Videos

Support activity cost allocation

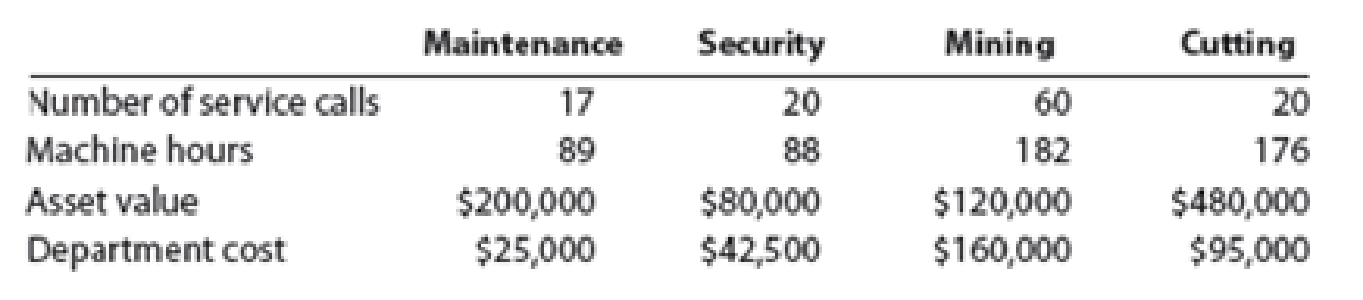

Jake’s Gems mines and produces diamonds, rubies, and other gems. The gems are produced by way of the Mining and Cutting activities. These production activities are supported by the Maintenance and Security activities. Security costs are allocated to the production activities based on asset value. Maintenance costs are normally allocated based on machine hours. However, Maintenance costs typically correlate more with the number of service calls. Information regarding the activities is provided in the following table:

Instructions

1. Should Maintenance costs continue to be allocated based on machine hours? Why would a different driver be more appropriate?

2. Based on your response to part (1), determine the total costs allocated from each support activity to the other activities using the reciprocal services method and the most appropriate cost driver for Maintenance.

3. Jake’s Gems is considering cutting costs by switching to a simpler support activity cost allocation method. Using the information provided and given your response to part (2), determine if switching to the direct method would significantly alter the production activity costs.

a.

Identify the cost driver to allocate maintenance costs and whether or not to use the machine hours as the cost driver.

Explanation of Solution

Cost Driver: The cost driver refers to the all the activities on which the money is spent to produce the product or the service. It has a cause-effect relationship with the resources utilized in production. The cost drivers are used to form the activity cost pools.

The support department costs in the production are the indirect costs that difficult to identify and be associated to the concerned cost drivers. Hence, it is difficult to apply support department costs to the products.

Machine hours are not an accurate cost driver and must not be used. Service calls must be used as it a more appropriate cost driver as maintenance department is associated more with the service calls rather than the machine hours.

b.

Compute the total cost of each production department after allocating all support costs to the production departments using the cost driver chosen in part a.

Explanation of Solution

Maintenance Department Cost to be allocated:

The total Maintenance Department costs include 25% of the Security department costs as,

Therefore, the Security Department cost is,

Security Department Cost to be allocated:

The total Security Department costs include 20% of the Maintenance department costs as,

Therefore, the Security Department cost is,

Substitute the equation for M into the S equation:

Substitute the value of S into the M equation:

Maintenance Department Cost Allocation:

Compute the allocation of costs from Maintenance Department to Security Department:

The cost allocated from Maintenance Department to Security Department is $7,500.

Compute the allocation of costs from Maintenance Department to Cutting Department:

The cost allocated from Maintenance Department to Cutting Department is $7,500.

Compute the allocation of costs from Maintenance Department to Mining Department:

The cost allocated from Maintenance Department to Mining Department is $22,500.

Security Department Cost Allocation:

Compute the allocation of costs from Security Department to Maintenance Department:

The cost allocated from Security Department to Maintenance Department is $12,500.

Compute the allocation of costs from Security Department to Cutting Department:

The cost allocated from Security Department to Cutting Department is $30,000.

Compute the allocation of costs from Security Department to Mining Department:

The cost allocated from Security Department to Mining Department is $7,500.

Total Costs of Production Departments:

Compute the total cost of the Cutting Department:

The total costs of the Cutting department are $132,500.

Compute the total cost of the Mining Department:

The total costs of the Pruning department are $190,000.

c.

Identify the impact on the costs if company switches to simpler cost allocation method than the one used in part (b).

Explanation of Solution

Maintenance Department Cost Allocation:

Compute the allocation of costs from Maintenance Department to Cutting Department:

The cost from Maintenance Department that should be allocated to Cutting department is $6,250.

Compute the allocation of costs from Maintenance Department to Mining Department:

The cost allocated from Maintenance Department to Pruning department is $18,750.

Security Department Cost Allocation:

Compute the allocation of costs from Security Department to Cutting Department:

The cost allocated from Security Department to Cutting department is $34,000.

Compute the allocation of costs from Security Department to Pruning Department:

The cost allocated from Security Department to Pruning department is $8,500.

Total Costs of Production Departments:

Compute the total cost of the Cutting Department:

The total costs of the Cutting department are $135,250.

Compute the total cost of the Mining Department:

The total costs of the Pruning department are $187,250.

The switch from the existing method to the direct method would ensure the reduction of cost also there is a very little change in the costs being allocated amongst the two methods.

Want to see more full solutions like this?

Chapter 5 Solutions

Managerial Accounting

- Support activity cost allocation Jake’s Gems mines and produces diamonds, rubies, and other gems. The gems are produced by way of the Mining and Cutting activities. These production activities are supported by the Maintenance and Security activities. Security costs are allocated to the production activities based on asset value. Maintenance costs are normally allocated based on machine hours. However, Maintenance costs typically correlate more with the number of service calls. Information regarding the activities is provided in the following table: Maintenance Security Mining Cutting Number of service calls 17 20 60 20 Machine hours 89 88 182 176 Asset value $200,000 $80,000 $300,000 $300,000 Department cost $25,000 $42,500 $160,000 $95,000 Is the process of allocating maintenance costs based on machine hours correct? Identify the measure than can possibly be used to allocate the maintenance costs. Measures that can…arrow_forwardSupport activity cost allocation Jake’s Gems mines and produces diamonds, rubies, and other gems. The gems are produced by way of the Mining and Cutting activities. These production activities are supported by the Maintenance and Security activities. Security costs are allocated to the production activities based on asset value. Maintenance costs are normally allocated based on machine hours. However, Maintenance costs typically correlate more with the number of service calls. Information regarding the activities is provided in the following table: Maintenance Security Mining Cutting Number of service calls 17 20 60 20 Machine hours 89 88 182 176 Asset value $200,000 $80,000 $300,000 $300,000 Department cost $25,000 $42,500 $160,000 $95,000 1. Is the process of allocating maintenance costs based on machine hours correct? Identify the measure than can possibly…arrow_forwardSupport activity cost allocationJake’s Gems mines and produces diamonds, rubies, and other gems. The gems are produced by way of the Mining and Cutting activities. These production activities are supported by the Maintenance and Security activities. Security costs are allocated to the production activities based on asset value. Maintenance costs are normally allocated based on machine hours. However, Maintenance costs typically correlate more with the number of service calls. Information regarding the activities is provided in the following table:MaintenanceSecurityMiningCuttingNumber of service calls17 20 60 20 Machine hours89 88 182 176 Asset value$200,000 $80,000 $300,000 $300,000 Department cost$25,000 $42,500 $160,000 $95,000 1. Is the process of allocating maintenance costs based on machine hours correct? Identify the measure than can possibly be used to allocate the maintenance costs.No Measures that can possibly be used to allocate the maintenance costs.a. Number of service…arrow_forward

- Support activity cost allocation Jake's Gems mines and produces diamonds, rubies, and other gems. The gems are produced by way of the Mining and Cutting activities. These production activities are supported by the Maintenance and Security activities. Security costs are allocated to the production activities based on asset value. Maintenance costs are normally allocated based on machine hours. However, Maintenance costs typically correlate more with the number of service calls. Information regarding the activities is provided in the following table: Malntenance Security Mining Cutting Number of service calls 17 20 60 20 Machine hours 89 88 182 176 Asset value $200,000 $80,000 $300,000 $300,000 Department cost $25,000 $42,500 $160,000 1. Is the process of allocating maintenance costs based on machine hours correct? Identify the measure than can possibly be used to allocate the $95,000 maintenance costs. Measures that can possibly be used to allocate the maintenance costs. a. Number of…arrow_forwardJake’s Gems mines and produces diamonds, rubies, and other gems. The gems are produced by way of the Mining and Cutting activities. These production activities are supported by the Maintenance and Security activities. Security costs are allocated to the production activities based on asset value. Maintenance costs are normally allocated based on machine hours. However, Maintenance costs typically correlate more with the number of service calls. Information regarding the activities is provided in the following table: Maintenance Security Mining Cutting Number of service calls 17 20 60 20 Machine hours 89 88 182 176 Asset value $200,000 $80,000 $300,000 $300,000 Department cost $25,000 $42,500 $160,000 $95,000 1. Is the process of allocating maintenance costs based on machine hours correct? Identify the measure than can possibly be used to allocate the…arrow_forwardI need help with the following: Support department cost allocation—reciprocal services method Davis Snowflake & Co. produces Christmas stockings in its Cutting and Sewing departments. The Maintenance and Security departments support the production of the stockings. Costs from the Maintenance Department are allocated based on machine hours, and costs from the Security Department are allocated based on asset value. Information about each department is provided in the following table: MaintenanceDepartment SecurityDepartment CuttingDepartment SewingDepartment Machine hours 800 2,000 6,400 11,600 Asset value $2,000 $1,420 $1,500 $6,500 Department cost $36,720 $16,320 $64,000 $84,000 Determine the total cost of each production department after allocating all support department costs to the production departments using the reciprocal services method. CuttingDepartment SewingDepartment…arrow_forward

- Classify each of the following costs as either unit-level, batch-level, product-level, or facility-level. a. Engineering costs for a new product b. Order processing c. Depreciation on factory d. Direct labor e. Shipment of an order to a customer f. Product line manager salary g. Machine setup costs that are incurred whenever a new production order is started h. Patent for new product ore help Product-level Batch-level or Unit-level or Facility-level Facility-level Unit-level Unit-level Batch-level Batch-level or Facility-level Batch-level or Unit-level Batch-level or Unit-level or Facility-level Facility-level Facility-level or Product-level Facility-level or Unit-level Product-level Unit-level allarrow_forwardAll applicable Exercises are available with McGraw-Hill’s Connect™Accounting.Cost classifications For each of the following costs, check the column(s) that most likely apply:Cost Variable FixedWages of assembly-line workersDepreciation—plant equipmentGlue and threadShipping costsRaw materials handling costsSalary of public relations managerProduction run setup costsPlant utilitiesElectricity cost of retail storesResearch and development expensearrow_forwardClassify each of the following as either one-time or recurring costs: a. training personnel b. initial programming and testing c. systems design d. hardware costs e. software maintenance costsf. site preparation g. rent for facilities h. data conversion from old system to new system i. insurance costs j. installation of original equipment k. hardware upgradesarrow_forward

- Activity Levels and Cost Drivers Shroeder Machine Shop has the following activities: Machine operation Machine setup Production scheduling Materials receiving Research and development Machine maintenance Product design Parts administration Final inspection of a sample of products Materials handling Required Classify each of the activities as a unit-level, batch-level, product-level, or facility-level activity. Identify a potential cost driver for each activity in requirement 1.arrow_forwardMatch each of the following cost items with the value chain business function where you would expect the cost to be incurred: Cost Item 1. Purchase of raw materials 2. Advertising 3. Salary of research scientists 4. Delivery expenses 5. Reengineering of product assembly process 6. Replacement labor expense for warranty repairs 7. Manufacturing supplies 8. Sales salaries 9. Purchase of CAD (computer-aided design) software 10. Salary of website manager Business Functionarrow_forwardLarsen, Inc., produces two types of electronic parts and has provided the following data: There are four activities: machining, setting up, testing, and purchasing. Required: 1. Calculate the activity consumption ratios for each product. 2. Calculate the consumption ratios for the plantwide rate (direct labor hours). When compared with the activity ratios, what can you say about the relative accuracy of a plantwide rate? Which product is undercosted? 3. What if the machine hours were used for the plantwide rate? Would this remove the cost distortion of a plantwide rate?arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning