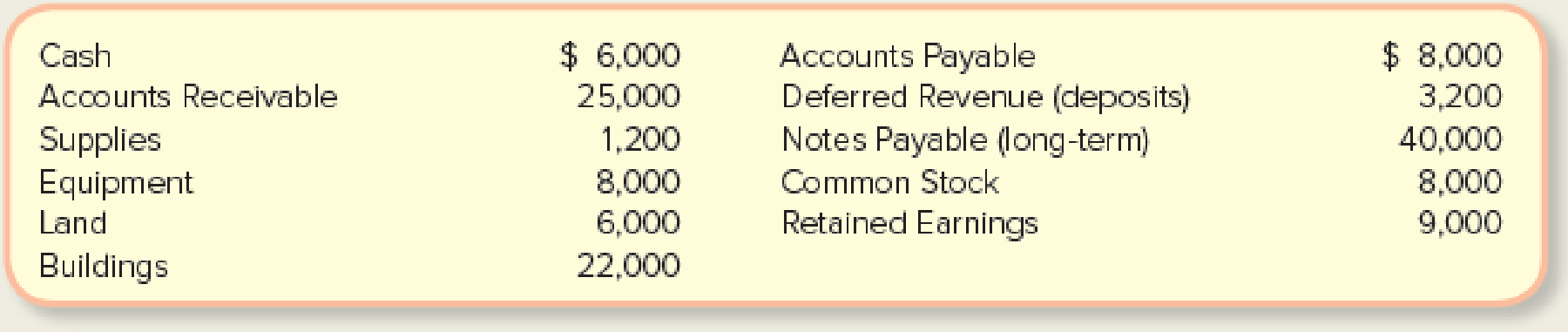

Ricky’s Piano Rebuilding Company has been operating for one year. On January 1, at the start of its second year, its income statement accounts had zero balances and its

Required:

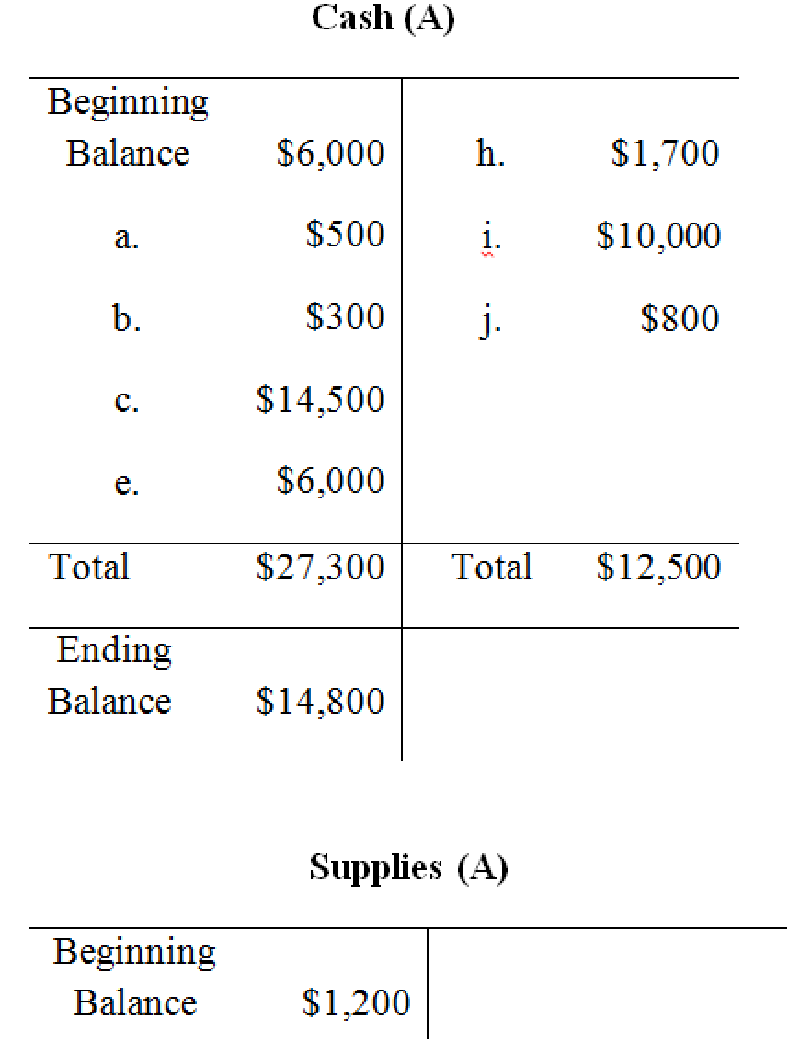

- 1. Create T-accounts for the balance sheet accounts and for these additional accounts: Service Revenue, Rent Revenue, Salaries and Wages Expense, and Utilities Expense. Enter the beginning balances. (If you are using the general ledger tool in Connect, this requirement will be completed for you.)

- 2. Prepare journal entries for the following January transactions, using the letter of each transaction as a reference:

- a. Received a $500 deposit from a customer who wanted her piano rebuilt in February.

- b. Rented a part of the building to a bicycle repair shop; $300 rent received for January.

- c. Delivered five rebuilt pianos to customers who paid $14,500 in cash.

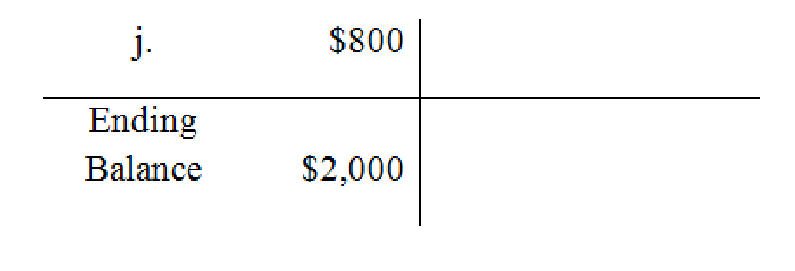

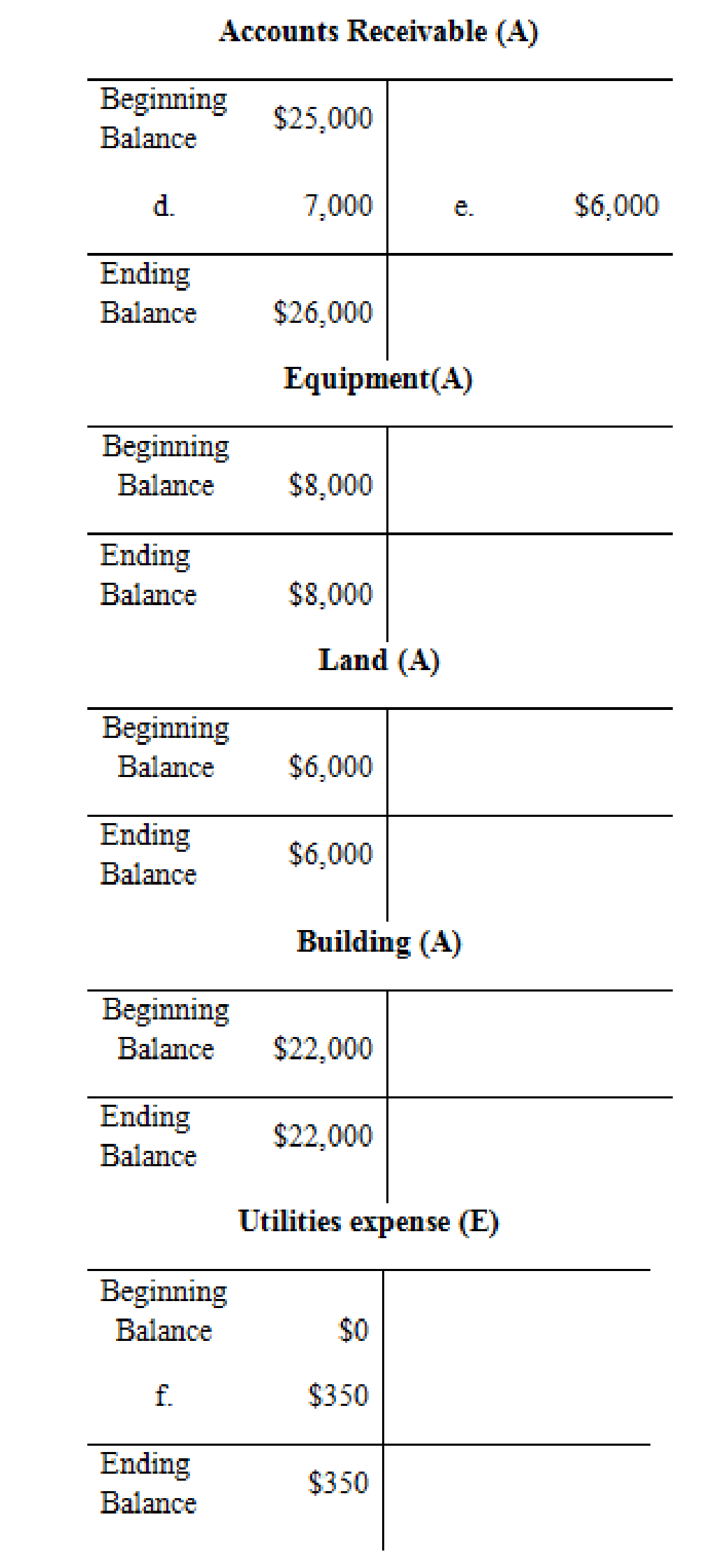

- d. Delivered two rebuilt pianos to customers for $7,000 charged on account.

- e. Received $6,000 from customers as payment on their accounts.

- f. Received an electric and gas utility bill for $350 for January services to be paid in February.

- g. Ordered $800 in supplies.

- h. Paid $1,700 on account in January.

- i. Paid $10,000 in wages to employees in January for work done this month.

- j. Received and paid cash for the supplies in (g).

- 3.

Post the journal entries to the T-accounts. Show the unadjusted ending balances in the T-accounts. (If you are using the general ledger tool, this requirement will be completed for you.) - 4. Use the balances in the completed T-accounts to prepare an unadjusted trial balance at January 31. (If you are using the general ledger tool, this requirement will be completed for you.)

- 5. Using the unadjusted balances, prepare a preliminary income statement and classified balance sheet for the month ended and at January 31

2.

Prepare journal entries for the given transaction.

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Accrual basis of accounting:

In accrual Basis of accounting, the company records all the transaction that brings changes in the financial statement of the company. In accrual basis of accounting, the revenue is recognized for the accounting period, in which the goods are sold, or the service performed even if cash is not exchanged. Similarly the expenses are recognized for the accounting period, in which the business incurred expenses even if cash is not exchanged.

Prepare journal entries for the given transaction as follows:

|

Date | Account Title and Explanation | Debit ($) | Credit ($) | |

| a. | Cash (A+) | 500 | ||

| Deferred Revenue (L+) | 500 | |||

| (To record the cash receipt for the service yet to provide) | ||||

| b. | Cash (A+) | 300 | ||

| Rent Revenue (R+, SE+) | 300 | |||

| (To record the cash receipt from rental area) | ||||

| c. | Cash (A+) | 14,500 | ||

| Service Revenue (R+, SE+) | 14,500 | |||

| (To record the cash received for the service rendered) | ||||

| d. | Accounts Receivable (A+) | 7,000 | ||

| Service Revenue (R+, SE+) | 7,000 | |||

| (To record the service provided to customers on account) | ||||

| e. | Cash (A+) | 6,000 | ||

| Accounts Receivable (A–) | 6,000 | |||

| (To record the cash receipt from customer ) | ||||

| f. | Utilities expense (E+, SE–) | 350 | ||

| Accounts Payable (L+) | 350 | |||

| (To record the payment incurred for utilities expense which are to be paid later) | ||||

| g. | No transaction required | - | ||

| h. | Accounts Payable (L–) | 1,700 | ||

| Cash (A–) | 1,700 | |||

| (To record the payment of cash for the purchases made already) | ||||

| i. | Salaries and Wages Expense (E+, SE–) | 10,000 | ||

| Cash (A–) | 10,000 | |||

| (To record the payment of wages expenses to employees) | ||||

| j. | Supplies (A+) | 800 | ||

| Cash (A–) | 800 | |||

| (To record the purchase of supplies) | ||||

Table (1)

Note:

Item g is not a transaction because there is no cash exchange. Hence it is not recorded in the books of journal.

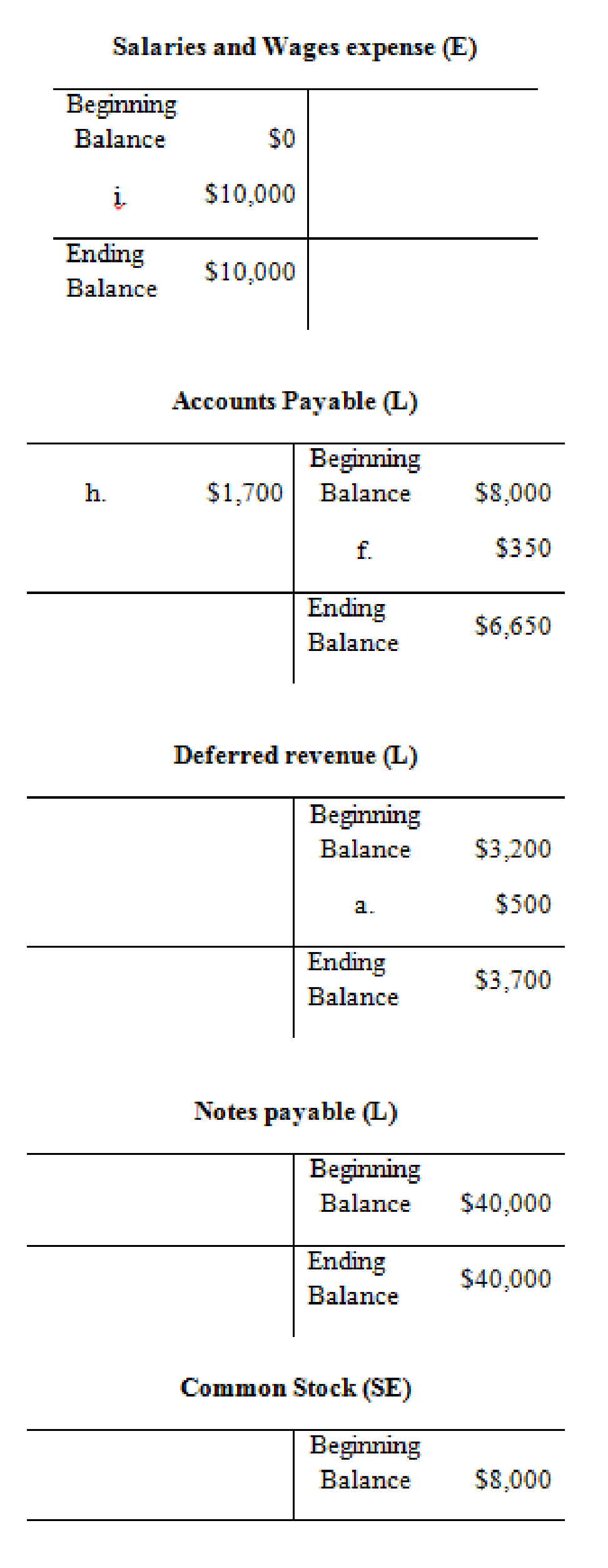

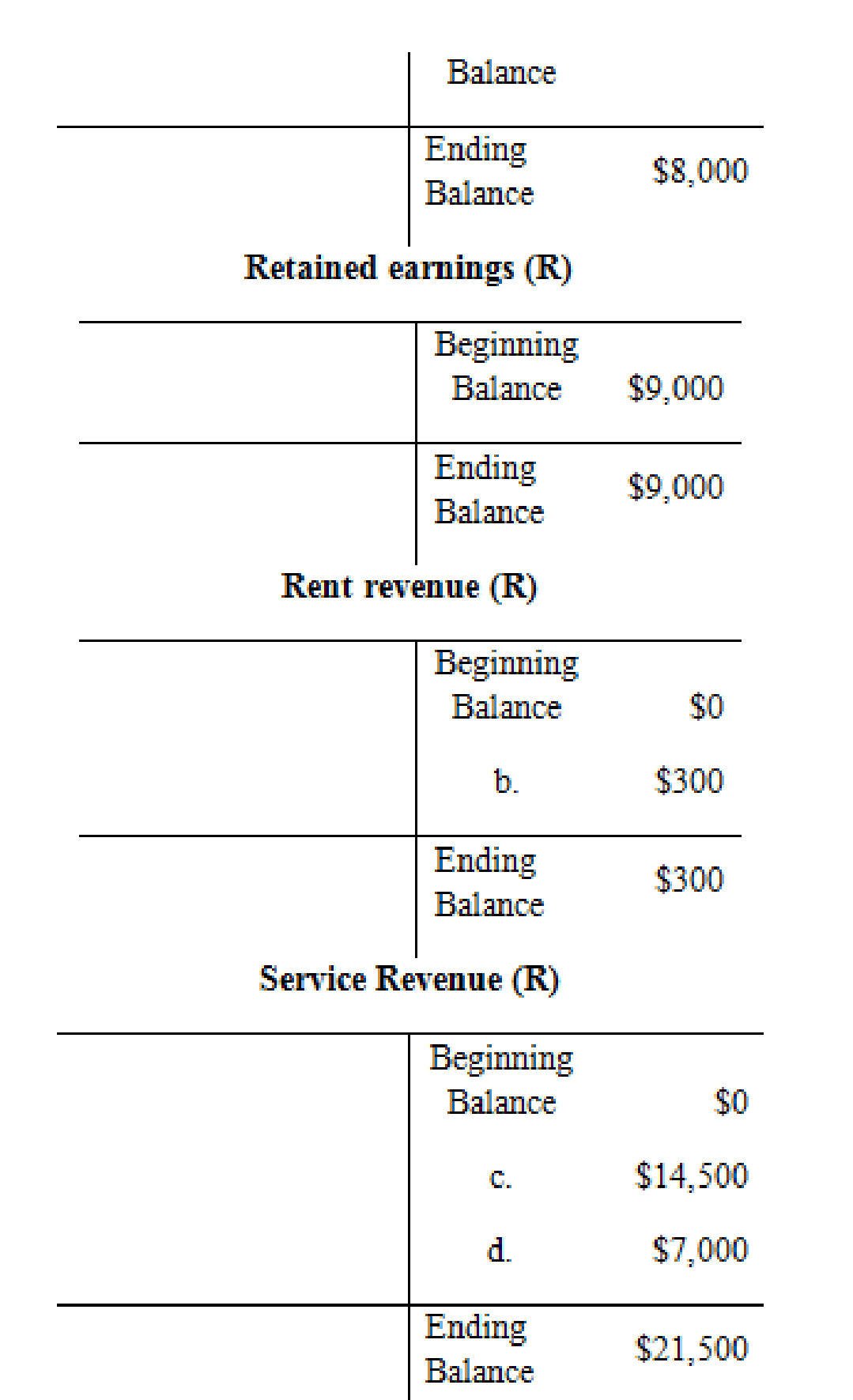

1. and 3.

Prepare the T accounts for the balance sheet accounts and post the journal entries to the T-account, also show the unadjusted ending balance in the T- accounts.

Explanation of Solution

T-account:

An account is referred to as a T-account, because the alignment of the components of the account resembles the capital letter ‘T’. An account consists of the three main components which are as follows:

- The title of the account.

- The left or debit side.

- The right or credit side.

The posting of the journal entries to the T accounts are as follows:

4.

Prepare an unadjusted trial balance at January 31 using the balances in the completed T-accounts.

Explanation of Solution

Unadjusted trial balance:

Unadjusted trial balance is that statement which contains complete list of accounts with their unadjusted balances. This statement is prepared at the end of every financial period.

Prepare an unadjusted trial balance at January 31 as follows:

| Company R | ||

| Unadjusted Trial Balance | ||

| At January 31 | ||

| Particulars | Debit | Credit |

| Cash | $14,800 | |

| Accounts Receivable | 26,000 | |

| Supplies | 2,000 | |

| Equipment | 8,000 | |

| Land | 6,000 | |

| Building | 22,000 | |

| Accounts Payable | $6,650 | |

| Deferred Revenue | 3,700 | |

| Notes Payable | 40,000 | |

| Common Stock | 8,000 | |

| Retained Earnings | 9,000 | |

| Service Revenue | 21,500 | |

| Rent Revenue | 300 | |

| Salaries and Wages Expense | 10,000 | |

| Utilities Expense | 350 | |

| Total | $89,150 | $89,150 |

Table (2)

5.

Prepare a preliminary income statement and classified balance sheet for the month ended January 31.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Classified balance sheet: The main elements of balance sheet assets, liabilities, and stockholders’ equity are categorized or classified further into sections, and sub-sections in a classified balance sheet. Assets are further classified as current assets, long-term investments, property, plant, and equipment (PPE), and intangible assets. Liabilities are classified into two sections current and long-term. Stockholders’ equity comprises of common stock and retained earnings. Thus, the classified balance sheet includes all the elements under different sections.

- Prepare a preliminary income statement for the month ended January 31 as follows:

| Company R | |

| Income Statement | |

| For the Month Ended January 31 | |

| Particulars | $ |

| Revenues: | |

| Service Revenue | $21,500 |

| Rent Revenue | 300 |

| Total Revenues (a) | 21,800 |

| Less: Expenses | |

| Salaries and Wages Expense | 10,000 |

| Utilities Expense | 350 |

| Total Expenses (b) | 10,350 |

| Net Income | $11,450 |

Table (3)

- Prepare the Statement of retained earnings for the month ended January 31 as follows:

| Company R | |

| Statement of Retained Earnings | |

| For the Month Ended January 31 | |

| Particulars | $ |

| Retained Earnings, January 1 | $9,000 |

| Add: Net Income | 11,450 |

| Less: Dividends | 0 |

| Retained Earnings, January 31 | $20,450 |

Table (4)

- Prepare the classified balance at January 31 as follows:

| Company R | |

| Statement of Retained Earnings | |

| For the Month Ended January 31 | |

| Particulars | $ |

| Assets: | |

| Current Assets: | |

| Cash | $14,800 |

| Accounts Receivable | 26,000 |

| Supplies | 2,000 |

| Total Current Assets | 42,800 |

| Equipment | 8,000 |

| Land | 6,000 |

| Building | 22,000 |

| Total Assets | $78,800 |

| Liabilities: | |

| Current Liabilities | |

| Accounts Payable | $6,650 |

| Deferred Revenue | 3,700 |

| Total Current Liabilities | 10,350 |

| Notes Payable (long-term) | 40,000 |

| Total Liabilities (a) | 50,350 |

| Stockholders’ Equity: | |

| Common Stock | 8,000 |

| Retained Earnings | 20,450 |

| Total Stockholders’ Equity (b) | 28,450 |

| Total Liabilities and Stockholders’ Equity | $78,800 |

Table (5)

Want to see more full solutions like this?

Chapter 3 Solutions

Fundamentals Of Financial Accounting

- On June 1 , Michelob signed up and paid $1,200 to Master Brewer Inc. for a 6 monthbrewing course that started on the same date. As of July 31st, Master Brewer'saccounting records would indicate: $400 of revenue, $800 of accounts receivable $400 of revenue, $800 of deferred revenue $1,200 of revenue, $1,200 of cash $800 of revenue, $400 of accounts receivablearrow_forwardYour calendar year company completes a $6,000 job, of which $1,000 has been received by year end and credited to Revenue. If you discover before the books are closed that no adjusting entry was made, your correcting entry will: debit Accounts Receivable for $6,000 credit Revenue for $5,000 credit Accounts Receivable for $5,000 debit Revenue for $5,000arrow_forwardPrepare journal entries for each transaction listed.a. At the end of June, bad debt expense is estimated to be $14,000.b. In July, customer balances are written off in the amount of $7,000.arrow_forward

- Rosie Dry Cleaning was started on January 1, Year 1. It experienced the following events during its first two years of operation: Events Affecting Year 1 Provided $32, 680 of cleaning services on account. Collected $26, 144 cash from accounts receivable. Adjusted the accounting records to reflect the estimate that uncollectible accounts expense would be 1 percent of the cleaning revenue on account. Events Affecting Year 2 Wrote off a $245 account receivable that was determined to be uncollectible. Provided $38, 138 of cleaning services on account. Collected $33, 752 cash from accounts receivable. Adjusted the accounting records to reflect the estimate that uncollectible accounts expense would be 1 percent of the cleaning revenue on account. Required: Organize the transaction data in accounts under an accounting equation for each year. Determine the following amounts: (1) Net income for Year 1. (2) Net cash flow from operating activities for Year 1. (3) Balance of accounts receivable at…arrow_forwardSuppose a customer rents a vehicle for three months from Franklin Rental on November 1, paying $3,750 ($1,250/month). Required: 1.&2. Record the necessary entries in the Journal Entry Worksheet below. 3. Calculate the year-end adjusted balances of Deferred Revenue and Service Revenue (assuming the balance of Deferred Revenue at the beginning of the year is $0).arrow_forwardOn November 1, Year 1, a company borrows $49,000 cash from Community Savings and Loan. The company signs a three-month, 6% note payable. Interest is payable at maturity. The company's year-end is December 31. Required: 1.-3. Record the necessary entries in the Journal Entry Worksheet below. (If no entry is required for a particular transaction/event, select "No Journal Entry Required" in the first account field.) View transaction list View journal entry worksheet No Date General Journal Debit Credit 1 November 01 Cash 49,000 Notes Payable 49,000 2 December 31 Interest Expense 490 Interest Payable 490 3 February 01 Notes Payable 49,000 Interest Payable 735 Cash 49,735 :......:arrow_forward

- On November 1, Year 1, a company borrows $49,000 cash from Community Savings and Loan. The company signs a three-month, 6% note payable. Interest is payable at maturity. The company's year-end is December 31. Required: 1.-3. Record the necessary entries in the Journal Entry Worksheet below. (If no entry is required for a particular transaction/event, select "No Journal Entry Required" in the first account field.) View transaction list Journal entry worksheet Record the repayment of the note at maturity. Note: Enter debits before credits. Date General Journal Debit Credit February 01arrow_forwardOn November 1, Year 1, a company borrows $49,000 cash from Community Savings and Loan. The company signs a three-month, 6% note payable. Interest is payable at maturity. The company's year-end is December 31. Required: 1.-3. Record the necessary entries in the Journal Entry Worksheet below. (If no entry is required for a particular transaction/event, select "No Journal Entry Required" in the first account field.) View transaction list Journal entry worksheet 1 > Record the issuance of note. Note: Enter debits before credits. Date General Journal Debit Credit November 01arrow_forwardState assumptions and answer accordingly. Assume December 31st year-end, unless otherwise stated. Assume all amounts are normal balances, unless otherwise stated. Jp holdings ending trial balance from july 31, 2000 is below. You were hired as the accountant on august 1 and your task is to complete the accounting cycle for the year end of august 30. The company prepares adjusting journal entries monthly, which means the adjusting entries for july were prepared properly by the former accountant. Debit Credit Cash $ 8,660 Accounts receivable 7,440 Supplies 1,600 Equipment Accumulated depreciation- equipment 30,000 $ 3,000 Accounts payable 6,200 Salaries payable 1,400 Unearned revenue 800 Common shares 20,000 Retained earnings 16,300 $47,700 $47.700 During July, the following transactions were completed: Paid employees $2,200 for salaries due, of which $1,400 was for july salaries payable and $800 for august. June. 6 Received $5,400 cash from customers in payment of accounts. 11 Received…arrow_forward

- On November 1, Year 1, a company borrows $47,000 cash from Community Savings and Loan. The company signs a three-month, 6% note payable. Interest is payable at maturity. The company’s year-end is December 31. 1.-3. Record the necessary entries in the Journal Entry Worksheet below. (If no entry is required for a particular transaction/event, select "No Journal Entry Required" in the first account field.)arrow_forwardPreparing and Analyzing Closing Entries At December 31, the ledger of Aulani Company includes the following accounts, all having normal balances: Sales Revenue, $59,800; Cost of Goods Sold, $31,400; Retained Earnings, $20,000; Interest Expense, $3,200; Dividends (declared and paid), $5,000; Wages Expense, $8,000, and Interest Payable, $2,100. Required: Prepare the closing entries for Aulani at December 31. If an amount box does not require an entry, leave it blank. How does the closing process affect Aulani's retained earnings?arrow_forwardprepare these entries for Sarah's plant services. prepare general journal entries for the needed balance dy adjustments for the year ending 30/6/21: A stocktake of the inventory on hand was completed on 30/6/21. The value of the stocktake was $17,000. The inventory asset account as at 30/6/21 before adjustments was $18,000 The allowance for Doubtful debts should be 5% of the balance of Accounts Receivable. The accounts receivable balance at 30/6/21 is $76,120 and the balance of the Allowance for Doubtful Debts was $3,450arrow_forward

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage