Concept explainers

Videos

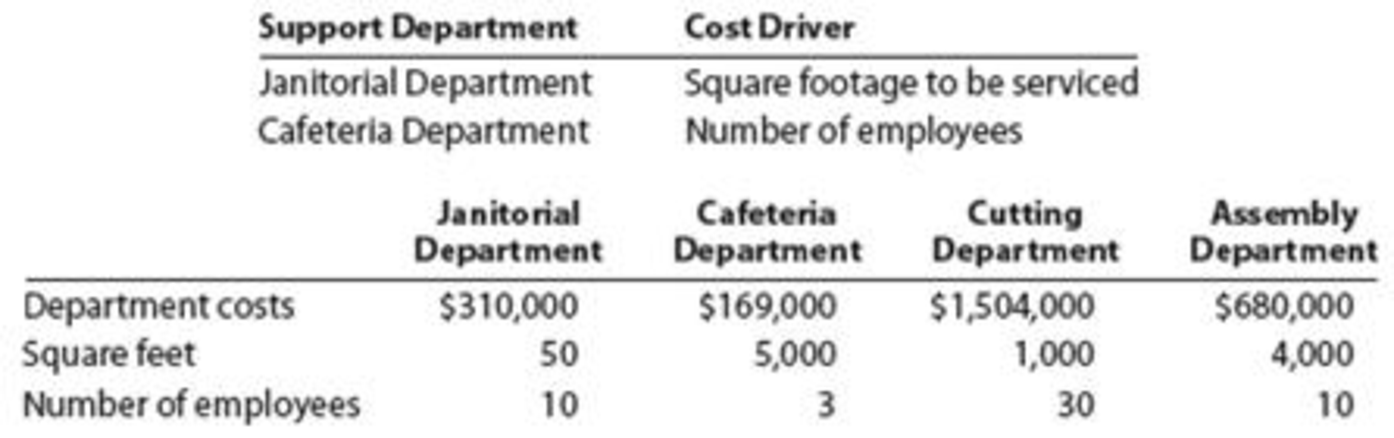

Support department cost allocation —comparison

Refer to your answers to Exercises 7-9. Compare the total support department costs allocated to each production department under each cost allocation method. Which production department is allocated the most support department costs (a) under the direct method, (b) under the sequential method, and (c) under the reciprocal services method?

EX 19-7 Support department cost allocation—direct method

Becker Tabletops has two support departments (Janitorial and Cafeteria) and two production departments (Cutting and Assembly). Relevant details for these departments are as follows:

Allocate the support department costs to the production departments using the direct method.

EX 19-8 Support department cost allocation—sequential method

Refer to the information provided for Becker Tabletops in Exercise 7. Allocate the support department costs to the production departments using the sequential method. Allocate the support department with the highest department cost first.

EX 19-9 Support department cost allocation —reciprocal services method

Refer to the information provided for Becker Tabletops in Exercise 7. Allocate the support department costs to the production departments using the reciprocal services method.

Identify the production department with greater department cost allocation under each method.

Explanation of Solution

Cost allocation:

The cost allocation refers to the process of allocating the costs associated with the production of the products mainly indirectly and are generally ignored. The main objective of cost allocation is to ensure proper pricing of the products. This can be done by several methods.

(a) The direct method:

Compute the costs allocated from the support departments.

Cutting Department Total Cost:

Assembly Department Total Cost:

Under the direct method the Assembly department has been allocated the greater costs from the support departments.

Working Notes:

Janitorial Department Cost Allocation:

Compute the allocation of costs from Janitorial Department to Cutting Department:

The costs from Janitorial Department that should be allocated to Cutting department is $62,000.

Compute the allocation of costs from Janitorial Department to Assembly Department:

The cost allocated from Janitorial Department to Assembly department is $248,000.

Cafeteria Department Cost Allocation:

Compute the allocation of costs from Cafeteria Department to Cutting Department:

The costs allocated from Cafeteria Department to Cutting department is $126,750.

Compute the allocation of costs from Cafeteria Department to Assembly Department:

The cost allocated from Cafeteria Department to Assembly department is $42,250.

(b) The sequential method:

Compute the costs allocated from the support departments.

Cutting Department Total Cost:

Assembly Department Total Cost:

Under the sequential method the Cutting department has been allocated the greater costs from the support departments.

Working Notes:

Janitorial Department Cost Allocation:

Compute the allocation of costs from Janitorial Department to Cafeteria Department:

The cost allocated from Janitorial Department to Cafeteria department is $155,000.

Compute the allocation of costs from Janitorial Department to Cutting Department:

The costs allocated from Janitorial Department to Cutting department is $31,000.

Compute the allocation of costs from Janitorial Department to Assembly Department:

The cost allocated from Janitorial Department to Assembly department is $124,000.

Cafeteria Department Total Cost:

The total costs of Cafeteria Department are $324,000.

Compute the allocation of costs from Cafeteria Department to Cutting Department:

The costs allocated from Cafeteria Department to Cutting department is $243,000.

Compute the allocation of costs from Cafeteria Department to Assembly Department:

The cost allocated from Cafeteria Department to Assembly department is $81,000.

(c) The reciprocal services method:

Compute the costs allocated from the support departments.

Cutting Department Total Cost:

Assembly Department Total Cost:

Under the reciprocal services method the Cutting department has been allocated the greater costs from the support departments.

Working Notes:

Janitorial Department Cost to be allocated:

The total Janitorial Department costs include 20% of the Cafeteria department costs as,

Therefore, the Cafeteria Department cost is,

Cafeteria Department Cost to be allocated:

The total Cafeteria Department costs include 50% of the Janitorial department costs as,

Therefore, the Cafeteria Department cost is,

Substitute the equation for J into the C equation:

Substitute the value of C into the J equation:

Janitorial Department Cost Allocation:

Compute the allocation of costs from Janitorial Department to Cafeteria Department:

The cost allocated from Janitorial Department to Cafeteria Department is $191,000.

Compute the allocation of costs from Janitorial Department to Cutting Department:

The cost allocated from Janitorial Department to Cutting Department is $38,200.

Compute the allocation of costs from Janitorial Department to Assembly Department:

The cost allocated from Janitorial Department to Assembly Department is $152,800.

Cafeteria Department Cost Allocation:

Compute the allocation of costs from Cafeteria Department to Janitorial Department:

The cost allocated from Cafeteria Department to Janitorial Department is $72,000.

Compute the allocation of costs from Cafeteria Department to Cutting Department:

The cost allocated from Cafeteria Department to Cutting Department is $216,000.

Compute the allocation of costs from Cafeteria Department to Assembly Department:

The cost allocated from Cafeteria Department to Assembly Department is $72,000.

Want to see more full solutions like this?

Chapter 5 Solutions

Managerial Accounting

- Refer to Cornerstone Exercise 7.3. Now assume that Valron Company uses the sequential method to allocate support department costs. The support departments are ranked in order of highest cost to lowest cost. Required: 1. Calculate the allocation ratios (rounded to four significant digits) for the four departments using the sequential method. 2. Using the sequential method, allocate the costs of the Human Resources and General Factory departments to the Fabricating and Assembly departments. (Round all allocated costs to the nearest dollar.) 3. What if the allocation ratios in Requirement 1 were rounded to six significant digits rather than four? How would that affect any rounding error in the allocation of costs?arrow_forward(Appendix 4B) Sequential Method of Support Department Cost Allocation Refer to Exercise 4-51 for data. Now assume that Stevenson uses the sequential method to allocate support department costs to the operating divisions. General Factory is allocated first in the sequential method for the company. Required: 1. Calculate the allocation ratios for Power and General Factory. (Note: Carry these calculations out to four decimal places.) 2. Allocate the support service costs to the operating divisions. (Note: Round all amounts to the nearest dollar.) 3. Assume divisional overhead rates are based on direct labor hours. Calculate the overhead rate for the Battery Division and for the Small Motors Division. (Note: Round overhead rates to the nearest cent.)arrow_forwardDistribution of service department costs to production departments using the sequential distribution method Required: Using the information in P4-6, prepare a schedule showing the distribution of the service departments’ expenses using the sequential distribution method in the order of number of other departments served. (Hint: First distribute the service department that services the greater number of other departments.)arrow_forward

- Comprehensive support department allocationsManagement at C. Pier Press has decided to allocate costs of the paper’s two support departments (administration and human resources) to the two revenue-generating departments (advertising and circulation). Administration costs are to be allocated on the basis of dollars of assets employed; human resources costs are to be allocated on the basis of number of employees. The following costs and allocation bases are available: Department Direct Costs Number of Employees Assets Employed Administration $1,094,100 14 $541,940 Human resources 689,780 11 408,380 Advertising 1,340,920 17 1,067,360 Circulation 1,893,640 36 2,618,420 Totals $5,018,440 78 $4,636,100 c. Assuming that the benefits-provided ranking is the order shown in the table, use the step method to allocate the support department costs to the revenue-generating departments.Note: Round your final answers only to the nearest whole dollar. Amount allocated…arrow_forwardComprehensive support department allocationsManagement at C. Pier Press has decided to allocate costs of the paper’s two support departments (administration and human resources) to the two revenue-generating departments (advertising and circulation). Administration costs are to be allocated on the basis of dollars of assets employed; human resources costs are to be allocated on the basis of number of employees. The following costs and allocation bases are available: Department Direct Costs Number of Employees Assets Employed Administration $1,094,100 14 $541,940 Human resources 689,780 11 408,380 Advertising 1,340,920 17 1,067,360 Circulation 1,893,640 36 2,618,420 Totals $5,018,440 78 $4,636,100 e. Using the algebraic method, allocate the support department costs to the revenue-generating departments. Note: Round percentages in your calculation to the nearest whole percent (for example, round 34.5% to 35%). Note: Round your final answer to the nearest…arrow_forwardComprehensive support department allocationsManagement at C. Pier Press has decided to allocate costs of the paper’s two support departments (administration and human resources) to the two revenue-generating departments (advertising and circulation). Administration costs are to be allocated on the basis of dollars of assets employed; human resources costs are to be allocated on the basis of number of employees. The following costs and allocation bases are available: Department Direct Costs Number of Employees Assets Employed Administration $1,094,100 14 $541,940 Human resources 689,780 11 408,380 Advertising 1,340,920 17 1,067,360 Circulation 1,893,640 36 2,618,420 Totals $5,018,440 78 $4,636,100 c. Assuming that the benefits-provided ranking is the order shown in the table, use the step method to allocate the support department costs to the revenue-generating departments.Note: Round your final answers only to the nearest whole dollar. Amount…arrow_forward

- Comprehensive support department allocations Management at C. Pier Press has decided to allocate costs of the paper’s two support departments (administration and human resources) to the two revenue-generating departments (advertising and circulation). Administration costs are to be allocated on the basis of dollars of assets employed; human resources costs are to be allocated on the basis of number of employees. The following costs and allocation bases are available: Department Direct Costs Number of Employees Assets Employed Administration $390,750 5 $193,550 Human resources 246,350 4 145,850 Advertising 478,900 6 381,200 Circulation 676,300 13 935,150 Totals $1,792,300 28 $1,655,750 a. Using the direct method, allocate the support department costs to the revenue-generating departments.Note: Round percentages in your calculation to the nearest whole percent (for example, round 34.5% to 35%).Note: Round your final answer to the nearest whole dollar.Total…arrow_forwardQuestion Content Area Miller Safety Equipment uses multiple production department rates to apply overhead to products. The company will allocate support department costs to production departments based on the amount of support activity a. used by the entire production facility b. used by the department in the prior month c. budgeted by the department d. used by the departmentarrow_forwardRefer to the data in Exercise 7.22. The support departments are ranked in order of highest cost to lowest cost. Required: 1. Allocate the costs of the support departments using the sequential method. (Round allocation ratios to four significant digits. Round allocated costs to the nearest dollar.) 2. Using direct labor hours, compute departmental overhead rates. (Round to the nearest cent.)arrow_forward

- Refer to the data in Exercise 7.22. The company has decided to simplify its method of allocating support service costs by switching to the direct method. Required: 1. Allocate the costs of the support departments to the producing departments using the direct method. (Round allocation ratios to four significant digits. Round allocated costs to the nearest dollar.) 2. Using direct labor hours, compute departmental overhead rates. (Round to the nearest cent.)arrow_forwardRefer to Cornerstone Exercise 7.3. Now assume that Valron Company uses the reciprocal method to allocate support department costs. Required: 1. Calculate the allocation ratios (rounded to four significant digits) for the four departments using the reciprocal method. 2. Develop a simultaneous equations system of total costs for the support departments. Solve for the total reciprocated costs of each support department. (Round reciprocated total costs to the nearest dollar.) 3. Using the reciprocal method, allocate the costs of the Human Resources and General Factory departments to the Fabricating and Assembly departments. (Round all allocated costs to the nearest dollar.) 4. What if the square footage in Fabricating were 13,300 and the square footage in Assembly were 5,700. How would that affect the allocation of support department costs?arrow_forwardFIFO Method, Single Department Analysis, One Cost Category Refer to the data in Problem 6.33. Required: Prepare a cost of production report for the Fabrication Department for December using the FIFO method of costing.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning