Concept explainers

Videos

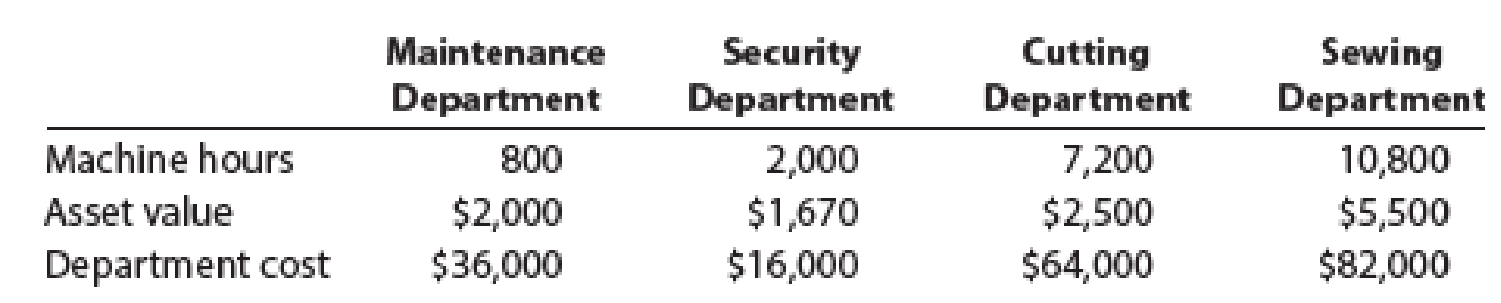

Davis Snowflake & Co. produces Christmas stockings in its Cutting and Sewing departments. The Maintenance and Security departments support the production of the stockings. Costs from the Maintenance Department are allocated based on machine hours, and costs from the Security Department are allocated based on asset value. Information about each department is provided in the following table:

Determine the total cost of each production department after allocating all support department costs to the production departments using the reciprocal services method.

Compute the total cost of each production department after allocating all support costs to the production departments.

Explanation of Solution

Cost allocation:

The cost allocation refers to the process of allocating the costs associated with the production of the products mainly indirectly and are generally ignored. The main objective of cost allocation is to ensure proper pricing of the products. This can be done by several methods.

Maintenance Department Cost to be allocated:

The total Maintenance Department costs include 20% of the Security department costs as,

Therefore, the Security Department cost is,

Security Department Cost to be allocated:

The total Security Department costs include 10% of the Maintenance department costs as,

Therefore, the Security Department cost is,

Substitute the equation for M into the S equation:

Substitute the value of S into the M equation:

Maintenance Department Cost Allocation:

Compute the allocation of costs from Maintenance Department to Security Department:

The costs allocated from Maintenance Department to Security Department is $4,000.

Compute the allocation of costs from Maintenance Department to Cutting Department:

The costs allocated from Maintenance Department to Cutting Department is $14,400.

Compute the allocation of costs from Maintenance Department to Sewing Department:

The costs allocated from Maintenance Department to Sewing Department is $21,600.

Security Department Cost Allocation:

Compute the allocation of costs from Security Department to Maintenance Department:

The costs allocated from Security Department to Maintenance Department is $4,000.

Compute the allocation of costs from Security Department to Cutting Department:

The costs allocated from Security Department to Cutting Department is $5,000.

Compute the allocation of costs from Security Department to Sewing Department:

The costs allocated from Security Department to Sewing Department is $11,000.

Total Costs of Production Departments:

Compute the total cost of the Cutting Department:

The total costs of the Cutting department are $83,400.

Compute the total cost of the Sewing Department:

The total costs of the Sewing department are $114,600.

Want to see more full solutions like this?

Chapter 5 Solutions

Managerial Accounting

- A manufacturing company has two service and two production departments. Human Resources and Machine Repair are the service departments. The production departments are Grinding and Polishing. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The human resources department services all departments of the company, and its costs are allocated using the numbers of employees within each department, while machine repair costs are allocable to Grinding and Polishing on the basis of machine hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardA manufacturing company has two service and two production departments. Building Maintenance and Factory Office are the service departments. The production departments are Assembly and Machining. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The building maintenance department services all departments of the company, and its costs are allocated using floor space occupied, while factory office costs are allocable to Assembly and Machining on the basis of direct labor hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardVirgin River Inc. produces horse and rancher equipment. Costs from Support Department 1 are allocated based on the number of employees. Costs from Support Department 2 are allocated based on asset value. Relevant department information is provided in the following table. Using the sequential method of support department cost allocation, determine the total costs from Support Department 1 (assuming they are allocated first) that should be allocated to Support Department 2 and to each of the production departments. Support Department 1 Department 2 Support Production Production Department 1 Department 2 Number of employees 9. 7 25 18 Asset value $1,150 $670 $6,230 $5,100 Department cost $20,000 $15,500 $99,000 $79,000arrow_forward

- Snowy River Stallion Inc. produces horse and rancher equipment. Costs from Support Department 1 are allocated based on the number of employees. Costs from Support Department 2 are allocated based on asset value. Relevant department information is provided in the following table: Using the sequential method of support department cost allocation, determine the total costs from Support Department 1 (assuming they are allocated first) that should be allocated to Support Department 2 and to each of the production departments.arrow_forwardSupport department cost allocation-reciprocal services method Temple Lights, Inc. produces Hanukkah menorahs in its Cutting and Molding departments. The Maintenance and Security departments support the production of the menorahs. Costs from the Maintenance Department are allocated based on machine hours, and costs from the Security Department are allocated based on asset value. Information about each department is provided in the following table: Maintenance Machine hours Asset value Department cost Department Security Department Cutting Department Molding Department 800 2,000 7,200 10,800 $2,000 $36,000 $1,670 $2,500 $5,500 $16,000 $64,000 $82,000 Determine the total cost of each production department after allocating all support department costs to the production departments using the reciprocal services method. Cutting Molding Department Department Production departments' total costs 4arrow_forwardAI Rawabi company consist of two support departments (Administration and R& D) and two operating departments (Manufacturing & Assembling). The cost of Administration department is allocated based on number of employees and the cost of R& D department is allocated based on research hours. The table below shows the cost details. Allocate the cost of the support departments to the operating departments using step-down method. How much is the Assembling department total cost after cost allocation: Support Departments Operating Departments R&D Manufacturing Assembling Total Cost Admin Cost: Salaries 30000 60000 44000 70000 204000 Supplies 10000 30000 25000 30000 95000 Total 40000 90000 69000 100000 299000 Allocation Base: Research Hours 200 300 450 250 Number of Employees 7 10 9 13 Select one: O a. RO 155775 O b. RO 162090.3 O c. RO 143225 O d. 136909.7arrow_forward

- Trek, Inc. has two service departments (Human Resources and Building Maintenance) and two production departments (Machining and Assembly). The company allocates Building Maintenance cost on the basis of square footage and believes that Building Maintenance provides more service than Human Resources. The square footage occupied by each department follows. Human Resources Building Maintenance. Machining Assembly Assuming use of the direct method, over how many square feet would the Building Maintenance cost be allocated (i.e., spread)? Multiple Choice O 18,000. 66,000. 48,000. 7,000 11,000 20,000 28,000 More information is needed to judge. 55,000.arrow_forwardPrism Company has two service departments: security departments and maintenance departments that give services to two producing departments: machining department and assembling department. Security department costs will be allocated using the number of employees and maintenance department costs will be allocated using direct labor hours. For calculation of predetermined rate, machine hours and direct labor hours are used for machining and assembling departments, respectively.arrow_forwardThe Woodridge Manufacturing Company has two Production Departments: Cutting and Pasting. Each of these two departments uses the services provided by the Computing and Maintenance Departments, which both support the production functions and each other’s functions as well. Woodridge uses the step method of allocating these service department costs to the production departments. Computing is allocated on the basis of hours of department operations and Maintenance is allocated on the basis of departmental direct labor hours. Last period the following costs were recorded: Cutting Department overhead $400,000 Pasting Department overhead $600,000 Computing Department total costs $700,000 Maintenance Department total costs $300,000 Production Department data: Cutting Pasting Computing Maintenance Hours of operation 5,000 7,500 15,000 2,500 Direct labor hours recorded 4,000 8,000 4,000 8,000 Required: a. Determine the…arrow_forward

- 2. Assume that Kizzle's management allocates Maintenance costs based on the number of service calls. Further assume that in a given period, the Janitorial, Mixing, and Cooking activities incur 16, 40, and 24 service calls, respectively, and that the Janitorial and Maintenance costs of that period are $3,000 and $4,200, respectively. Determine the total costs allocated from each support activity to the other three activities using the reciprocal services method. Malntenance cost allocation: Janitorial: Mixing: $4 Cooking: Janitorial cost allocation: Maintenance: Mixing: Cooking: 3. The company is considering changing from the reciprocal service method to a simpler method. Why should the company continue with the reciprocal service method? a. It is complex, but more accurate. b. It can be practiced if the company has sufficient resources and capacity. C. The simpler cost allocation methods are less accurate. d. All the above.arrow_forwardSupport Department Cost Allocation-Reciprocal Services Method Brewster Toymakers Inc. produces toys for children. The toys are produced in the Molding and Assembly departments, The Janitorial and Security departments support the production of the toys. Costs from the Janitorial Department are allocated based on square feet. Costs from the Security Department are allocated based on asset value. Relevant department information is provided in the following table: Janitorial Department Security Department Molding Department Assembly Department Square feet 650 1,600 1,600 4,800 Asset value $100 $120 $900 $1,000 Department cost $2,000 $1,500 $10,900 $12,100 < Using the reciprocal services method of support department cost allocation, determine: a. The percentage of Janitorial costs that should be allocated to the Security Department. % b. The percentage of Security costs that should be allocated to the Janitorial Department. %arrow_forwardHugo, owner of Automated Fabric, Inc., is interested in using the reciprocal allocation method. The following data from operations were collected for analysis: Budgeted manufacturing overhead costs: M (Support Dept) P (Support Dept) W (Weaving Dept) C (Colorizing Dept) Maintenance Personnel Weaving Colorizing Services furnished: By Maintenance (budgeted labor-hours): to Personnel to Weaving to Colorizing By Personnel (Number of employees serviced): Plant Maintenance Weaving Colorizing Which of the following linear equations represents the complete reciprocated cost of the Personnel Department? A. P= $200,000 B. P = (1,100/ 13,700) M C. P= $200,000+ (1,100/ 13,700) M D. P= $330,000 $200,000 (1,100/ 13,700) M *** $330,000 $200,000 $660,000 $440,000 1,100 7,600 5,000 9 39 25arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning